From 1950 to 2023, the US stock markets have provided a significant average nominal annual return of 11.34% in dollar terms. Over the past five years, the returns have been even higher at 15.75% (in dollars, S&P 500, Shiller Data). The recent performance of the US markets has sparked debate over whether historically high returns can be considered normal in the future.

Many experts have warned that the assumption of continued outperformance is based on historical anomalies and may not be sustainable in the long term.

The current valuation levels of the US markets (2024) are historically exceptionally high, suggesting that future expected returns may be significantly more modest.

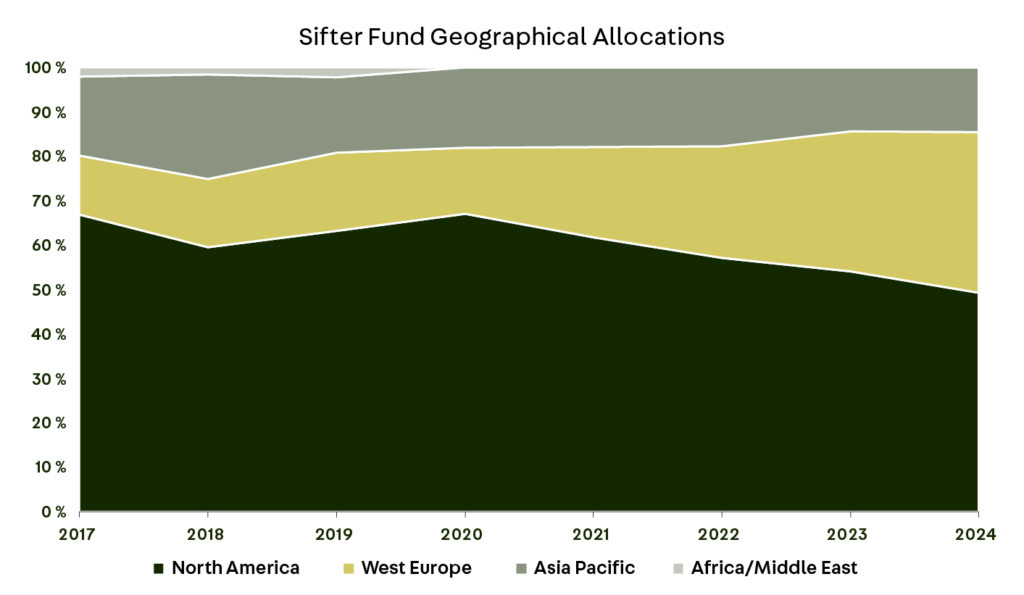

Elevated valuation levels have also been identified at Sifter. The weight of North American companies in the Sifter portfolio has decreased by 18 percentage points over the past 8 years and US-listed companies account for 44%, and Canadian companies for 5% as of 31.5.2024.

The high valuation levels in the United States are a result of the market’s learning process, where investors have become accustomed to viewing the U.S. stock market as a “safe haven,” thereby lowering return expectations and raising valuations.

However, high valuation levels might pose risks.

Valuation levels guide Sifter’s allocations

The allocations of the Sifter Fund are the result of a disciplined investment strategy, and we do not take a stance on the size of our individual country exposures. However, we have a blacklist of countries in which we do not invest. The blacklist consists mainly of countries where investor protection and access to reliable information are weak. These are for example China, Russia and many other emerging markets.

It is most important for us to invest and own highly quality companies whose business results and risks are predictable and balanced.

When a company’s valuation becomes too high, it typically means that the stock has been loaded with excessive expectations, which can increase investor risks.

Sifter’s companies are ranked in internal order based on five year earnings yield. When a company’s earnings forecast weakens, it falls down the list and leads to reduction or sale of the company.

Over the last eight years (2017-2024), the weight of North America has decreased by 18 percentage points in the Sifter portfolio. The primary reason for this reduction has been that we have found companies in other geographical regions with a lower valuations and a more attractive risk-return profile.

Stock selection based on geographical location is not a guarantee of future returns or lower risks – they indicate where our funds are invested and where the company’s headquarters are located. Instead of macro situations, we focus on monitoring the quality and earning potential of the companies we own.

The quality of a company can be assessed by the strength of its revenue model

The revenue model is the engine through which and how a company makes money. Owning a collection of good engines provides protection in different market environments.

If a company’s revenue model is based on projects or demand is cyclical, the company’s profitability and financial position are exposed to excessive risks.

We believe it is safer to own companies whose cash flows consist of recurring reveue streams and products are critical for their customers.

The qualitative characteristics of a company can be evaluated from several perspectives. Often, a quality company’s business is protected by high barriers to entry, patents, and strong competitive advantages. In our opinion, a resilient business model provides solid risk diversification.

Diversification is more than just a precautionary principle – it is a necessary strategy for long-term investors

Harry Markowitz’s famous quote, “diversification is the only free lunch,” remains extremely relevant.

Diversification allows investors not only potentially higher returns but also lower risk when investments are spread across multiple markets and asset classes.

Historical evidence and current research support the idea that investors should not rely solely on consistently high returns from a single stock market.

Instead, international diversification provides a path to exploit global growth opportunities and protect against regional market volatility or prolonged downturns.

Economic and political events can quickly change market dynamics.

For example, Japan’s long-term stagnation since the 1990s and the European economic crises demonstrate how market-specific risks can significantly undermine investment returns.

Conclusions

International diversification is a necessary strategy for long-term investors – it reduces the risks of individual markets and provides access to global growth opportunities.

- Historical returns of the US stock market have been high, but there is no guarantee that the same trend will continue in the future.

- High valuation levels in the United States indicate that future expected returns may be more modest.

- Investor risks increase when stock prices are loaded with excessive expectations.

Riku Pennanen

Relationship Manager