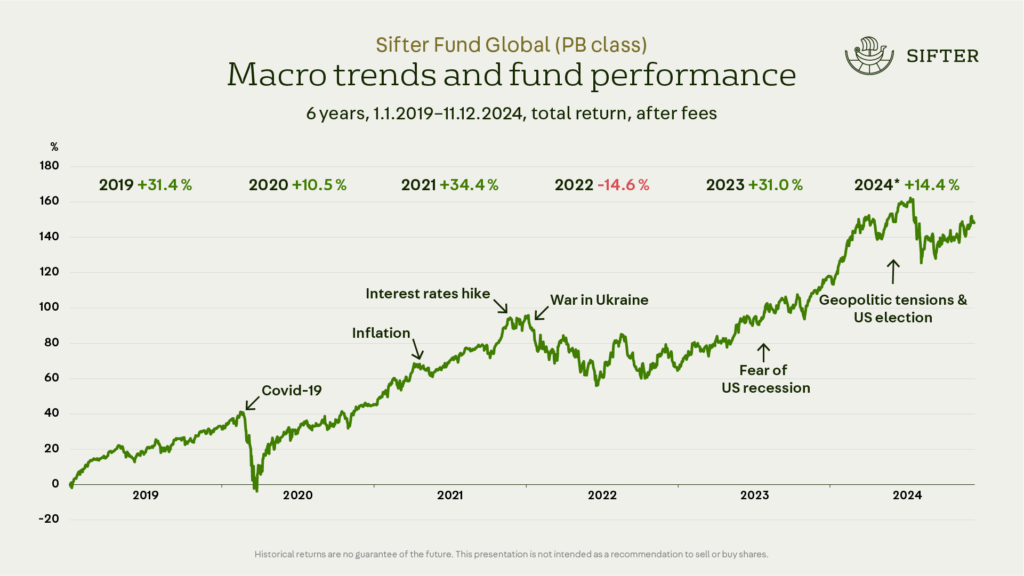

Investors are once again focused on stock price movements, trying to predict potential short-term market directions. This is evident from the number of questions we receive through various channels. When markets are highly active, it’s natural for investors to feel concerned about where things are headed and where Sifter is investing.

At the end of November, we held a two-day workshop with our entire investment team. During the discussions, several global market concerns and their potential impacts on the companies in the Sifter Fund were highlighted.

We shifted our focus to what we can influence—the overall portfolio view: the expected long-term money-making power and valuation levels of Sifter portfolio companies.

We aim to own companies with long-term growth potential and with predictable earnings growth. At the same time, we strive to avoid stocks priced with excessive expectations and uncertainties.

The Pains of the Macro World – The Present Always Feels Harder Than the Past

For those investing based on macroeconomic news, recent years have been exceptionally challenging. When one uncertainty fades, two new ones emerge. It often feels like there’s never a right time to invest.

While high inflation is now behind us, it has been replaced by an unpredictable U.S. president and escalating geopolitical tensions.

In Sifter Fund’s investment strategy, we analyze the effects of macroeconomics on the profitability of our companies, but we rarely make decisions based solely on macroeconomic factors. We remain fully invested in high-quality companies globally in all market conditions.

Expensive Companies Keep Getting Pricier

I recently listened to an excellent podcast discussing Warren Buffett’s stock picks and returns during the 1990s. Many believed the legendary investor had fallen behind because he avoided technology companies and lagged behind index returns. However, Buffett refused to overpay for companies he didn’t fully understand—a decision that ultimately rewarded Berkshire Hathaway’s investors.

In recent years, Sifter’s portfolio management team has faced a similar dilemma.

Avoiding investments in companies like Nvidia makes it challenging to keep pace with indices where these companies play a significant role.

Companies such as Nvidia currently appear to be on the expensive side, especially given the significant uncertainty surrounding their earnings growth over the next five years.

In 2006, Alphabet (Google) was a $10 billion revenue company with a P/E ratio of 68, widely considered overpriced at the time. Eighteen years later, in 2024, Alphabet generates approximately $25 billion in quarterly earnings, with its P/E ratio having dropped to around 25.

Once deemed overvalued, Alphabet’s stock price is now 18 times higher than its 2006 level. Sifter Fund has benefited from Alphabet’s journey since 2015, when its valuation met our criteria.

Companies like Alphabet and Nvidia make investing particularly challenging. Most of today’s overpriced tech companies will not emerge as winners like Alphabet.

We’ve decided not to overpay for market favorites but are willing to pay a slight premium for companies where we see highly predictable earnings growth.

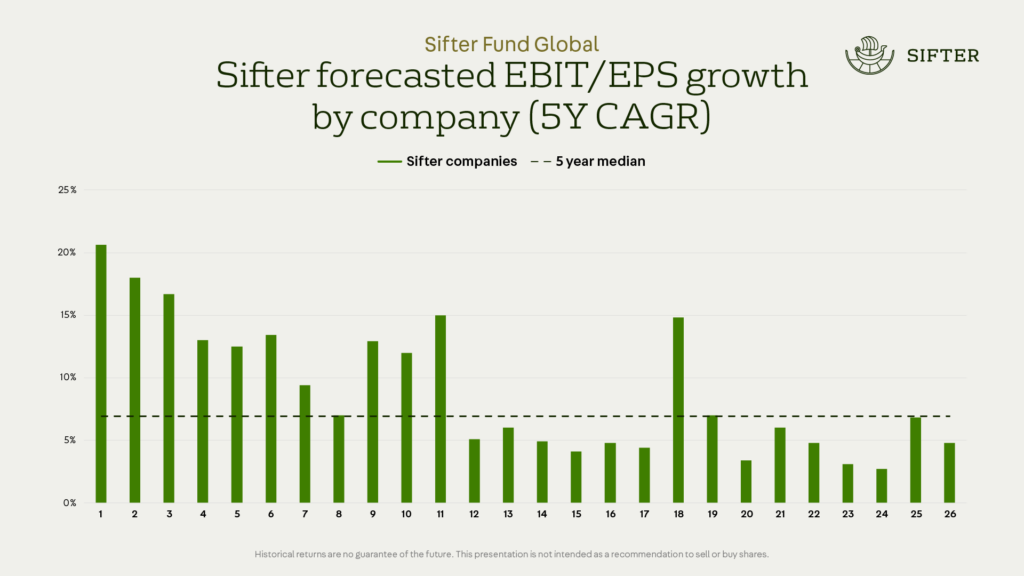

Sifter Companies’ Earnings Forecasts and Valuations up to next 5 Years

During our November workshop, we reviewed all our investments and updated their five-year earnings forecasts. Focusing on long-term earnings helps shift attention away from short-term stock price movements and toward achieving long-term goals.

According to our conservative estimates, Sifter Fund’s earnings growth is expected to average 8% annually over the next five years—an impressive figure.

Broadly speaking, Sifter’s portfolio companies can be categorized into three groups based on growth forecasts, each representing roughly one-third of the portfolio:

- High-growth companies (15–20%), e.g., Novo, Lam Research

- Steady-growth companies (6–12%), e.g., Alphabet, Safran

- Moderate-growth companies (3–5%), e.g., Atlas Copco, Texas Instruments

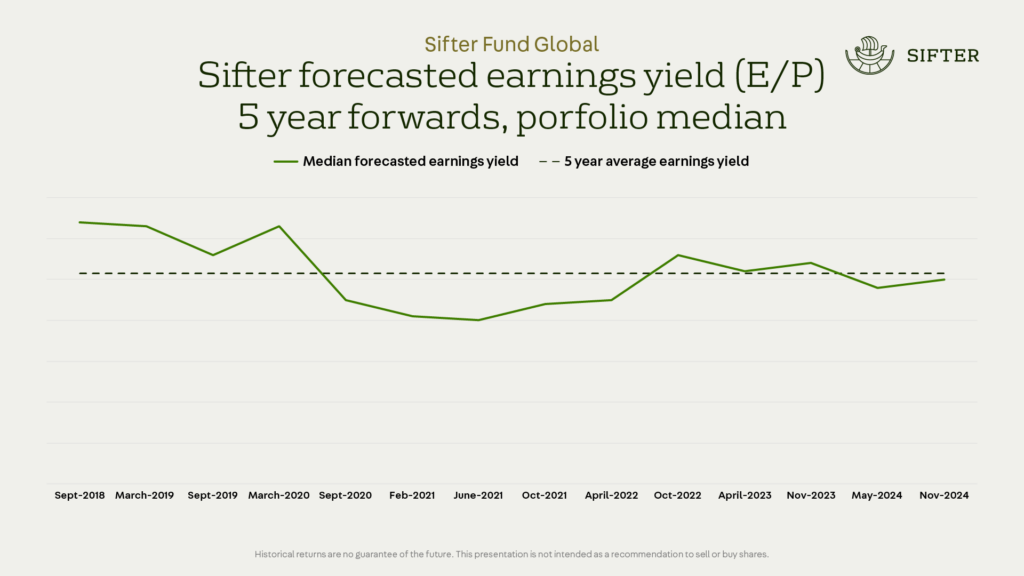

Sifter Portfolio Valuation Has Remained Historically Stable

High growth forecasts tend to be reflected in stock prices early on. The chart below illustrates the development of valuation levels for Sifter Fund’s companies from 2018 to 2024.

Despite a 15% increase in stock prices in 2024, the Sifter portfolio valuation remains at an average level based on the past five years. This is primarily due to improved earnings growth and the addition of new, attractively priced companies that we added into the portfolio during Q1/24.

Given our conservative earnings forecasts, the return potential of our companies now appears slightly stronger than it did at the start of the year.

The main reasons for improved earnings outlook are: 1) semiconductor companies are expected to recover from the bottom of their cycle and deliver stellar profits in the coming years, and 2) the US industrial sector is anticipated to rebound from its downturn.

Return on Invested Capital (ROIC) of Sifter Companies

The return on invested capital (ROIC) for Sifter companies has remained impressively high at a median of 20%, significantly above the S&P 500 average of 10%. This reflects that our companies operate in growing end markets where they hold clear competitive advantages, and their management teams have identified profitable opportunities for reinvestment within their businesses.

When a company’s management invests in business growth with a high ROIC, shareholders can reasonably expect substantial absolute earnings growth in the coming years.

A high ROIC also signals robust end-market demand and growth, as well as management’s confidence that reinvesting in the business offers better returns for shareholders than distributing profits as dividends.

During our two-day workshop, a sense of calm replaced the anxiety—while we cannot control stock prices, we can control what we own.

And that brings us to a point that, unfortunately, causes some headaches.

Could Trump Ruin Everything?

Probably not, at least in the short term. In the near future, tax cuts are likely to boost not only corporate net profits but also consumer purchasing power. It’s fairly certain that U.S. economic growth will continue to accelerate in 2025.

However, in the longer term, potential tariffs and increased consumption could fuel inflation. For now, it seems the U.S. economy is being positioned in a way that offers companies excellent opportunities to grow and thrive.

We conducted our own analysis of Trump’s potential impacts on the companies in the Sifter portfolio. Admittedly, exercises like these can appear logically convincing, but the outcome remains uncertain.

It’s crucial to assess the probabilities of tariffs and their impacts on different companies.

Even if we managed to evaluate all possible variables correctly, the final question remains how the stock market will price these effects. As a result of our analysis, we made small adjustments to portfolio weights but did not fully exit any company solely due to Trump’s potential influence.

Based on our analysis, the expected Trump effect on Sifter Portfolio is expected to be slightly positive, on average.

| Company | Risk | Reasons |

|---|---|---|

| Microsoft | Positive |

|

| Alphabet | Positive |

|

| Old Dominion Freight Line | Positive |

|

| Novo Nordisk | Negative |

|

| Safran | Slightly Negative |

|

Impact of Trump’s Actions on the Semiconductor Industry

The semiconductor industry deserves its own discussion, as it represents one of the most advanced global networks of collaboration across continents, countries, and companies. Overall, the industry’s outlook is positive, as it is emerging from the bottom of its cycle and is expected to grow 10% per annum next 10 years.

However, a new concern arises with the potential side effects of Trump’s tariffs and possible trade war.

Semiconductors rely on a global and interdependent network. The players in the value chain are interconnected, and no single company or country is fully self-sufficient.

A potential trade war with China could result in a ban on selling advanced semiconductor equipment or chips to China. Similar restrictions have already been in place in recent years, yet China has managed to invest in and purchase more semiconductor equipment and chips than even oil. It remains to be seen how tariffs and sanctions will reshape the entire semiconductor value chain.

Minor Portfolio Adjustments in Early December

To reduce risks for Sifter investors, we trimmed the oversized position in TSMC in early December. TSMC’s stock price has risen by over 70% since the beginning of the year, while geopolitical and trade war-related risks have increased once again.

We realized part of the profits from TSMC and reallocated funds to Alphabet, which we consider one of the most attractively priced technology companies with a more stable risk profile.

Santeri Korpinen

CEO