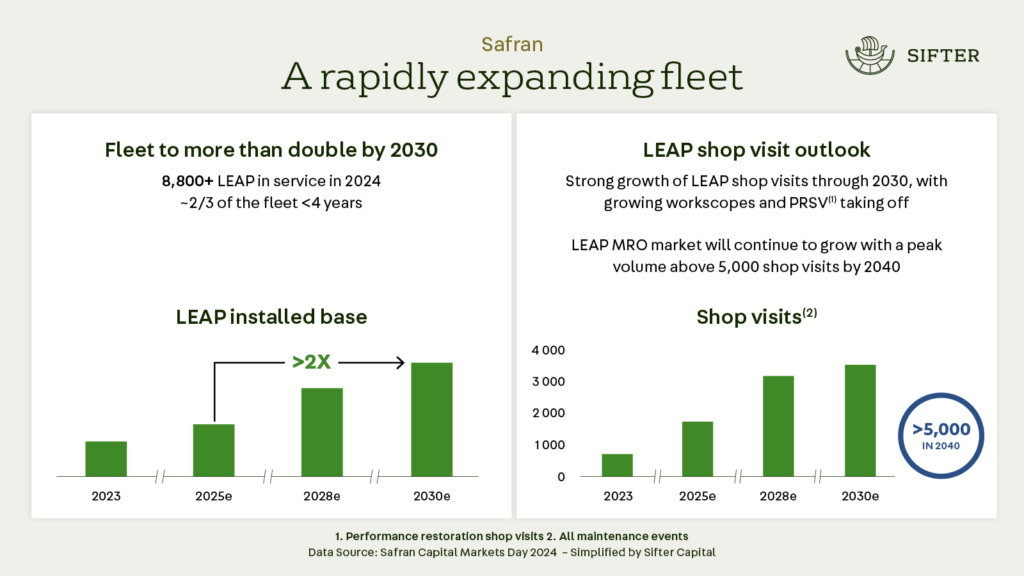

Safran is known for its Leap engines, which have gained almost a monopoly position in narrow-body Airbus and Boeing aircraft. Growth is on the way, as the number of airplanes is expected to double by 2040.

Safran is an excellent example of a Sifter Fund quality investment with sustainable competitive advantages and a strong business model. The company operates in a growing industry and has predictable revenue streams.

We made our first investment in Safran in 2015. Nearly ten years later, the company became the largest investment in the Sifter Fund portfolio in February 2025.

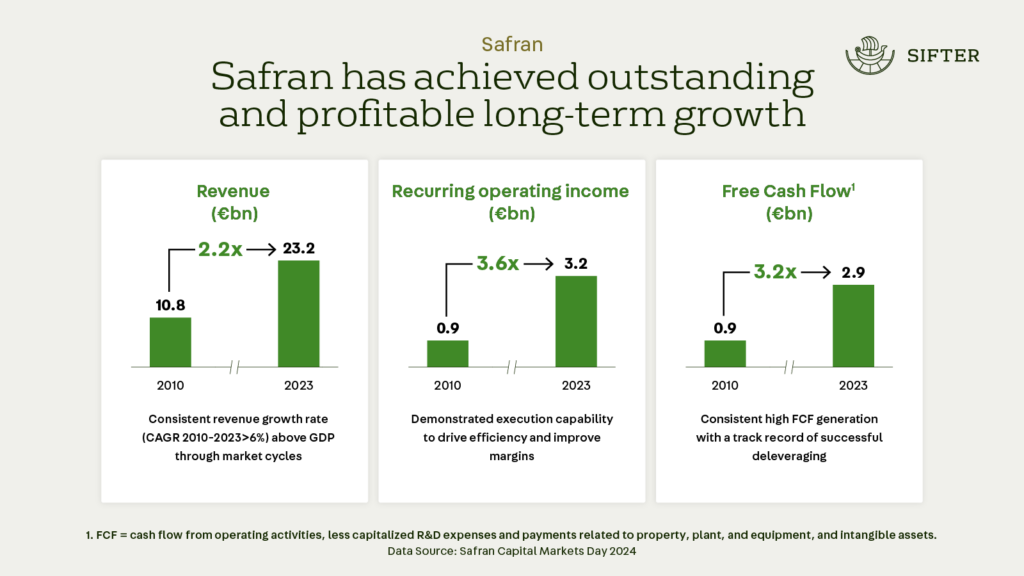

The beauty of Safran’s business model lies in its predictability.

Although the margins on engine sales are not impressive, Safran makes its money from long-term maintenance for engines, which provide predictable, growing, and highly profitable cash flows.

Three key factors stand out in Safran’s business that align perfectly with Sifter’s investment criteria.

- The company has clear competitive advantages.

- The demand for its products or services is growing.

- The company has a healthy balance sheet and is preferably debt-free.

Let’s look at Safran’s business from the perspective of predictability.

Competitive Advantages Provide Protection and Improve Predictability

High-margin businesses attract competition. Therefore, we seek to own companies with clear competitive advantages that create high barriers to entry and prevent competitors from entering the same market.

Safran’s competitive advantages can be seen in its technological expertise, strong customer relationships, long-term contracts, high switching costs, and global network.

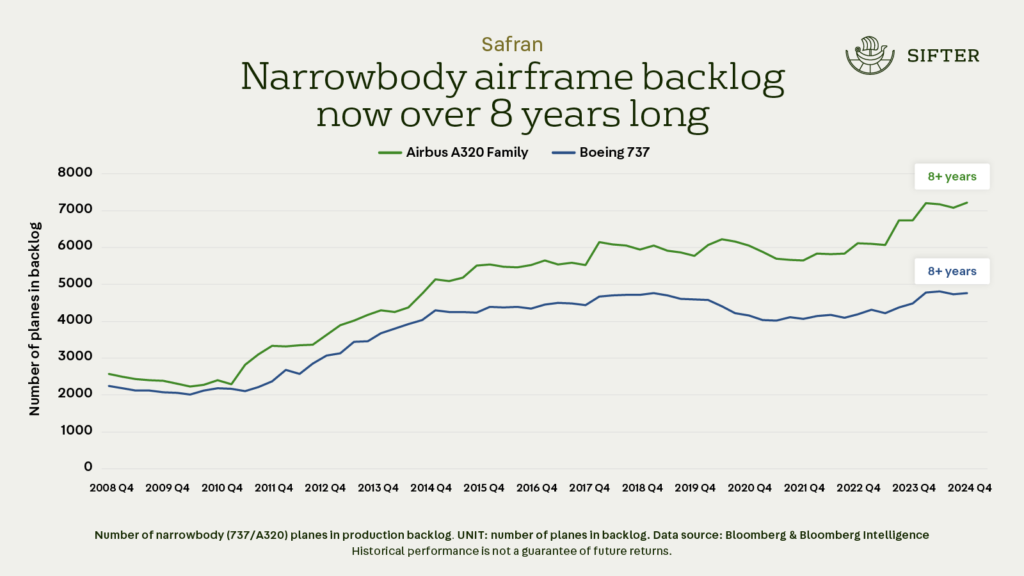

The aviation industry is one of the most strictly regulated industries. All parts used in airplanes and their suppliers must meet the requirements and pass tests from multiple regulatory authorities.

It is extremely difficult for new competitors to enter such a strictly regulated market.

Developing a new aircraft engine takes decades and requires vast technological expertise. Safran has a large portfolio of patents and intellectual property rights that protect the company’s developed technologies and products from potential competition.

Market Growth Enables Future Growth

Sifter Fund wants to own companies that operate in a market with growing end-demand. The growth of end-demand brings organic growth opportunities for companies that are market leaders and have competitive advantages.

The growth of air traffic drives Safran’s long-term growth.

The number of aircraft is expected to double by 2040, meaning that the number of engines requiring maintenance will increase significantly as the number of airplanes grows.

In Sifter’s investment strategy, the growth and predictability of a company’s business play a central role in making investment decisions. We prefer companies like Safran, which can profitably generate returns from the industry’s growth.

We avoid industries or markets with weak growth prospects. The withering of demand growth ultimately leads to stagnation.

Recurring Service Revenue Models Enhance Long-Term Predictability

Recurring service revenue models provide an excellent opportunity to forecast a company’s long-term cash flows. We want to own companies whose cash flows mainly consist of recurring services.

Safran’s business is largely based on maintenance for engines sold, which generates stable and highly profitable revenue streams for the company.

By knowing how many engines Safran manufactures annually and how many engines it has under maintenance, we can predict how the maintenance business will perform in the future.

Long-term contracts secured by recurring revenue streams are predictable and provide peace of mind, especially when products or services are critical for their customers.

The criticality of products or services for customers gives investors confidence that demand will remain high even during economic downturns, which improves the predictability of the company’s business.

Sifter Fund favors companies whose products or services are so critical to end customers that they are not easily replaced or discontinued.

It is difficult to imagine a scenario where aircraft engines would be replaced by another manufacturer’s engines during their lifespan.

Summary

Safran is an excellent example of a Sifter Fund quality investment with sustainable competitive advantages and a strong business model. The company operates in a growing industry and has predictable revenue streams.

Safran’s strong market position, high barriers to entry, and established customer relationships—especially with Airbus and Boeing—provide protection during economic fluctuations.

Sifter Fund focuses on long-term ownership in very high-quality companies with predictable business models. Predictability brings stability and helps manage risks in the long term.

Santeri Korpinen

CEO