In the summer of 2025, we finally invested on IDEXX Laboratories. We had followed the company for years, fully convinced of its quality, yet always kept at a distance because the valuation felt too high. This time the setup looked different.

In this article we look at what IDEXX Laboratories does, how it makes money, and why we believe its earnings can grow over the next five years, making it a good fit for Sifter’s long-term quality portfolio.

What IDEXX Laboratories Does and How It Makes Money

IDEXX is a global leader in pet diagnostics. The company manufactures in-clinic diagnostic analyzers, provides laboratory services, and offers a full ecosystem of software and apps that help veterinarians run tests and diagnose pets in-house within minutes.

When a pet owner brings their dog or cat to a veterinary clinic. The veterinarian draws a small blood sample and places it into an IDEXX analyzer.

Within minutes the device delivers results that allow the vet to diagnose infections, organ problems, or more serious diseases on the spot. If a more advanced test is needed, the sample is sent to an IDEXX reference laboratory.

IDEXX operates a razor and blade business model where analyzers drive long-term demand for high-margin consumables. Once installed, the devices become part of a clinic’s routine, and every test run or consumable used generates recurring revenue.

This is a highly scalable business model because new tests and upgrades roll out instantly across the global installed base. The more tests clinics run, the more consumables they use, making consumables the key driver of predictable long-term earnings.

IDEXX generates roughly 4 billion dollars in annual revenue. About 60 percent comes from the United States and 40 percent from international markets. The company operates in about 175 countries and serves more than 100,000 veterinary clinics worldwide.

1. Predictable Growth

At Sifter, predictable growth is the foundation of a long-term compounder. Earnings growth must be visible and supported by clear drivers. IDEXX fits this description well.

Pets live longer today thanks to better health care and a stronger bond between humans and animals.

Diagnostic testing has become more common as pet owners seek better care for their pets, creating a reinforcing cycle where frequent diagnostics support longer lifespans and those longer lifespans lead to even more testing.

IDEXX supports this trend by continually developing new diagnostic tests and educating veterinarians on modern diagnostics. One recent example is the fine needle aspiration capability in its latest analyzer, which allows vets to diagnose certain cancers within minutes instead of sending samples to a lab.

The industry has grown about 9 percent annually in the last decade, and is expected to continue experiencing strong growth. IDEXX holds roughly 50 percent of the global veterinary diagnostics market. The company targets 8.5 to 11 percent long-term organic growth.

With recurring revenue streams, multi-year contracts, and consumables making up a large share of sales, we view IDEXX as a business with a highly predictable growth trajectory.

2. Strong Moat

A quality company must have structural advantages that protect it from competition, and in IDEXX’s case there are three factors that together create a moat that is very hard for competitors to break.

1. Fragmented and demaning customer base

Veterinary clinics are a fragmented customer group, yet they require a broad range of diagnostic tools. IDEXX offers a fully integrated solution that includes analyzers, lab services, software, and education. This ecosystem saves vets time and produces reliable results, making it hard for competitors to break in.

2. Strong investment in product development

IDEXX invests heavily in product development, roughly 7 to 8 percent of revenue per year, which rivals what some competitors generate in total revenue. New tests and product improvements scale instantly across the global installed base of analyzers, reinforcing IDEXX’s market leadership.

3. High switching costs

Clinics are typically locked into multi-year contracts and rely on IDEXX’s systems in their daily workflow. Once the equipment, software, and lab processes are fully integrated, switching becomes costly and disruptive. These high switching costs create a powerful lock-in effect.

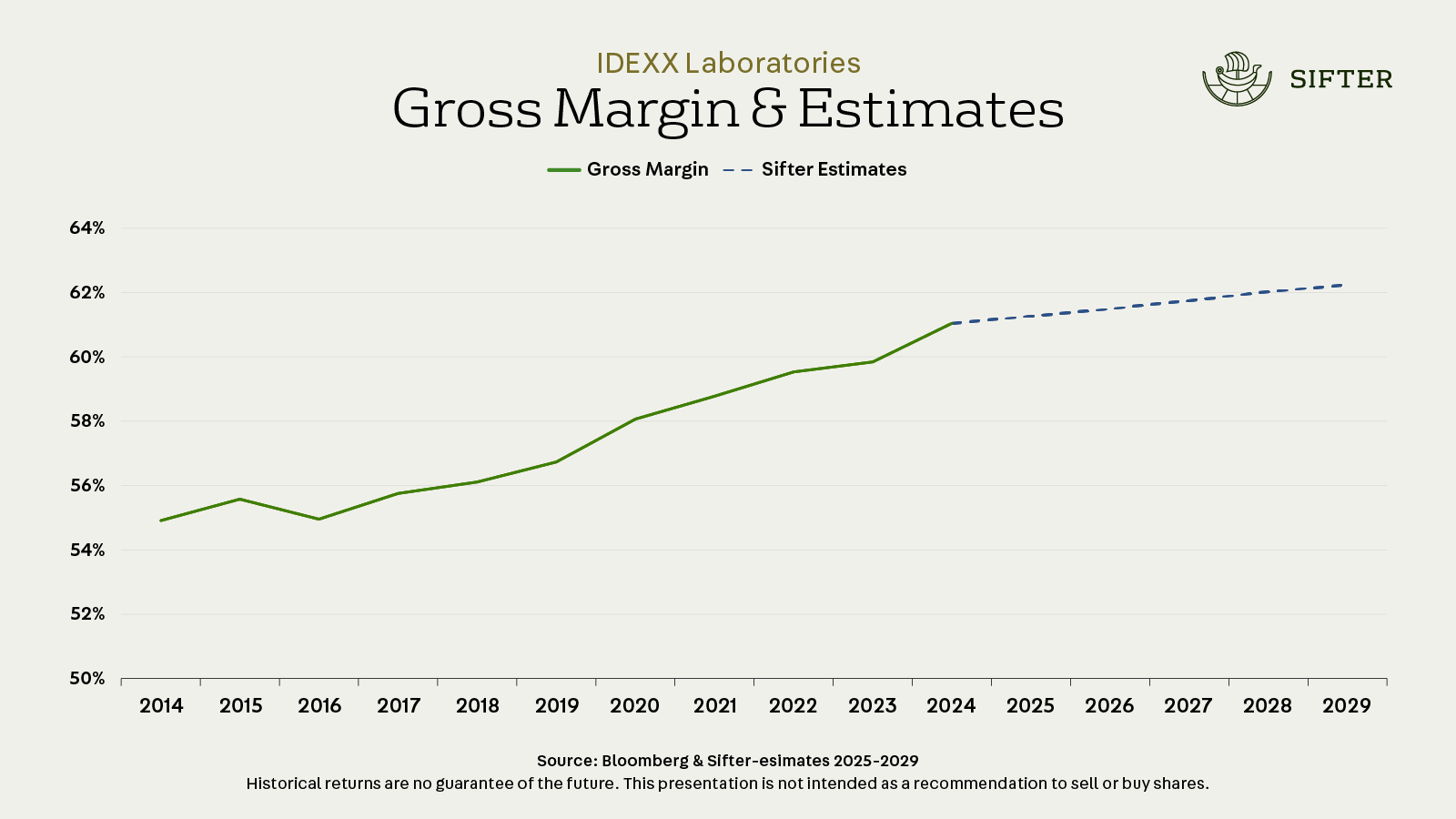

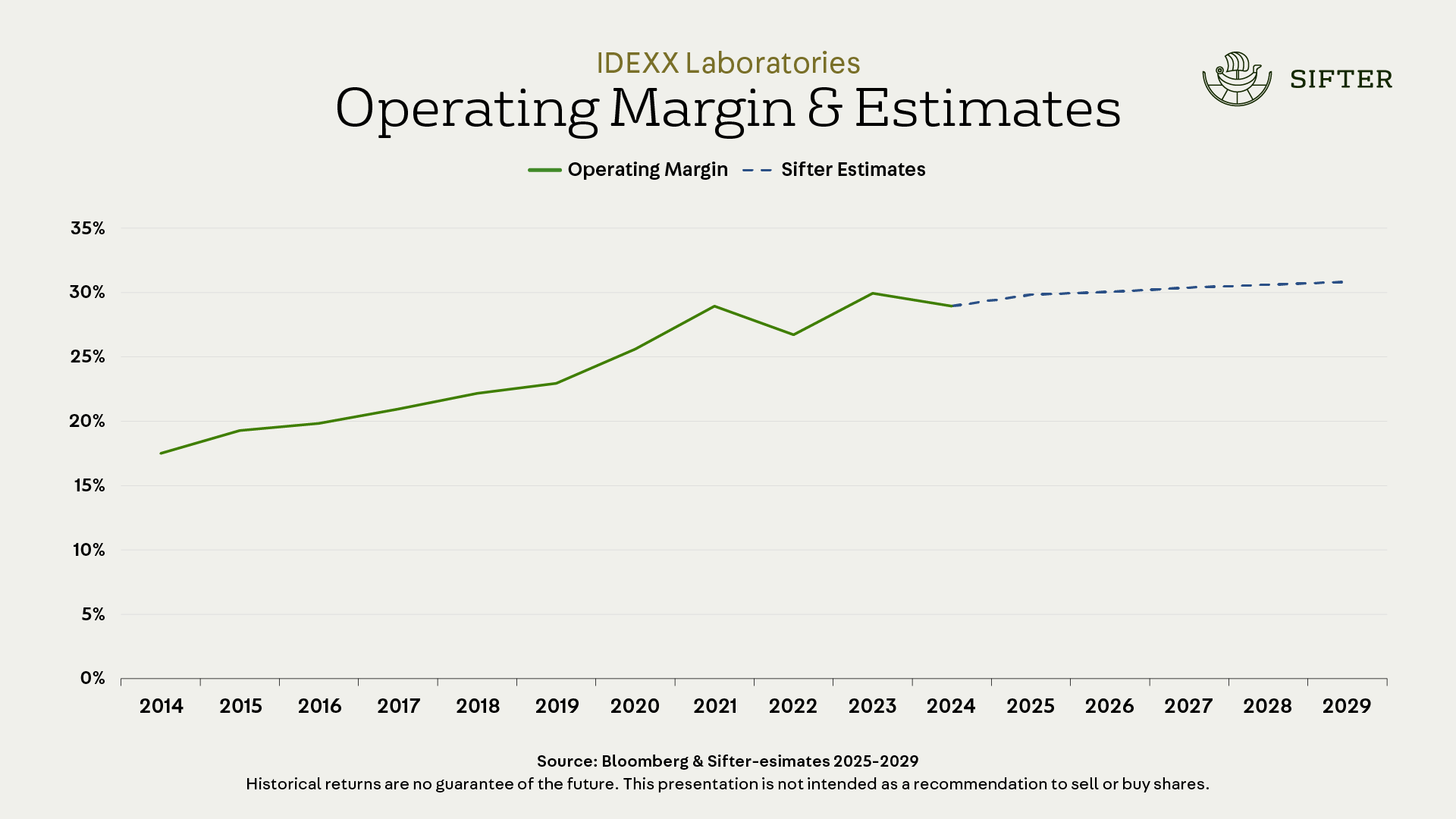

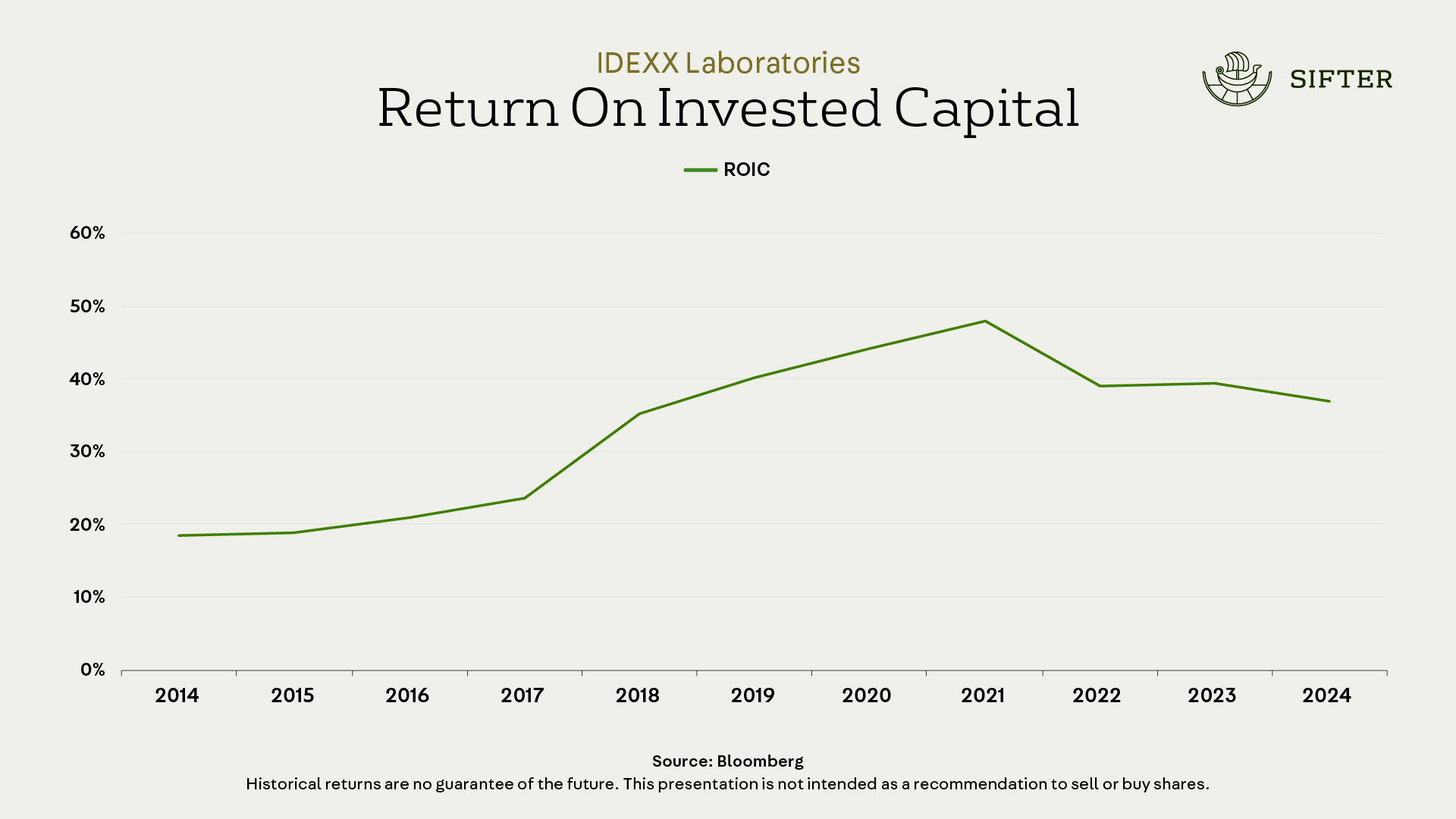

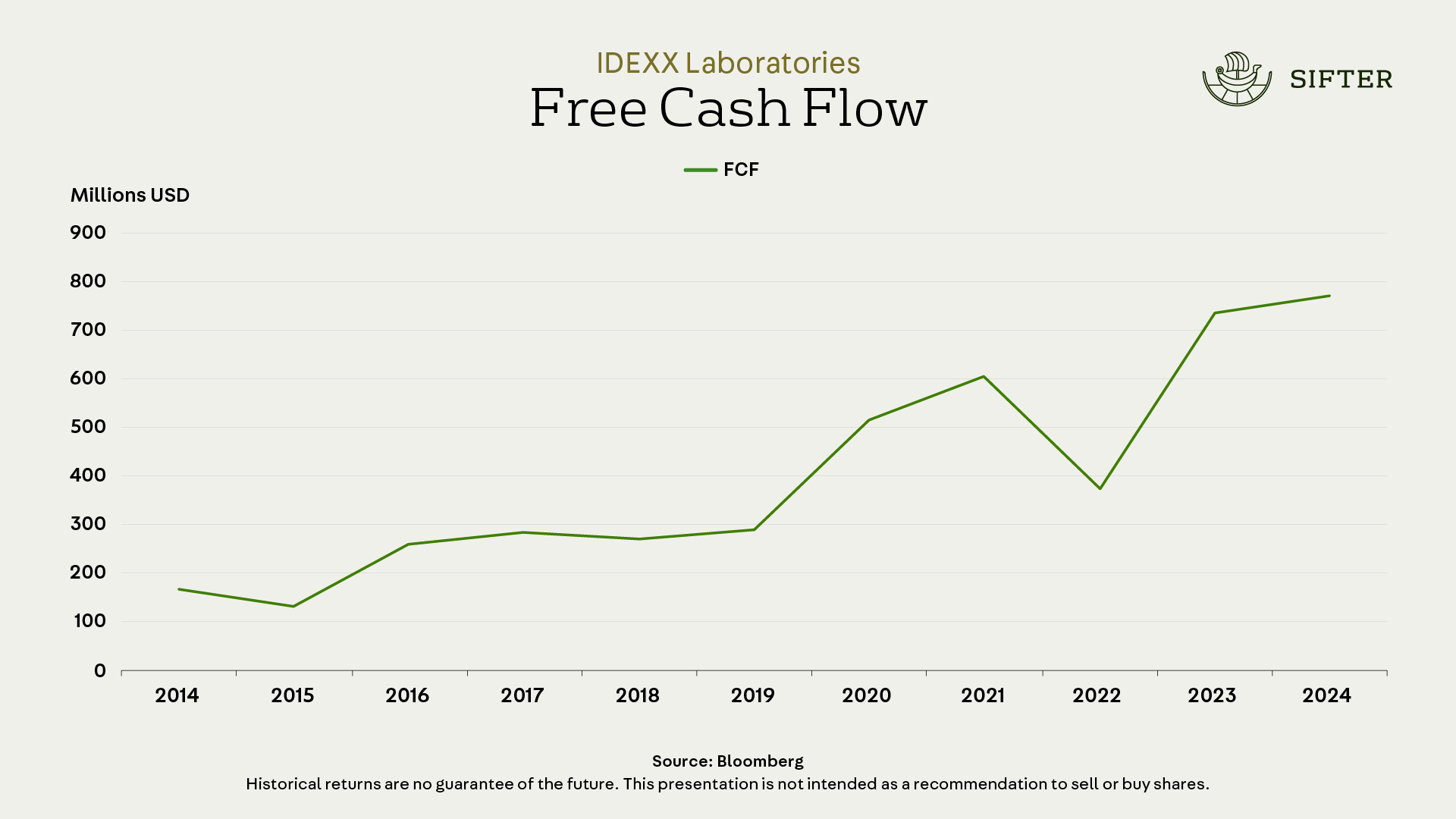

3. Solid Financials

Financial figures are what separate good companies from great ones. Strong growth and a durable moat tend to show up clearly in the financials, and IDEXX is a good example of how quality becomes visible in the numbers.

Investment needs are low outside of R&D. The balance sheet is strong, with low net debt and high cash generation. These characteristics give IDEXX the flexibility to reinvest in innovation, buy back shares, and pursue new growth opportunities.

4. Attractive Valuation

Quality companies rarely trade at bargain prices, and IDEXX is no exception. The question is whether the quality, growth potential, and durability justify the price.

Historically, we viewed IDEXX as too expensive. Pandemic-era expectations drove valuations to unsustainable levels.

By June 2025, those expectations had normalized, and the valuation had fallen to a level we considered reasonable. We initiated a position of about 2.5 percent of portfolio assets, which is typical for a new investment.

Since then, growth in consumables has reaccelerated faster than expected. While this has supported the share price, valuation must always be monitored.

As long-term quality investors, we continuously evaluate each company in the portfolio. If expectations rise too far or valuation becomes detached from fundamentals, we are ready to trim or exit. For now, IDEXX behaves as a company that fits our investment hypothesis.

Summary

IDEXX is a global leader in pet diagnostics with predictable growth, strong moat, solid financials, and a valuation we considered fair at the time of investment.

The company benefits from rising pet-care demand, holds a leading position in global diagnostics, and generates high recurring revenue from consumables and lab services.

With strong margins, excellent returns on invested capital, and low capital intensity, IDEXX has the qualities we look for in a long-term compounder.

Karl Lidsle

Portfolio Manager