After a long bull market, one of the most common questions we ask ourselves as investors is whether it makes sense to postpone investing and wait for a market correction.

When share prices stand at all-time highs, some investors see strong momentum and opportunity, while others fear an approaching correction.

None of us wants to invest just before a market decline.

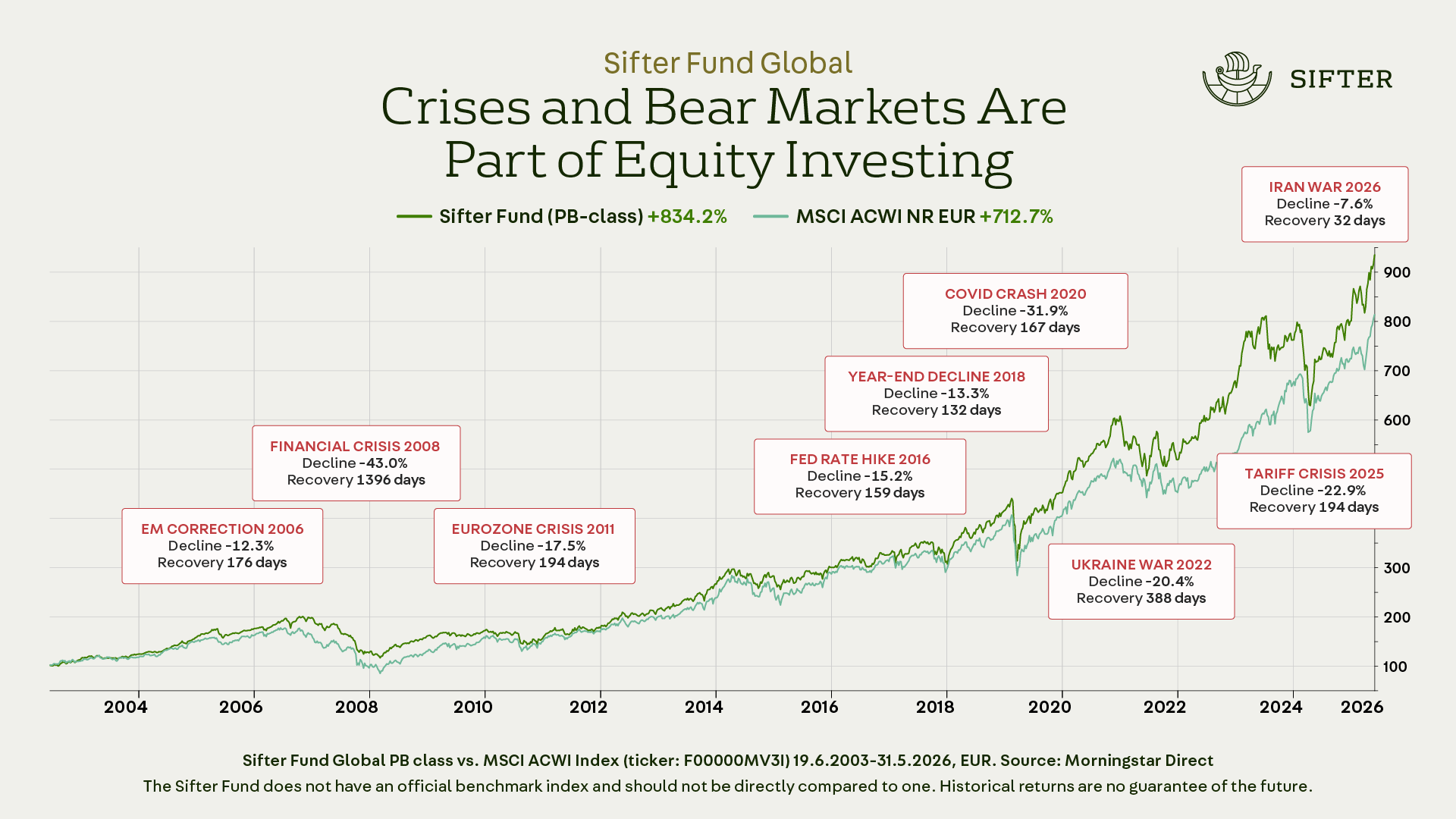

However, many of history’s best investment returns have come not from perfect timing but from the ability to own quality companies for long enough.

Historically, high valuation levels have often preceded more modest future returns, and share prices tend to run ahead of earnings from time to time.

This does not automatically mean, however, that the best course of action is to wait on the sidelines.

Core Principle of Sifter Fund Investment Strategy

We believe an investor is better served by spending more time considering what kind of companies they want to own over the next ten years than by trying to predict what the markets will do over the next ten months, or to find the perfect moment to buy.

The market is more efficient than we would like to believe

Market efficiency refers to the idea that all available information is already reflected in share prices.

The Nobel laureate Robert Shiller has aptly described market efficiency as a “half-truth”. Markets are not perfectly efficient, but they are considerably more efficient than many of us would like to believe.

Share prices are formed from the views of millions of market participants, among them analysts, pension funds, hedge funds, insurance companies and private investors.

This is why I find myself returning, from time to time, to a simple question:

What do I know that the market does not?

The question does not imply that the market is always right. History is full of bubbles, overreactions and long stretches when prices have detached from fundamentals. What it does is remind us how high the bar for successful market timing really is.

In hindsight, everything looks obvious

One reason market timing often looks easy is that we examine history after the fact. What looks in hindsight like an obvious timing mistake was not necessarily a mistake at the moment the decision was made. On a price chart it is easy to point to where one should have sold and where one should have bought.

Yet the present moment almost always feels exceptionally uncertain, as though there is never a right time to invest.

In reality, investment decisions are always made in the midst of uncertainty. At the moment of decision, no one knows which part of the flow of news is already in the prices and which is not.

A market that looks expensive today relative to the past ten years may, in hindsight, look inexpensive relative to the next ten.

Returns come from the earnings growth of companies

Over the long term, equity returns are determined above all by companies’ ability to grow their earnings. As investors, we do not ultimately own share prices but stakes in businesses.

The management of the world’s best companies spends every day working to grow revenue, cash flow, market share and competitive advantages. It is precisely this value creation that has been the most important driver of long-term equity returns.

As investors, we easily fall into thinking that high valuations are inevitably corrected through a fall in prices. This happens sometimes, but not always.

Valuations can also normalise as companies’ earnings grow while share prices move sideways for an extended period. In other words, companies can grow into their valuations without a significant market correction.

Uncomfortable moments are part of investing

In the interest of honesty, it should be said that this is not always easy.

There are periods when markets feel expensive, optimism looks excessive and the news offers more reasons for concern than for enthusiasm. As an investor, it is entirely natural to wonder whether cash might be the better option right now.

I have thought this way myself.

In the end, though, the question is not whether the markets are perfectly priced at this particular moment. The question is which option looks most attractive over the long term.

Would I rather own a stake in quality companies whose management works to grow earnings, cash flow and competitive advantages year after year, or hold my assets in cash while waiting for a moment I will only recognise after it has passed?

Often it is precisely this perspective that helps us stay patient when markets feel at their most uncomfortable.

Waiting is also an investment decision

This is one reason market timing is so difficult. In practice, we would need to get at least four decisions right: when to sell, how much to sell, when to buy back and how much to buy back.

Getting one decision right is hard. Getting four decisions right consistently is considerably harder still.

Waiting, moreover, often feels like a neutral choice, even though in reality it is an investment decision too.

When we postpone investing in the hope of a better entry point, we are at the same time taking a view: that staying on the sidelines is, right now, a better option than being in the market.

Finding the right level of risk and staying with it

This does not mean that risks should be ignored or that one should invest at any price. On the contrary.

Risk is an essential part of investing, and each of us should build a portfolio we can live with through difficult times as well.

Looked at historically, our greatest mistakes as investors have rarely had to do with starting to invest slightly too early.

Far more often, the problem has been interrupting our long-term plan when markets turned uncomfortable.

In investing, what matters is neither avoiding risk nor maximising it. What matters is finding a level of risk that suits you and staying with it, also when markets turn uncomfortable.

At Sifter, we believe an investor is better served by spending more time considering what kind of companies they want to own over the next ten years than by trying to predict what the markets will do over the next ten months.

Over the long term, it is companies’ earnings development that grows the value of investments, not the ability to predict the market’s short-term movements.

Charlie Munger famously distilled the idea:

“The big money is not in the buying and the selling, but in the waiting.”

Many of history’s best investment returns have come not from perfect timing but from the ability to own quality companies for long enough.

At Sifter, we believe an investor is better served by spending more time considering what kind of companies they want to own over the next ten years than by trying to predict what the markets will do over the next ten months, or to find the perfect moment to buy.

Riku Pennanen

Investor Relations