The second quarter was a strong one for the Fund. The Sifter Fund PB class rose 18.5%, and year to date the Fund has returned 18.9% (30 June 2026). A significant part of the gains came from semiconductor companies and it was precisely those we decided to trim.

Many investors will recognise the situation. As a rally continues, it is tempting to let your winners run, and trimming can feel like a mistake. Over the long term, however, a portfolio’s return is not built on individual rockets, but on keeping the overall valuation level sensible year after year.

Please note that the Fund’s past performance is not a guarantee of future results.

A Divided Start to the Year

Most of the year’s gains were generated during the second quarter. The first quarter was clearly more difficult: the conflict in Iran in March effectively wiped out the early-year returns, but the second quarter recouped them in record fashion. A single quarter is still a poor measure of how well a strategy is working. Longer periods tell a more complete story.

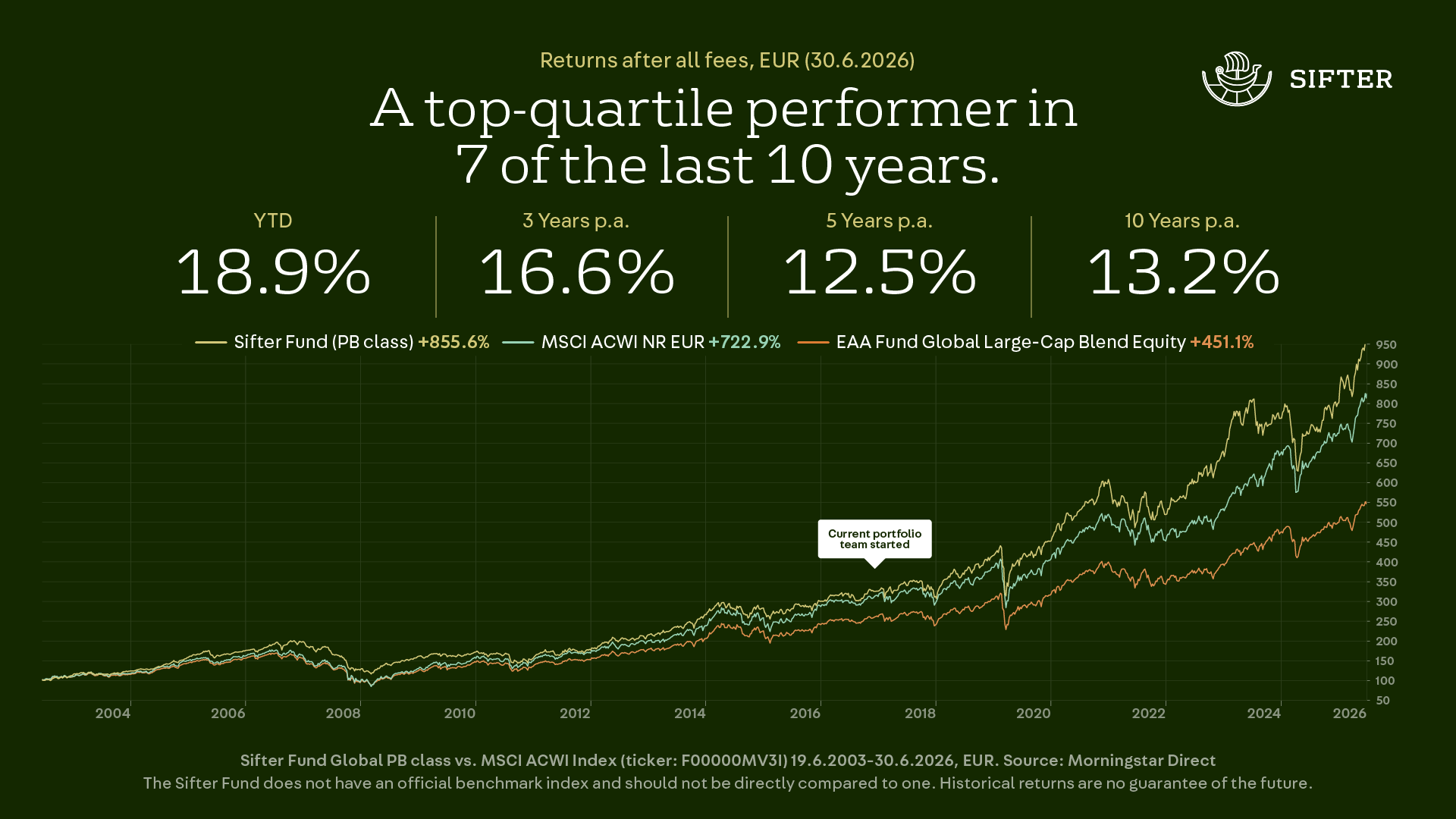

The Sifter Fund turned 23 in June.

Over its 23-year history, the Sifter Fund has returned +855.6% (PB class) after fees. That is approximately 130 percentage points more than the global equity index (MSCI ACWI NR EUR) and approximately 400 percentage points more than the peer group average (EAA Fund Global Large-Cap Blend Equity).

It is still worth remembering that the Sifter Fund does not beat the index every year. There are weaker years along the way, and the strategy has worked precisely because it has been applied with patience over the long term.

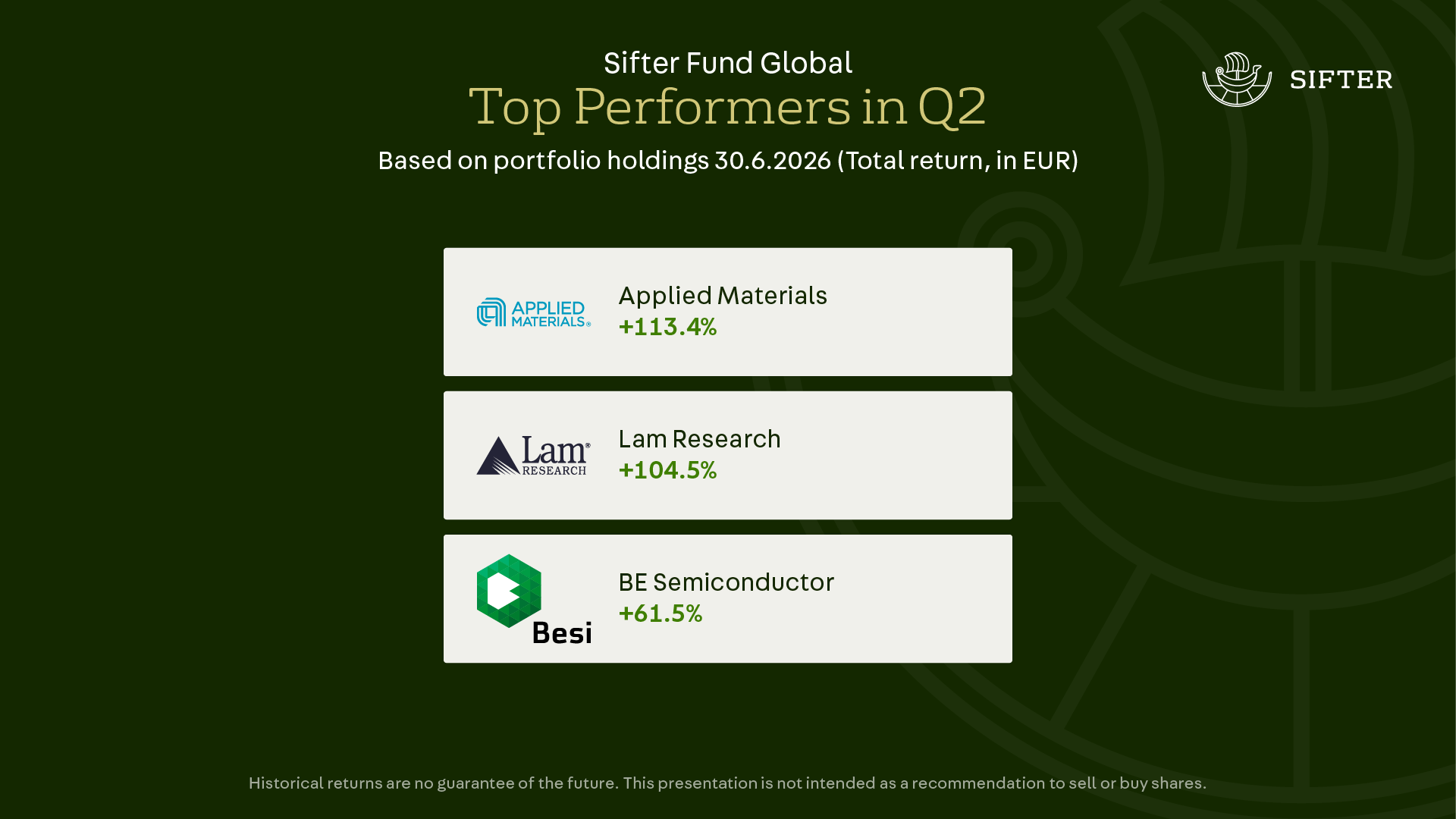

Top Performers Q2/2026

The three best performers of the quarter were all semiconductor equipment and materials companies: Applied Materials +113.4%, Lam Research +104.5% and BE Semiconductor +61.5%.

There is a strong structural driver behind the rally: the data-centre construction boom continues, the industry cycle is strong, and a shortage in memory chips in particular signals future investment in new production capacity. All three companies benefit directly from this wave of investment.

The share prices of Applied Materials and Lam Research more than doubled in a single quarter. Although the companies’ fundamentals and outlook have strengthened, in our view the shares’ valuation ran ahead of the long-term earnings estimates for the business.

The strongest performer after the top three was West Pharmaceutical Services, a manufacturer of rubber components for the pharmaceutical industry. It was one of the portfolio’s biggest decliners last year, but the share has now turned higher, driven in part by the rapid growth of GLP-1 drugs. West supplies the rubber components used in the syringes for these drugs.

West’s example is a good reminder that even a quality company goes through difficult periods. When the business returns to its proper footing, the share price tends to follow.

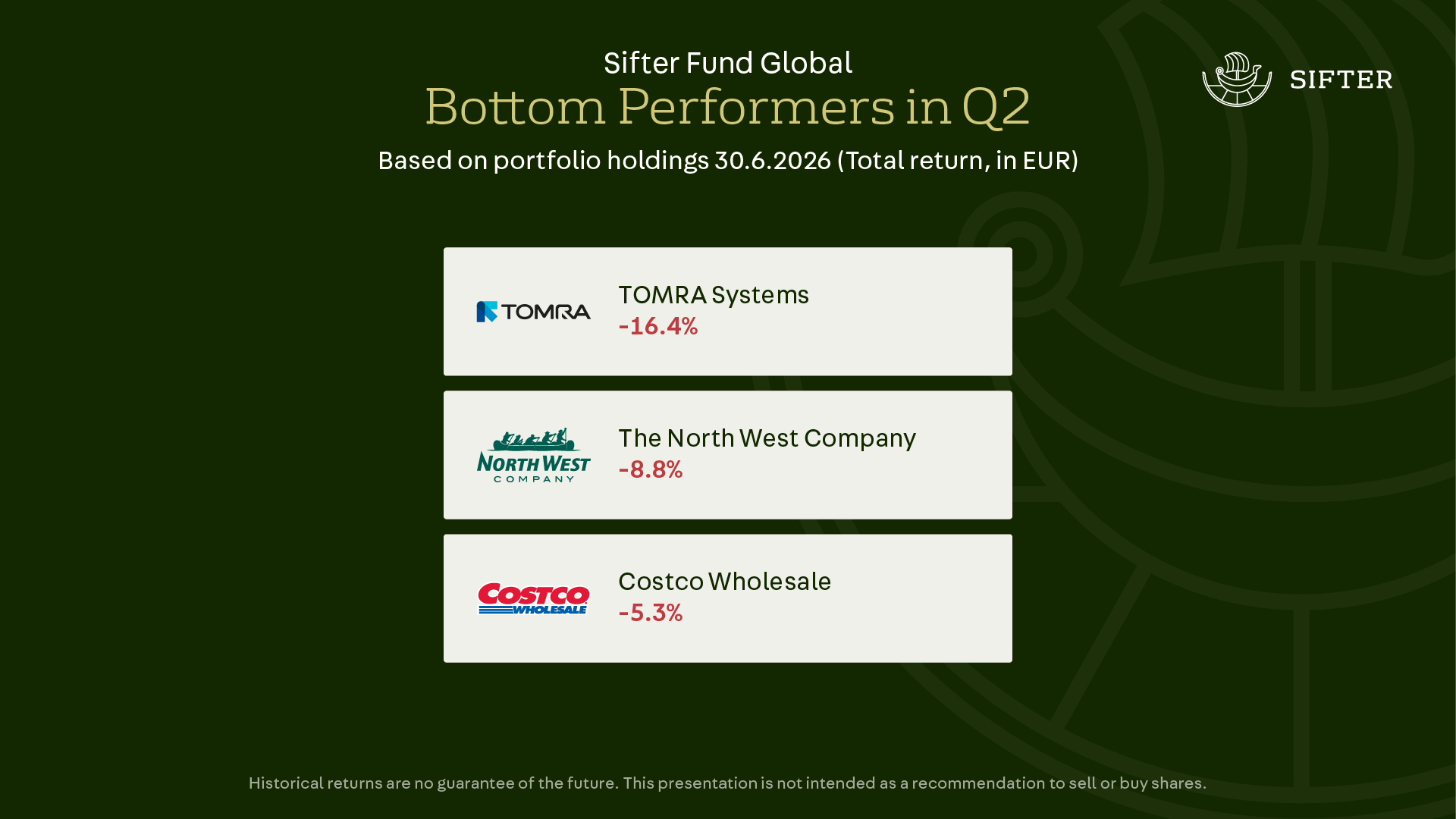

Bottom Performers Q2/2026

The three weakest holdings were TOMRA Systems -16.4%, The North West Company -8.8% and Costco Wholesale -5.3%.

TOMRA’s decline was company-specific. Of the company’s three divisions, recycling turned down in both revenue and earnings. This is hopefully a temporary dip rather than a structural change in the business model. We are following TOMRA’s outlook closely.

Behind Costco and North West lies largely a market rotation. Both were first-quarter winners, when the market sought safety in defensive retail shares during the conflict in Iran. As the conflict appeared to calm during the second quarter, a natural rotation out of defensive shares followed.

Has the Fund’s Valuation Risen Too High?

We are often asked: the Fund has risen a great deal, aren’t valuations already high? It is a fair question. The portfolio’s share prices have risen by around 80% over five years, or approximately 12.5% per year.

We track the portfolio’s valuation using the fifth-year earnings yield. We look five years ahead at the companies’ earnings and relate them to today’s share price; the resulting figure is the earnings yield. The Fund’s earnings yield has barely changed, and the valuation level has stayed close to its long-term average, even as share prices have risen.

The reason is simple. The portfolio companies’ earnings have grown by an average of around 13.5% per year over the past five years. The rise in value is therefore driven by the companies’ earnings growth, not by an expansion of valuation multiples.

Alongside owning high-quality companies, our other task is to keep the portfolio’s valuation level sensible. That is precisely why we also trim our best performers when the price runs ahead of the business.

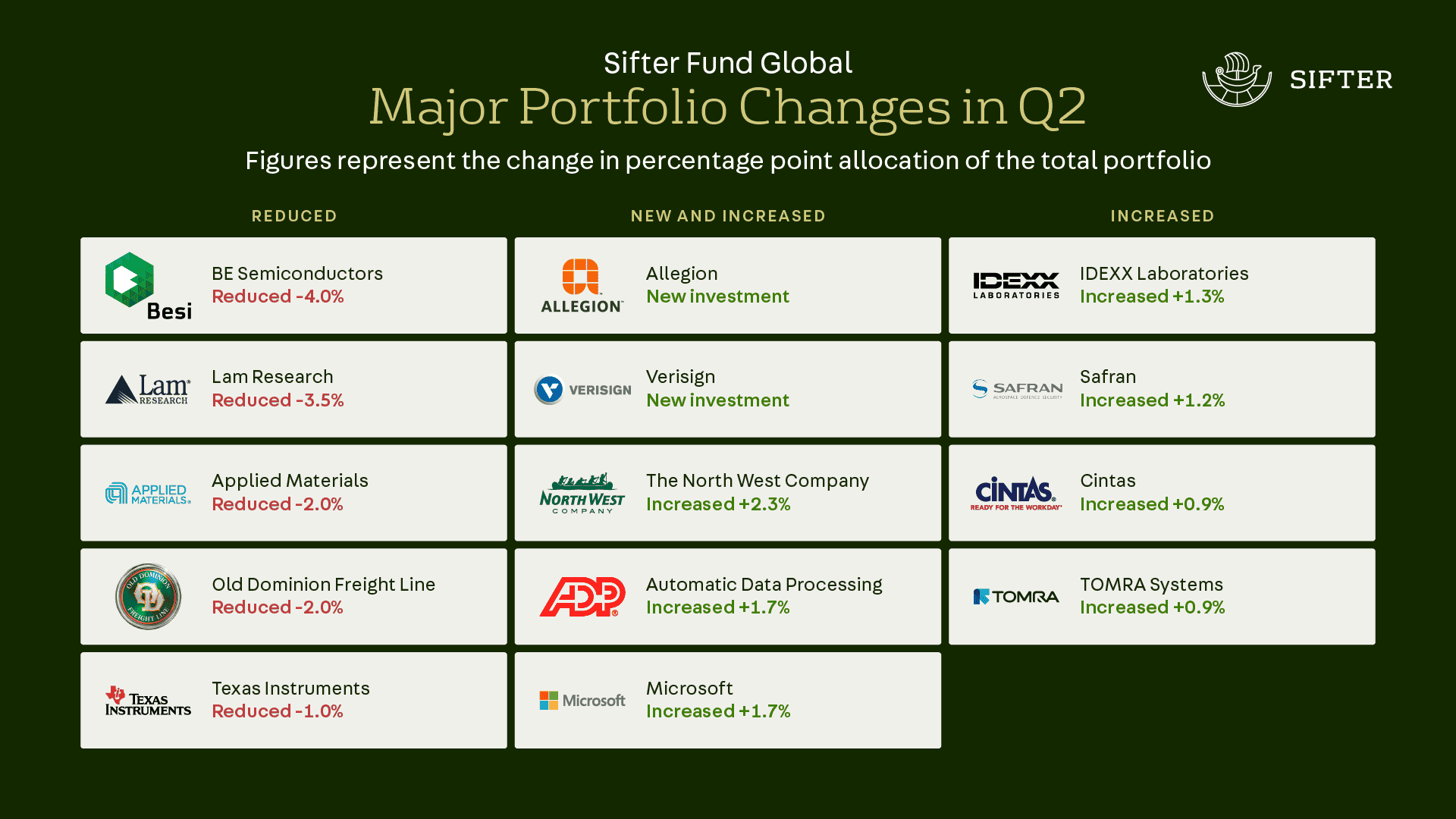

Portfolio Changes Q2/2026

During the second quarter we did not sell any company entirely, but we made two purchases and adjusted the weights of the portfolio’s holdings.

The new addition to the portfolio was Allegion, a US manufacturer of lock and security solutions. A familiar point of comparison is Assa Abloy, which is also Allegion’s main competitor. Assa Abloy operates internationally, whereas Allegion focuses on the US market, and it is precisely this focus that we like, because it improves the company’s predictability. The company earns stable revenue from institutional customers such as schools, hospitals and universities, even while construction activity is quieter due to interest rates.

We also brought Verisign back into the portfolio, having previously owned it from 2016 to 2024. Growth in the number of domain names is Verisign’s single most important metric. We sold the company back then, when growth in .com domain names turned to decline. Over the past four quarters, demand has turned back to growth, and we returned as owners of the company.

Verisign is a typical Sifter company. The business is capital-light, its market position is protected by contracts, it operates in a near-monopoly position, and it has high margins.

To offset the trimming of the semiconductor companies, we increased weights in, among others: North West, ADP, Microsoft, IDEXX, Safran, Cintas and TOMRA Systems. In these companies we currently see a better long-term risk-return profile than in the holdings we reduced.

Summary

The second quarter was strong. We trimmed our best performers because their valuation ran ahead of the business, and we shifted weight to companies where we see a better risk-return profile.

This is how we have operated for 23 years. We do not join every market narrative or chase hype, nor do we change our philosophy from one year to the next. The Sifter Fund’s return is built on discipline and on owning predictable, resilient businesses.

Company valuations have remained reasonable and earnings expectations strong, so we continue to see attractive potential in quality companies. That is why we are cautiously optimistic.

Discipline rarely shows in a single quarter. It shows over the years.

Santeri Korpinen

CEO