The Sifter Fund portfolio management team landed at Taipei Airport on the night of September 1st. Why did we want to spend a week in Taiwan at the Taiwan Semicon 2024 event? The reason is quite clear. Over 25% of Sifter’s portfolio is invested in semiconductor companies.

Sifter’s first investment in semiconductor companies was made back in 2013 when we invested in Taiwan Semiconductor. Now, we were heading to Taiwan Semicon 2024, the leading forum for the semiconductor industry, where all the major players from around the world were present.

The atmosphere was enthusiastic and at times very technical. What stood out the most was the strong sense of purpose within the semiconductor sector.

What else did we observe at the event?

1. Taiwan is the cornerstone of the semiconductor industry

Without Taiwan, the global semiconductor market wouldn’t function. This makes the stability of the country crucial for investors. The majority of the world’s most advanced chips are manufactured in TSMC’s factories in Taiwan. Because of this, the U.S. and Japan have taken Taiwan under their protection.

Geopolitical risks are always present, but the pressure from China towards Taiwan has been ongoing since the 1960s. So, nothing new for the Taiwanese.

Seminar presentations touched on geopolitical instability as a risk to the semiconductor industry, but China was not specifically mentioned. Instead, trade wars were seen as bigger threats, as they could harm the business of all companies operating within the semiconductor value chain.

2. The slowing of Moore’s Law opens doors to new innovations

The shrinking of chip size and the doubling of processing power is the foundation of Moore’s Law. Nvidia’s founder, Jensen Huang, has stated that Moore’s Law is obsolete. However, the chip engineers in Taiwan did not agree. They see Moore’s Law as a challenge that opens up opportunities for new innovations, such as improving energy efficiency and advancing chip packaging.

The seminar emphasized that modern chip packaging methods are playing an increasingly critical role in enhancing chip performance. The reason behind this is that improving chip performance using traditional front-end methods—like cramming more transistors onto the surface of silicon wafers through etching, deposition, and lithography—is becoming more difficult and expensive.

More efficiency gains are now being sought from modern packaging techniques, where chips are tightly connected side by side and stacked on top of each other.

For example, BE Semiconductor, a company in Sifter Fund’s portfolio, manufactures Hybrid Bonding equipment, positioning us in line with the growing trend of chip packaging technology development.

3. AI Development Drives Semiconductor Growth

The development of AI models requires massive computing power, which in turn drives demand for data centers and semiconductors.

Currently, the demand for AI chips accounts for nearly 70% of the growth in the semiconductor industry.

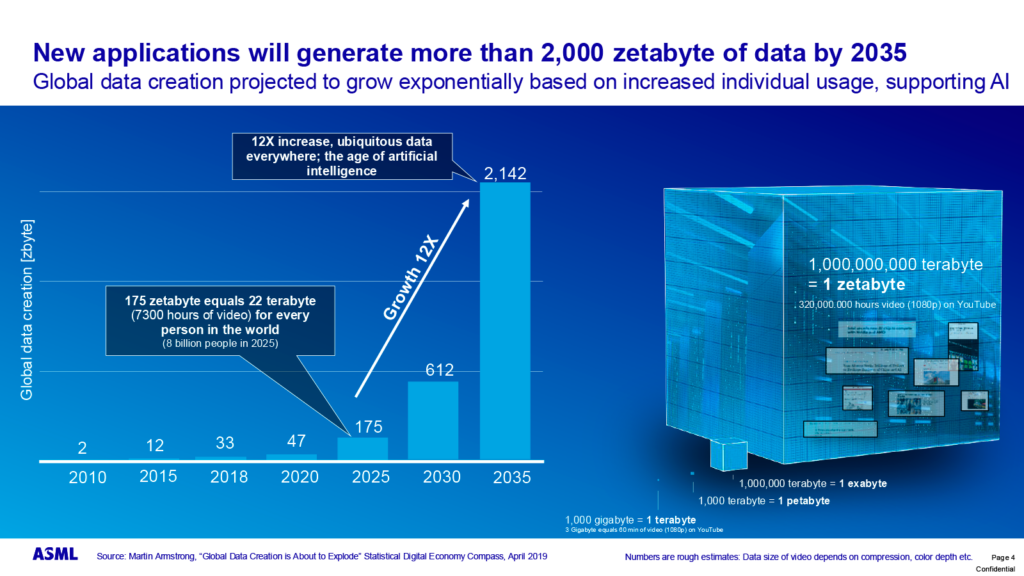

This presents both a risk and an opportunity. For example, a representative from the Dutch company ASML estimated that the amount of data will continue to grow exponentially and is expected to increase tenfold over the next 10 years. This long-term demand provides a sustainable growth platform for semiconductor companies. However, the risk lies in the possibility that confidence in AI development might decline, which could significantly reduce investment in the semiconductor industry.

4. “AI is a race of energy-efficient computing”

All players in the value chain are feverishly searching for solutions to reduce chip size, improve computing power, and, most importantly, lower energy consumption.

It’s estimated that 40% of a processor’s energy is used for cooling.

According to Gary Dickerson, CEO of Applied Materials, there is intense competition in the industry to reduce energy consumption. “AI is a race of energy-efficient computing,” said Dickerson.

5. TSMC’s dominance continues, and Nvidia is set to face competition

TSMC is the king of Taiwan. When TSMC’s leaders spoke at the forum, the seminar halls were packed, and everyone listened in silence. TSMC undeniably holds significant power, as they manufacture the world’s smallest and most advanced chips.

TSMC may also be starting to wield its power. Recently, TSMC has declared that modern chip packaging methods are now part of their strategic target market—alongside the traditional front-end processes.

Front-end processes still account for about 90% of TSMC’s revenue, but the role of back-end processes has become more prominent as the demand for AI chips grows rapidly.

In AI chips, modern packaging methods are crucial as they enable fast data transfer between the AI processor and its memory.

TSMC’s CoWoS packaging method has quickly become the standard for AI chips, and TSMC’s recent statements suggest they have no intention of relinquishing their strong position.

So far, TSMC has been cautious with price increases. As investors, we would like to see them leverage their power more in pricing.

For example, Nvidia takes the lion’s share of the profits from the GPUs they design, while TSMC manufactures them. Recently, TSMC’s tone has shifted, hinting that price increases for Nvidia’s GPU chips could be on the horizon. Nvidia may soon face competition from its own customers.

It may only be a matter of time before companies like Microsoft, Meta, or Alphabet are able to design their own processors similar to Nvidia’s. While there are no concrete facts to support this yet, Nvidia’s chips are so expensive that it’s likely these giant companies won’t want to pay such high prices in the future.

6. Semiconductor Manufacturing Capacity is Globalizing

The U.S. tech giants (Microsoft, Meta, Alphabet, and Amazon) are heavily investing in data centers and AI development, as none of them can afford to fall behind.

By 2025, these four companies alone have announced plans to invest $190 billion into AI-driven data centers.

These massive investments mean that the production capacity, equipment, and services for semiconductors must expand.

By 2027, it’s estimated that U.S. fab investments (excluding data centers) in production capacity will increase from $22 billion to $33 billion, while Europe will rise from $10 billion to close to $20 billion. The risks of trade wars, protectionism, and rising demand are driving the globalization of semiconductor manufacturing capacity.

7. Will Massive AI Investments Pay Off?

One of the hottest topics seems to be on-device AI, meaning how to integrate AI into end-user devices like phones, cars or any other electronic machines.

It’s estimated that the greatest value will be generated where new services and revenue models are created, not in the infrastructure itself.

This is where the big hyperscalers, like Microsoft and Alphabet, are focusing their efforts. The media and investors are concerned that there may not be a return on these massive investments. Forum speakers urged patience, stating that the infrastructure is being built first, and then the applications, services, and commercial ventures will follow.

Will investors’ patience last? That remains to be seen.

8. Winners and Losers in the Semiconductor Industry

The semiconductor industry is evolving and shifting at an incredibly fast pace. It is almost impossible to predict which technology will dominate three, five, or ten years from now. However, we believe it’s relatively safe to invest in companies that are the largest players in their niche and have a long learning curve in product design or manufacturing.

Currently, the winners in the semiconductor industry have been companies that design chips, such as Nvidia, and manufacturers like TSMC. Additionally, companies that produce chip-making equipment, such as ASML and Applied Materials, have also performed well

But what about the losers? U.S. tech giants are investing $190 billion in developing data centers and AI because no one dares to stay on the sidelines. It’s highly likely that over-investments will happen, and investor money will be lost—or it will shift to Asia, where chips are manufactured. Some of these companies may burn through their cash without seeing a return on their investments.

It’s also highly likely that countries that fail to invest in semiconductor development will fall behind in global growth. At worst, the rest of the world could become dependent on the policies of these countries and companies, similar to what has happened with Russia and China. China, however, will not accept this role.

China has been the world’s largest investor in AI chip and fab development and infrastructure in recent years and is certain to continue down this path. The U.S. and Europe have finally woken up to this reality as well.

Interestingly, there was no talk of politics at the event. All nationalities seemed to breathe the same semiconductor air. Trade policy was only briefly mentioned as a risk in a few presentations.

9. Should an Investor Attend Technical Conferences?

We asked ourselves this question several times while listening to semiconductor PhDs give atomic-level presentations. On the other hand, some of the talks provided great insight into where the industry is headed, which topics are trending, and how companies present themselves. Just seeing how the industry is growing and evolving was worth it.

Our portfolio management team was satisfied with the content of the conference. They have been following, researching, and investing in semiconductor companies for years.

Currently, we are invested in six semiconductor companies, with about 25% of the Sifter Fund’s assets tied up in these companies. For this reason alone, it’s essential to keep learning more.

There’s no point in investing based solely on the news. You need to understand better what is being discussed in the industry, what’s significant, and what’s just noise. Which semiconductor companies are likely to be future winners? You won’t find that in Bloomberg’s tools.

10. Semiconductor Industry Outlook from an Investor’s Perspective

Investing in semiconductor companies is not easy, for several reasons. It’s hard to understand what these companies actually do and what their competitive advantages are.

Comparing numbers and stock prices is simple, but numbers only reflect the past and the market’s expectations.

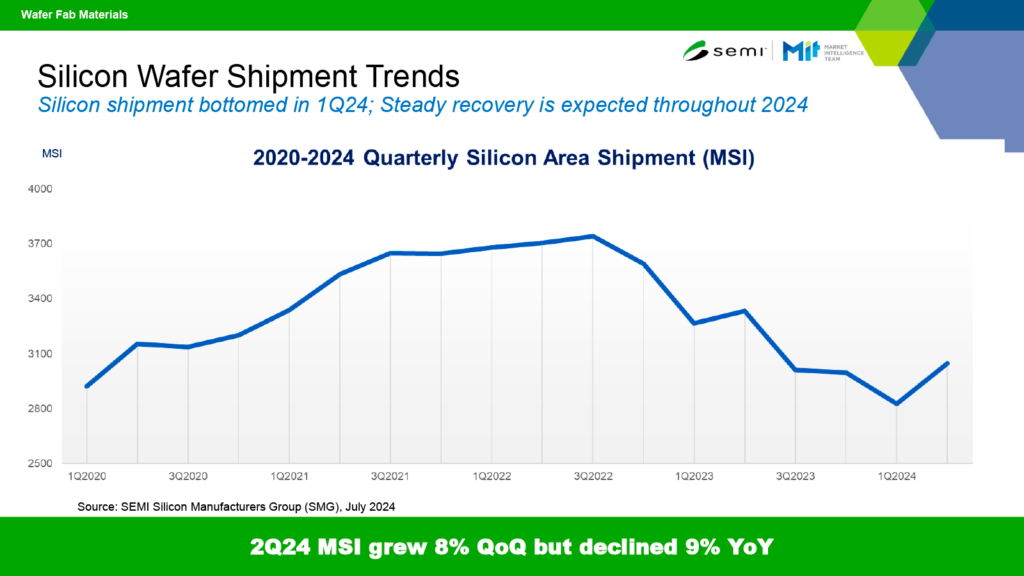

The fundamentals of the semiconductor industry follow a very different cycle compared to the stock market. For instance, in 2023 and the spring of 2024, the business figures of the semiconductor sector were extremely weak—essentially at the bottom of the cycle. Yet at the same time, many chip companies’ stock prices were soaring.

However, estimates suggest that 2025 is expected to be a record year for these companies, in terms of both revenue and profits.

More factories are being built outside of Asia, and equipment manufacturers are seeing increased orders for semiconductor manufacturing machines. It will be interesting to see how the stock market reacts to this, or whether the expected results for the peak year of 2025 were already priced into the spring 2024 stock prices.

What’s certain is that the semiconductor industry is experiencing a massive boom, benefiting nearly all players and driving global economic growth.

The companies with the best positions in the value chain are set to rake in huge profits in the coming years, and if the experts are to be believed, this growth is just getting started.

Santeri Korpinen

CEO