In January 2025, we invested into Cintas. At first glance, Cintas looks like the least exciting business you could imagine – it’s core business is essentially renting out uniforms and picking up dirty laundry. But under the hood, this low-glamour company has become a true compounding machine.

Sifter Fund focuses on companies with predictable growth, strong moat, and solid financials. Cintas demonstrates all three.

With steady earnings compounding, industry-leading margins, and consistently high returns on invested capital, it exemplifies the kind of predictable long-term compounder we seek for the Sifter portfolio.

Learn how Cintas turned ordinary laundry into extraordinary long-term returns and why we decided to invest in it?

How does Cintas make money?

Cintas, based in the United States, serves over one million customers nationwide. The company earns most of its revenue through recurring contracts, supplying businesses with uniforms and facility services.

For a regular fee, Cintas delivers, picks up, washes, repairs, and replaces workwear, providing customers with a reliable, cost-efficient solution to an essential need.

A service that saves companies the hassle and cost of doing it themselves.

Download Cintas Research Note (PDF)

Because Cintas drivers visit customer locations once or twice a week to replace uniforms, the company is in a unique position to offer much more than just laundry services.

Recurring contracts and broad cross-selling create the stable, scalable, and highly profitable business model that has powered Cintas’s long-term compounding.

With little additional cost, drivers can deliver and maintain a wide range of essentials that businesses need anyway, from entry mats and stocked first aid cabinets to clean shop rags, restroom supplies, fire extinguishers, and even safety alarms.

This model turns each route into a growth engine: uniforms form the recurring foundation, while add-on products and services create high-margin opportunities.

The result is a business that not only scales efficiently but also deepens customer relationships, making Cintas an indispensable partner in daily operations.

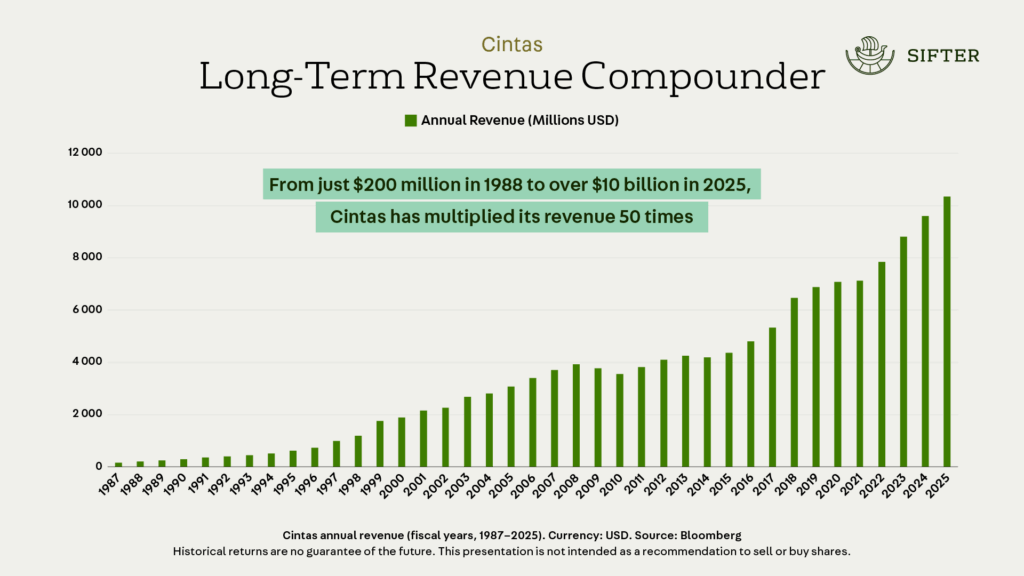

How Cintas Compounds Growth Over Decades

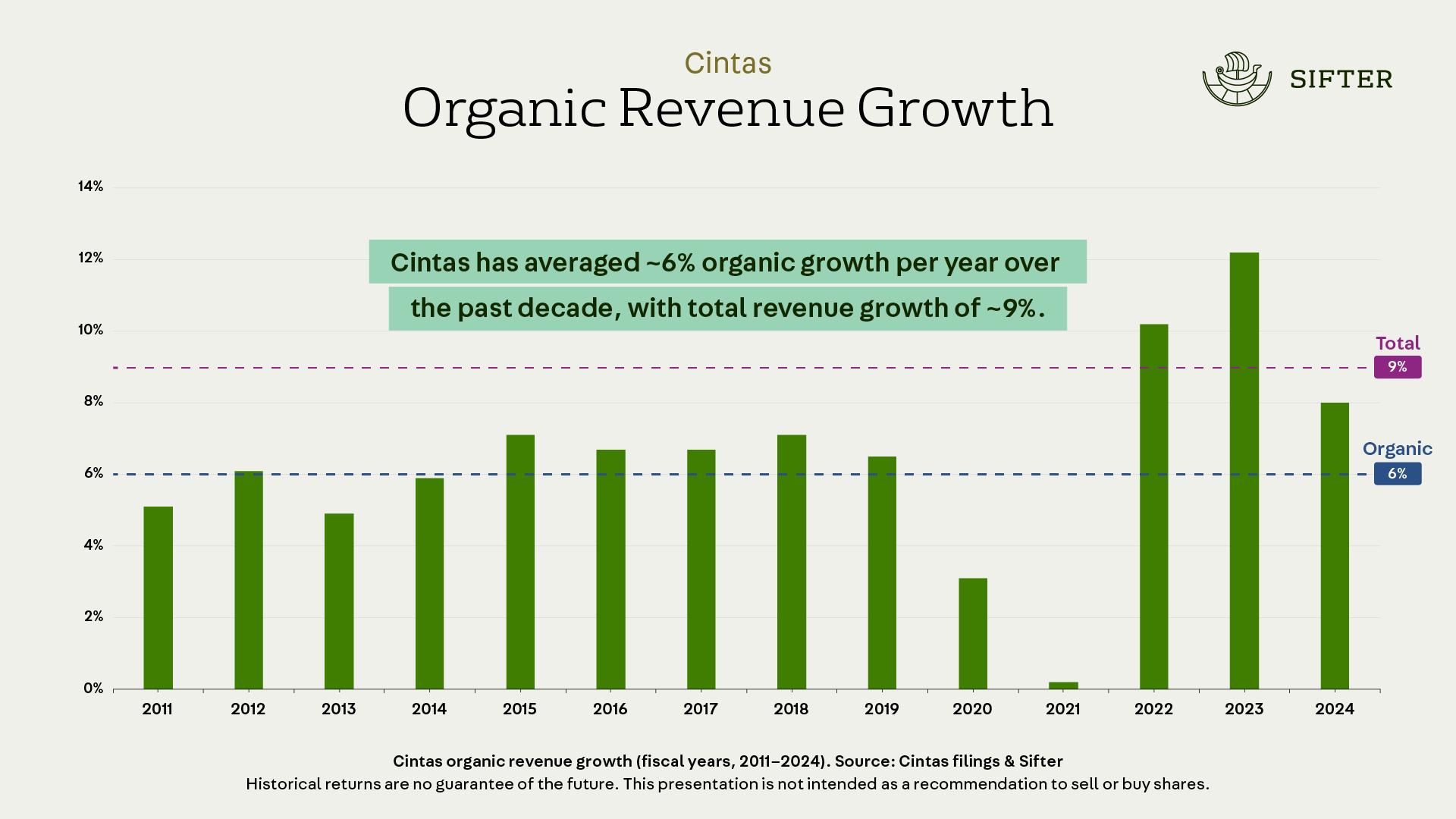

Cintas has delivered growth through a combination of steady demand and smart execution. The growth comes from many sources.

Uniform users: Expanding workforces add about 1% to annual growth as the number of uniform users increases.

New contracts: Securing new customer agreements adds another 1% to yearly growth across the business.

Pricing power: Raising prices above inflation without losing clients contributes steadily to growth.

M&A Acquisitions: Beyond organic growth, Cintas regularly acquires smaller local competitors. These acquisitions expand its footprint and allow the company to apply its scale advantages in new markets.

The result is a layered growth model: incremental gains from new users and contracts, pricing strength, and strategic acquisitions.

Moat and Competitive Edge

Cintas’s long-term success is built on a moat formed by scale, network density, efficiency, and culture. Advantages that smaller competitors struggle to replicate.

Scale Advantage & Network Density

With the largest market share in a fragmented industry, Cintas benefits from dense customer networks. The more clients it serves in one region, the lower the delivery costs per stop. This local scale advantage gives Cintas superior unit economics compared to smaller rivals.

Cintas can either keep prices lower to win business or maintain higher margins while competitors struggle to match profitability.

Operational Efficiency

Decades of process optimization, from laundry facilities to routing algorithms, have made Cintas exceptionally lean. Leveraging data and logistics expertise, the company reduces costs and improves service reliability, reinforcing its advantage year after year.

Culture of Continuous Improvement

Cintas’s culture treats employees as “partners” who are incentivized to upsell additional services during their regular customer visits. This mindset combines frontline entrepreneurship with disciplined cost control, boosting productivity and deepening customer relationships.

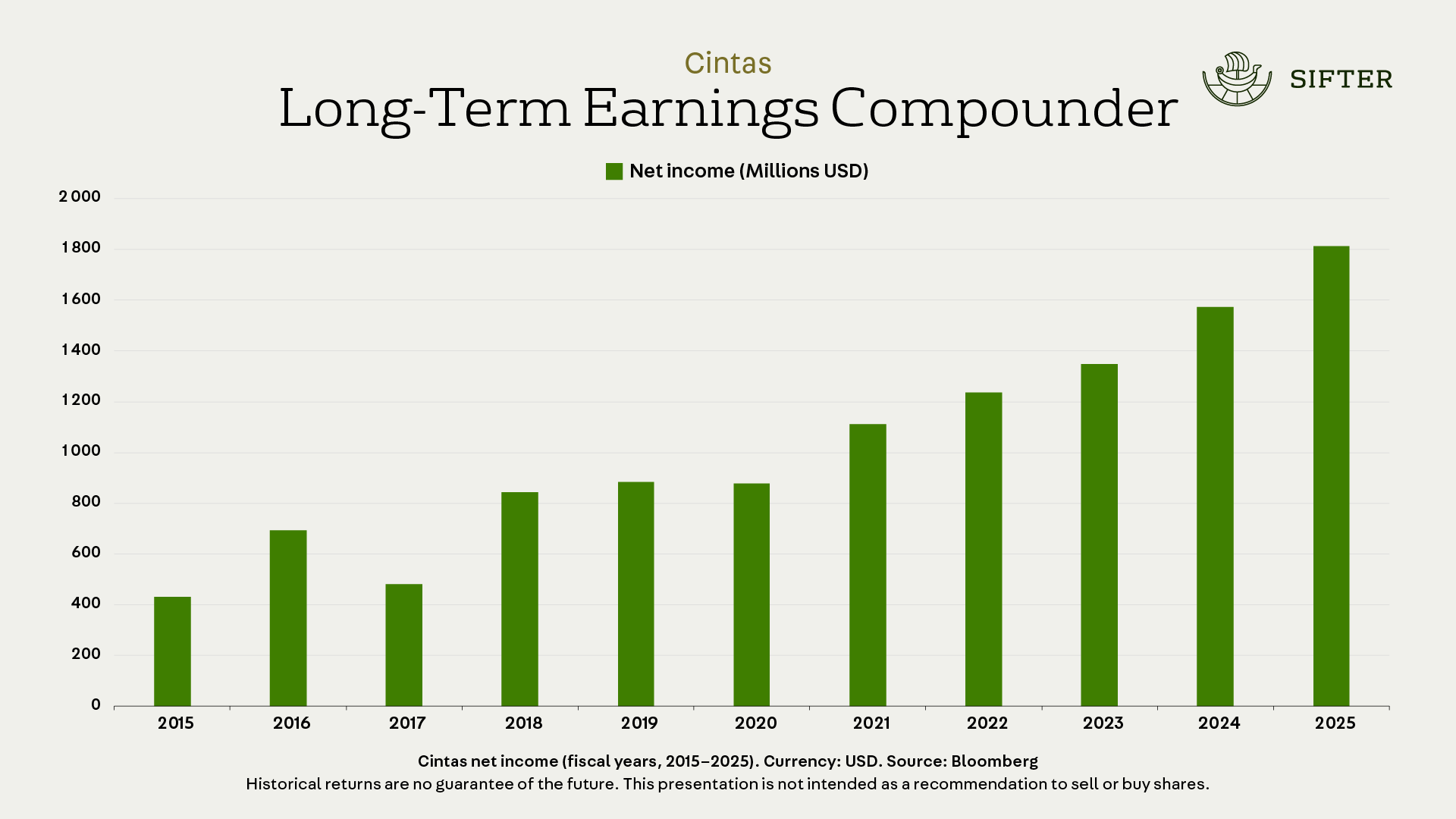

Business Results

The competitive edges of scale, efficiency, and culture translate directly into Cintas’s financial results. Over time, the company has expanded its margins, increased returns on invested capital, and steadily compounded earnings. Productivity at the employee level also demonstrates its operational strength.

Download Cintas (CTAS) Research Note (PDF)

At Sifter Fund, we focus on conducting high-quality research and analysis before making any investment decisions. We value transparency and seek to highlight the diligence of our investment process by sharing our comprehensive research notes with our investors.

Do you want to know what a quality company analysis looks like?

Download the Cintas Research Note

Why We Invested in Cintas

We invested in Cintas because it embodies the qualities we seek in a long-term compounder: predictable growth, a strong moat, and solid financials.

For decades, the company has steadily grown earnings at around 10% per year, supported by recurring uniform rental contracts and high-margin add-on services.

Its scale advantage, operational efficiency, and strong culture create barriers that smaller rivals cannot easily replicate.

These competitive strengths translate into industry-leading margins, ROIC, and consistent earnings compounding.

With a large and fragmented market still ahead, Cintas has both the resilience and the runway to continue creating shareholder value. That combination makes it a high-quality business and a natural fit for the Sifter portfolio.

Alexander Järf

Portfolio Manager