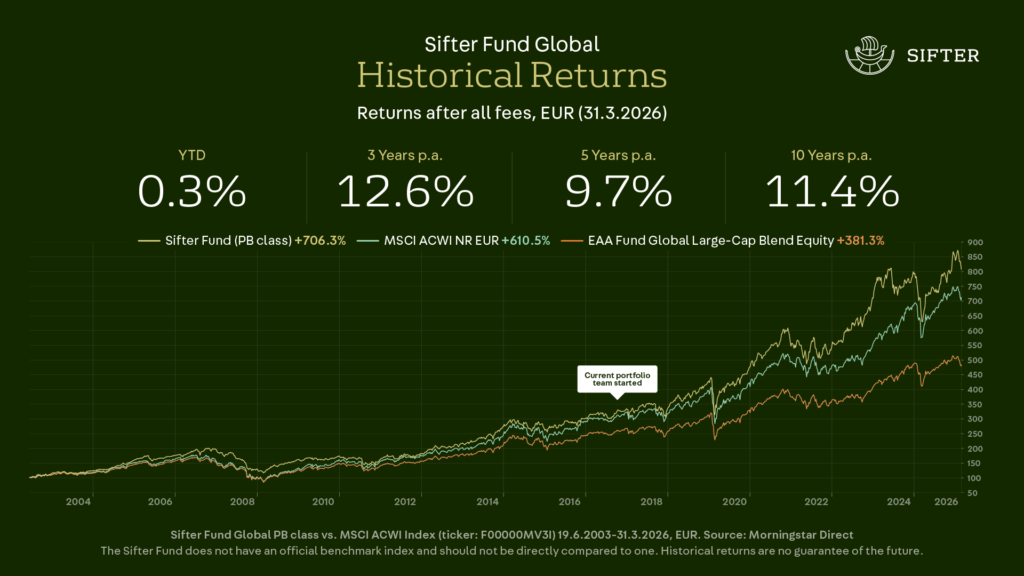

The first quarter started strongly, but in March, the escalation of the situation in Iran wiped out a large part of the year’s early gains. The Sifter Fund PB class returned +0.3% in the first quarter of the year. A modest but positive result in a fast-moving market.

Sifter Fund Return in Q1/2026

The Fund outperformed the global equity index (MSCI ACWI) by approximately 3 percentage points. The short term is, however, a poor measure of how well a strategy is working. Longer time periods tell a more complete story.

Over its 23-year history, the Sifter Fund has returned 710% (PB class) after fees. The Fund has outperformed the global equity index (MSCI ACWI) by 105 percentage points and has clearly outperformed the peer group average (EAA Fund Global Large-Cap Blend Equity).

Top Performers in Q1/2026

The share price gains were driven by an accelerating AI investment cycle. Large cloud companies such as Alphabet, Amazon, and Meta guided their capital expenditure 50-100% higher compared to 2025.

Semiconductor demand exceeded supply, and memory chip prices also remained elevated.

At the start of the quarter, Sifter held approximately a 20% allocation to the semiconductor equipment and materials sub-sector. The equivalent weight in the benchmark index is around 2%.

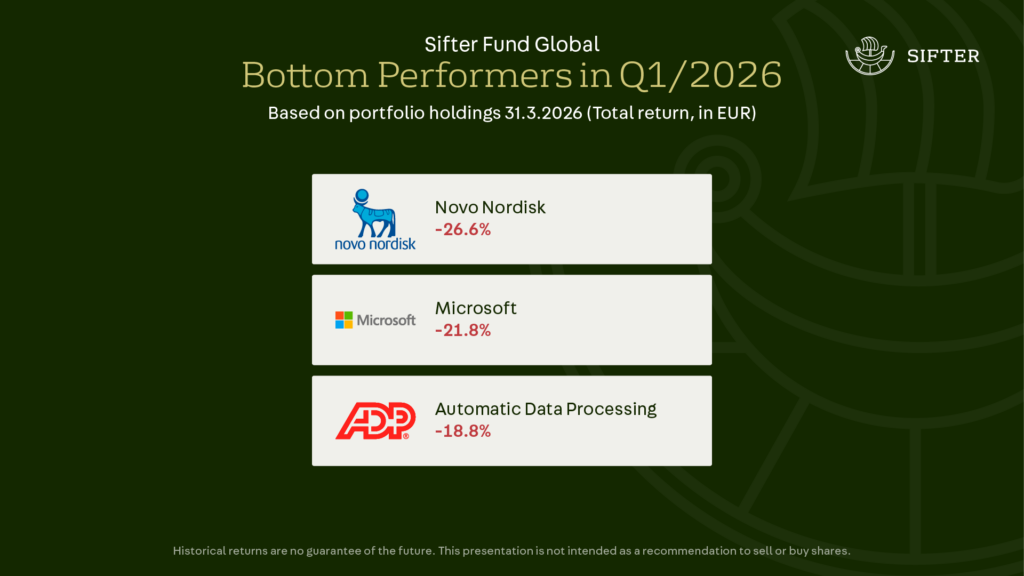

Bottom Performers in Q1/2026

Novo Nordisk appeared on the bottom performers list once again. It is worth noting that Novo’s weight in the Sifter portfolio is now only around 1%. We reduced the position further during Q1 and are considering closing it entirely.

The reason for Novo’s decline was company-specific. The results of its next-generation weight-loss drug in its own clinical trials fell short of those of competitor Eli Lilly, significantly increasing uncertainty around the long-term outlook.

The share price declines of Microsoft and ADP reflect a broader concern: could AI disrupt the position of software companies? Neither company’s reported numbers nor management guidance shows any signs of concrete damage so far.

In Microsoft’s case, AI does not appear to be an existential threat. The company’s software forms a broad ecosystem, and it provides critical infrastructure. AI could even increase the utilisation of Microsoft’s data centres and thereby strengthen the company’s position over the long term.

ADP provides payroll-related software. The processes it handles can be classified as mission-critical, and they are unlikely to be among the first to be replaced by AI agents.

Is AI a Threat or an Opportunity for Software?

The answer depends on the company.

Companies offering narrow applications are clearly more vulnerable than those with broad, interconnected ecosystems. A narrow application can be thought of as software that does only one thing – Duolingo, for example, could be considered one. It is easy to replace, and the risks of doing so are practically non-existent.

In our view, the best-positioned companies are those that offer not only software but also databases and platforms – the infrastructure on which applications are built. These companies could actually benefit from AI as overall productivity increases.

Because predictability is a central requirement for Sifter, we have not invested in new software companies in recent years.

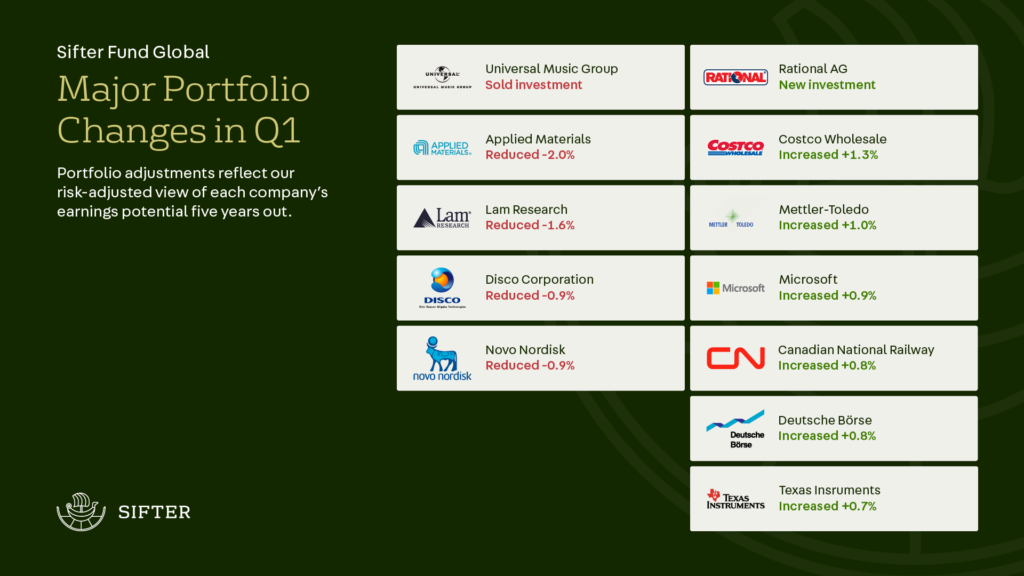

Portfolio Changes in Q1/2026

In early February, we sold Universal Music Group entirely. The impact of AI on the music industry was already visible in reported numbers, and the long-term predictability of the business no longer met our criteria.

In its place, we initiated a position in Rational AG – the global market leader in professional combi ovens, with a predictable business model and strong financials.

We also reduced our semiconductor positions as valuations rose and reallocated capital to industrial companies and several other portfolio holdings where we saw a more attractive risk-return profile.

Summary

The first quarter served as a reminder of something important: markets can move a great deal in the short term, but over time, high-quality businesses do the work.

The Sifter Fund’s outperformance is built on discipline. We do not follow every market narrative or chase hype. Instead, we invest in predictable, resilient businesses where the risk-return profile holds up over the long term.

Our portfolio is built on quality, not the index. We continue to see attractive potential in quality companies. Valuations are reasonable and earnings growth expectations remain strong. That is why we are cautiously optimistic.

In simple terms, we want to own companies with strong competitive advantages, solid cash flow, and the ability to generate earnings even in more challenging environments.

Santeri Korpinen

CEO, Sifter