The third quarter brought renewed strength to global equity markets and particularly to the semiconductor sector. Sifter Fund delivered a +3.5% return in Q3, bringing the year-to-date performance to +0.3%. (PA class, 30.9.2025)

While the quarterly numbers show progress, we continue to emphasize the long-term perspective — the cornerstone of our investment philosophy.

Please note that past performance is not indicative of future results.

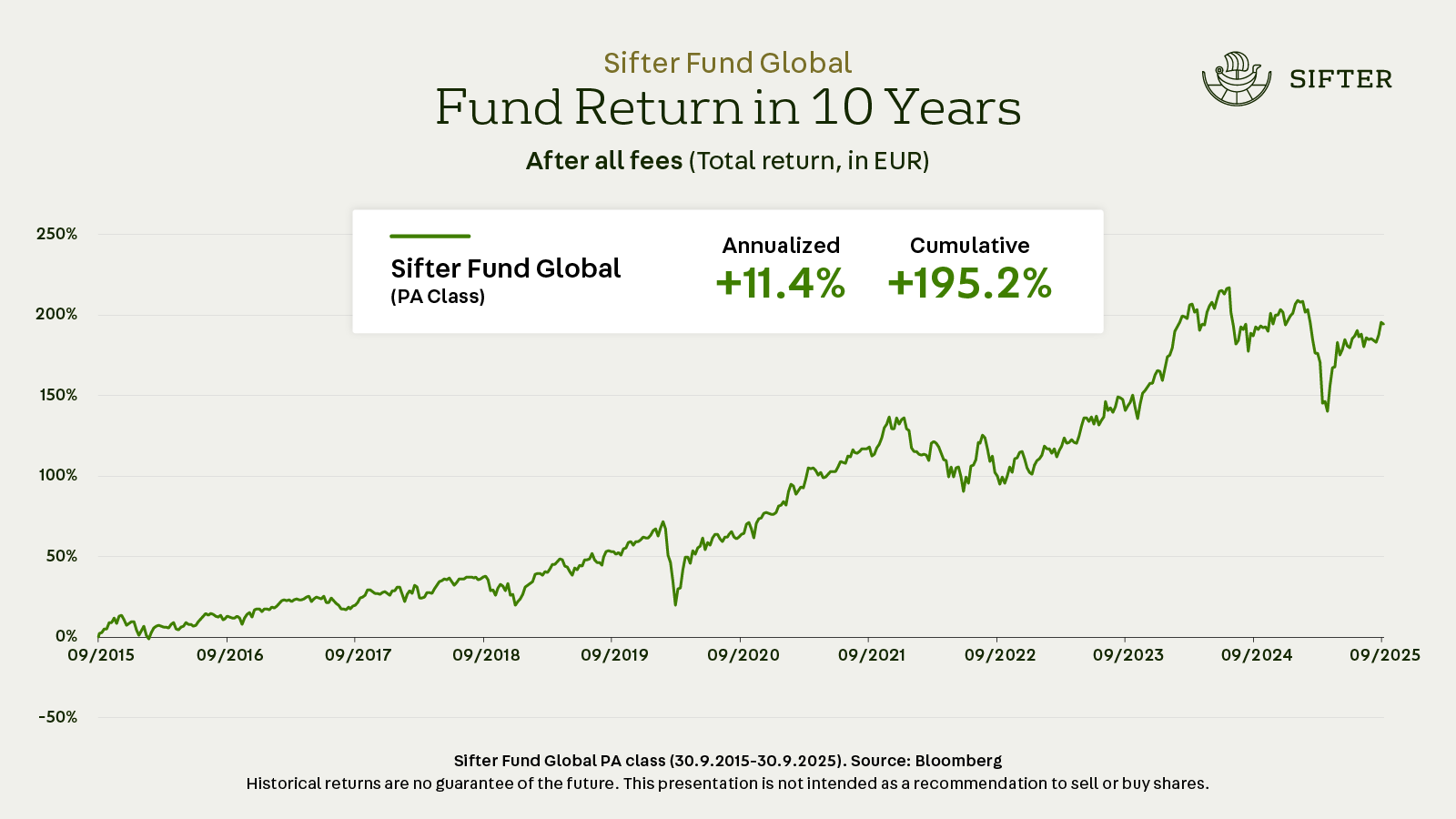

Patience Rewards Long-Term Quality Investor

When returns are viewed through a short-term lens, frustration comes easily — and understandably so. Markets can feel unpredictable, even unfair at times.

But when we zoom out, a different picture emerges.

More importantly, those numbers tell a story of perseverance of quality companies quietly growing stronger, even when markets stumble. It’s a reminder that true progress in investing doesn’t happen in months, but over years, and that time continues to reward patient owners.

Top Performers in Q3

Alphabet

Alphabet rebounded strongly after a favorable ruling in the long-running antitrust case, which turned out to be milder than expected. At the same time, Google’s advertising and cloud businesses continue to grow steadily. The company remains well-positioned in AI — not as the disruptor, but as a key enabler through its massive data assets, YouTube, and cloud infrastructure.

Lam Research

Semiconductor companies saw a clear turnaround this quarter after a weak start to the year. Lam Research, which supplies equipment essential for chip manufacturing, benefited from recovering demand and renewed investment confidence in the U.S. semiconductor industry. Policy support and steady end-market demand have improved the outlook for the entire sector.

TSMC

The world’s leading chip manufacturer continued to ride the global AI investment wave. Although we reduced our stake last year to manage geopolitical risks related to Taiwan, the company remains a core holding thanks to its exceptional profitability and technological leadership.

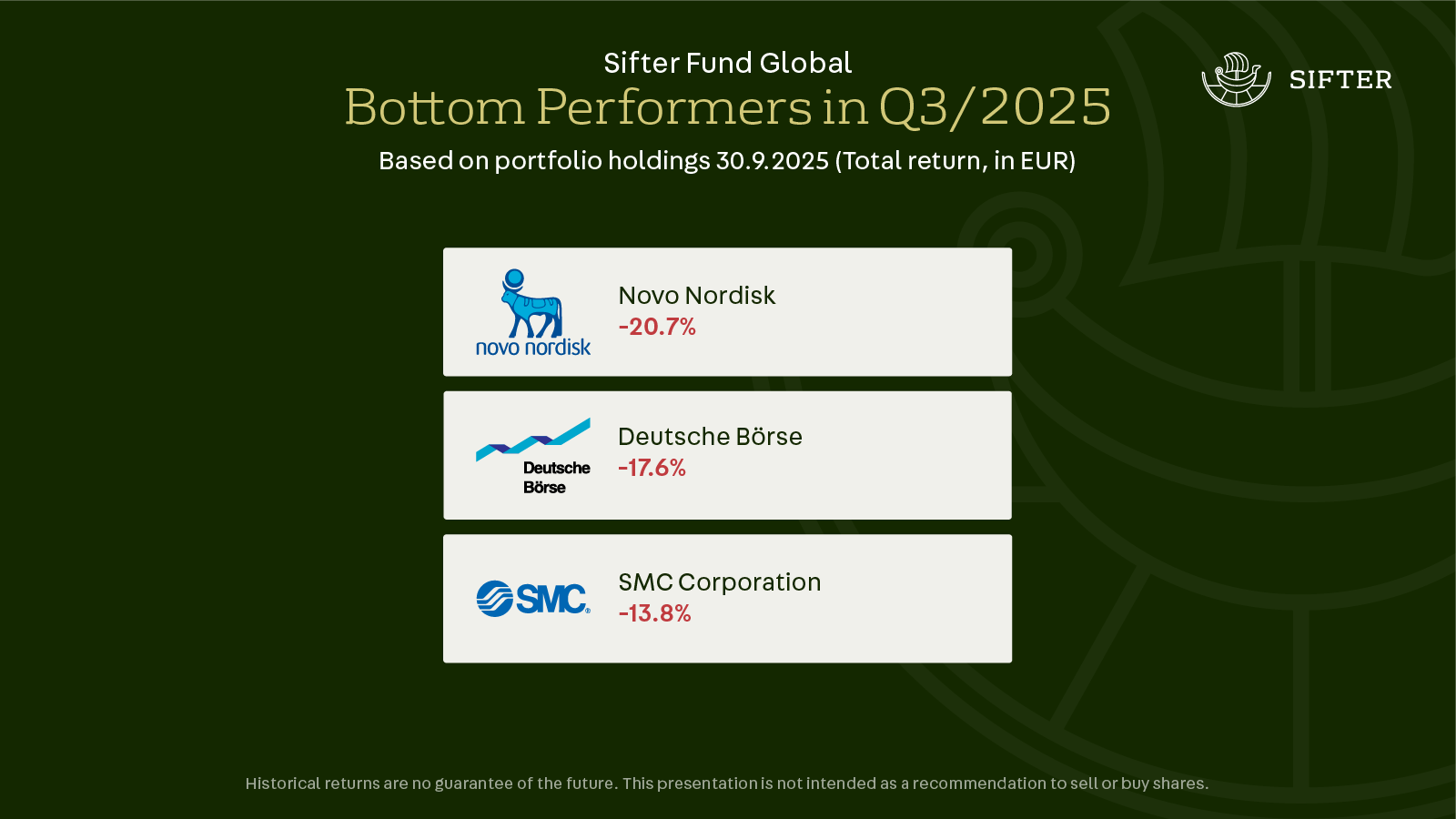

Bottom Performers in Q3

Novo Nordisk

Novo Nordisk faced a difficult quarter, issuing a profit warning and changing its CEO amid the growing challenge from U.S. compounding pharmacies producing unregulated versions of its GLP-1 drugs. While this has temporarily hurt results, we believe the issue will be resolved. Novo’s valuation is now attractive, and we slightly increased our position during the correction.

Deutsche Börse

After a strong first half, Deutsche Börse’s share price softened as market volatility declined and investor flows into Europe normalized. The company’s long-term fundamentals remain unchanged, driven by stable service revenues and regulatory trends that could support European capital markets over time.

SMC

The Japanese automation company has continued to face a sluggish industrial cycle. We expect gradual recovery as industrial spending picks up, supported by onshoring and infrastructure investments in Western markets.

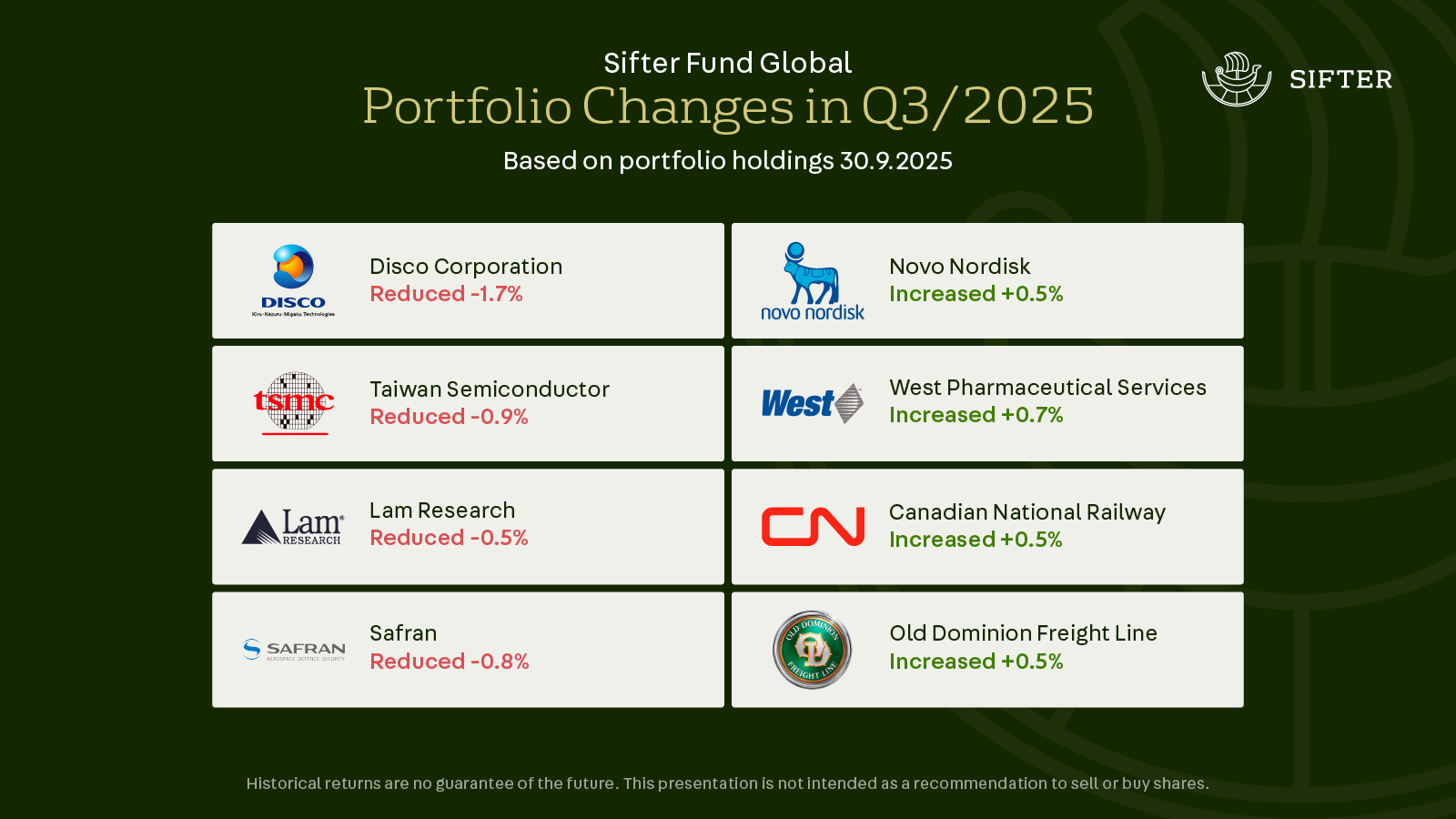

Portfolio Changes in Q3

We reduced slightly positions in Disco, TSMC, Safran, and Lam Research because of their strong stock price performance and regulative reasons.

We reallocated capital to Novo Nordisk, West Pharmaceutical Services, Canadian National Railway, and Old Dominion Freight Line — companies where fundamentals remain solid but recent price weakness improved expected long-term returns.

Santeri Korpinen

CEO