Universal Music Group, or UMG, is one of Sifter Fund’s latest investments. The company entered Sifter’s portfolio in January 2022, but why did Sifter invest in it? In short, UMG operates in a growing market, generates predictable and improving results, has sustainable competitive advantages, and it is available at a reasonable price.

UMG is a Dutch-American music company that was spun off from the French media group Vivendi in 2021. This article will explain how UMG makes its money and what its strengths are.

How does Universal Music Group (UMG) make its money?

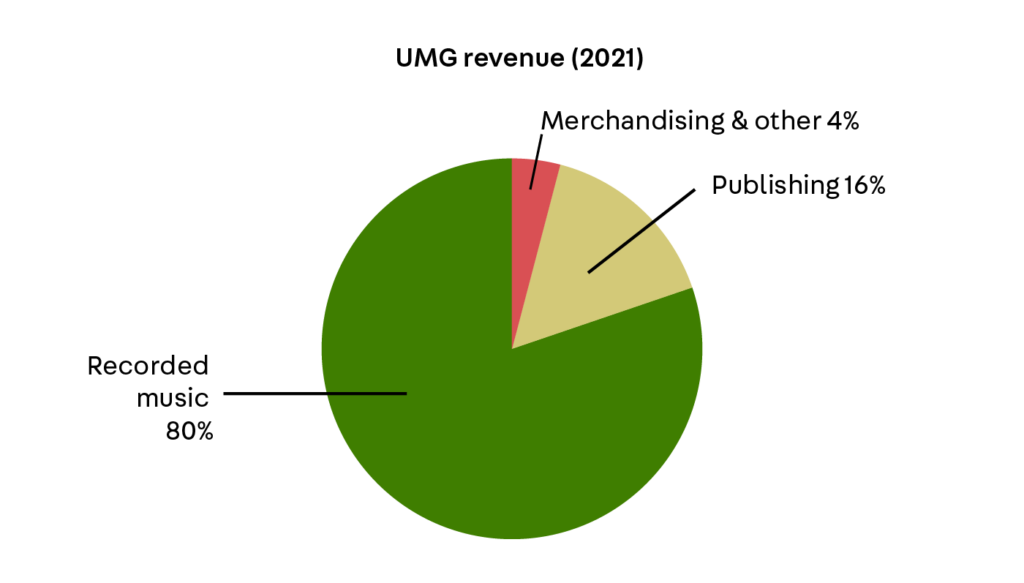

Overall, UMG’s business is to represent artists, songwriters, and composers.

By far the largest portion of UMG’s revenue, about 80%, originates from representing artists. That business is called Recorded Music.

Essentially, UMG operates as a record label, discovering and developing artists. In practice, UMG helps the artists succeed by offering them recording studios, expertise, marketing resources, and contacts.

In return for these investments and risk-taking, UMG typically signs a contract with the artist, granting UMG the copyright to the music recordings that the artist creates. Typically, those contracts cover several albums.

A copyright can be very valuable because the best songs are listened to over and over again. Or have you ever heard someone say “That’s a great song, but please don’t play it, I’ve heard it before.”?

Once the music recordings are created, UMG offers them to distributors and collects income from them. By far the largest source of that income originates from streaming, including services like Spotify, YouTube, and Apple Music. The rest originates from physical and digital music sales, public performances as well as commercials, movies, and social media.

UMG collects income from these various sources and shares some of it with the artist. UMG also compensates the original songwriter and composer for the use of their work.

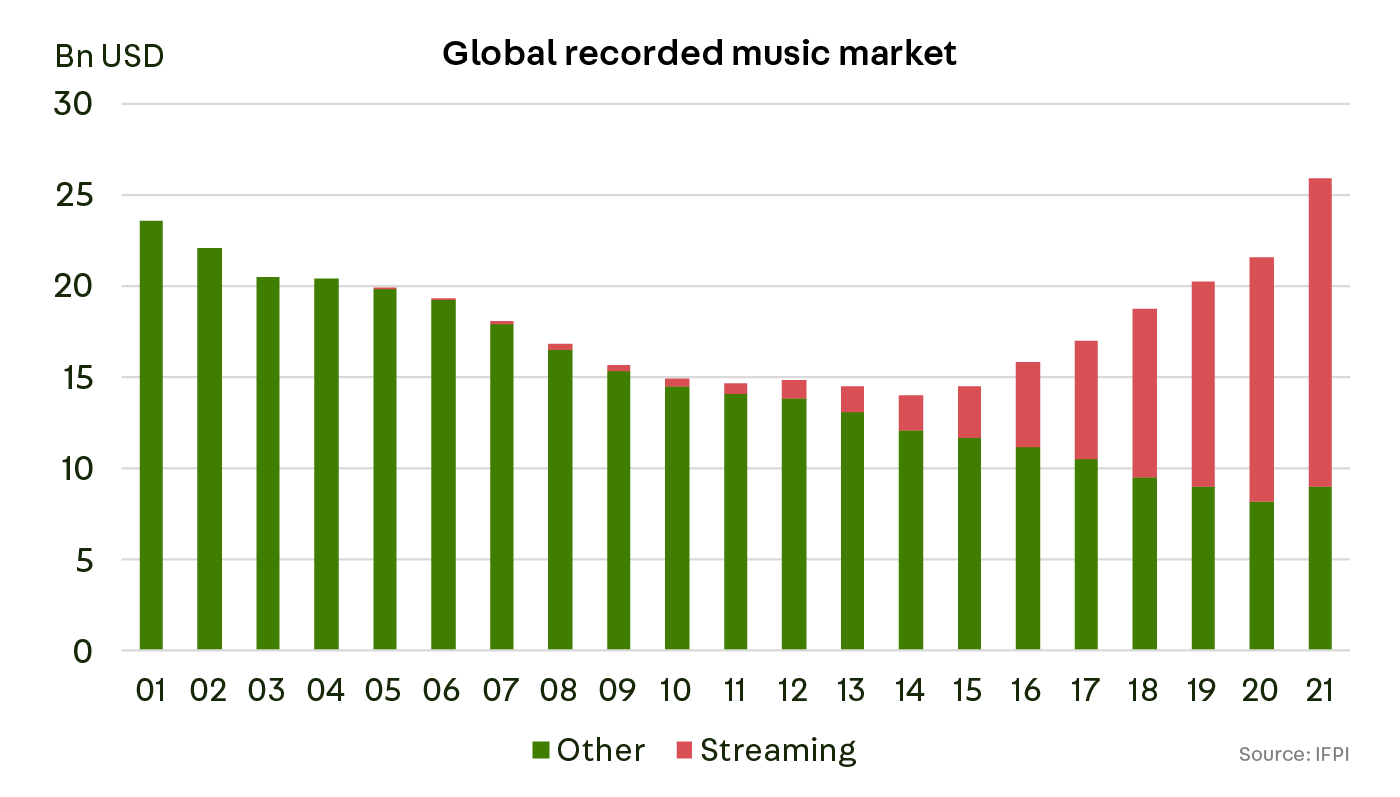

Streaming is driving growth in the recorded music market

The global market for recorded music has been quite a roller coaster. Since the early 2000s, the market was undermined by online piracy. However, since 2015, the market has been growing again, driven by streaming.

This is because streaming offers an exceptionally convenient way to enjoy music: for a fixed monthly fee, the consumer has access to an unlimited amount of music, while algorithms continuously offer content that best fits the consumer’s taste.

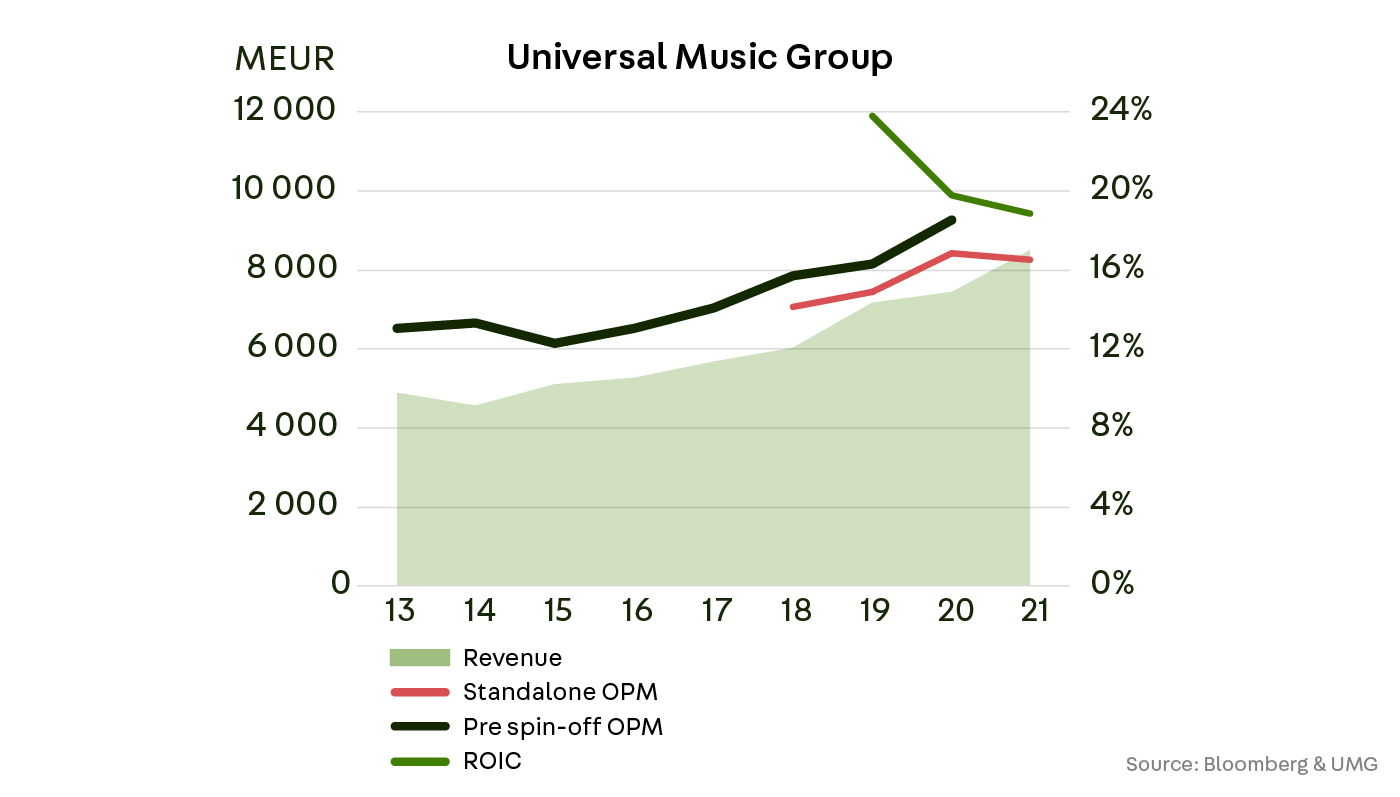

UMG has a healthy financial track record

What initially drew our attention to UMG? At first, we noticed its quantitative strengths.

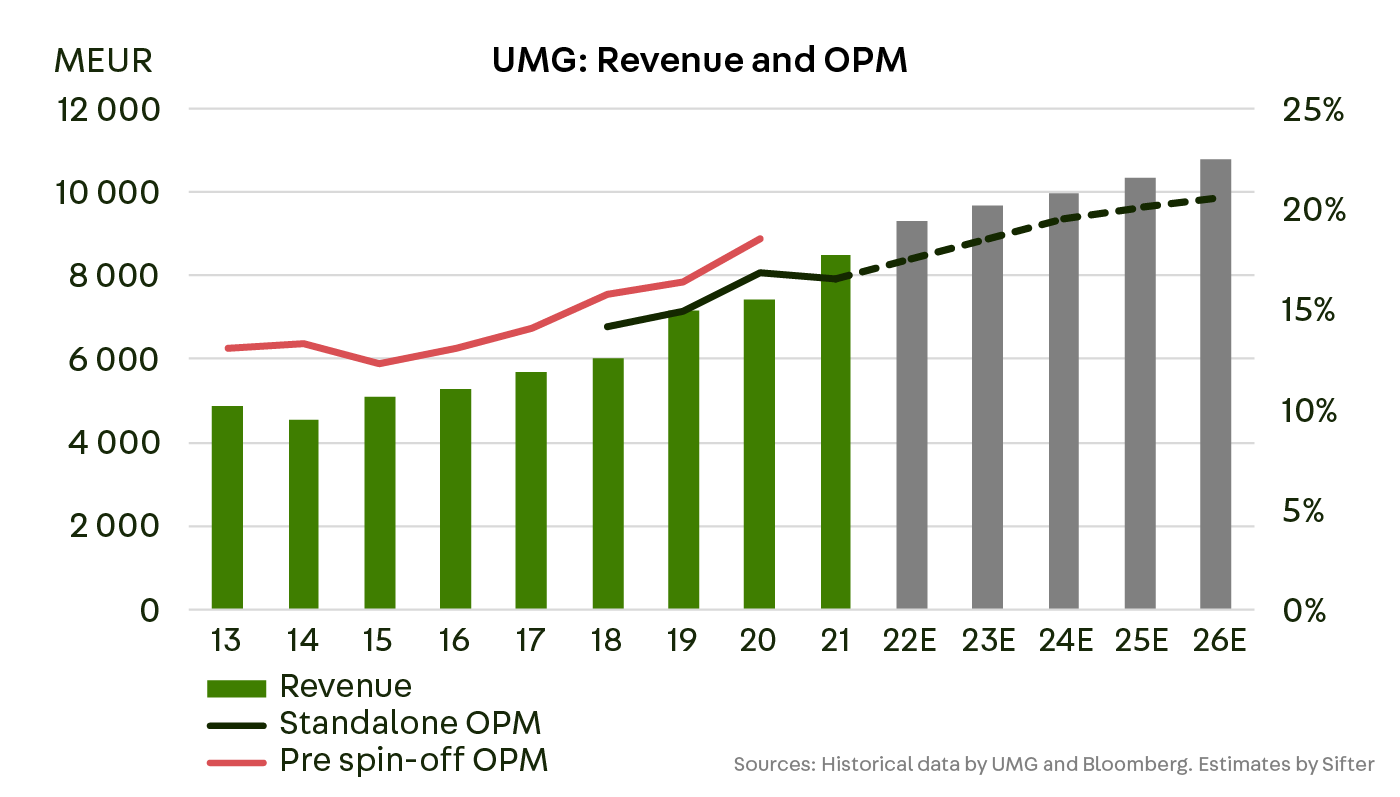

By 2021, UMG’s revenue has grown at a ca. 10% annual rate over the past five years, and that growth has been mainly organic. Meanwhile, UMG’s operating margin has improved for many years in a row, driven by economies of scale.

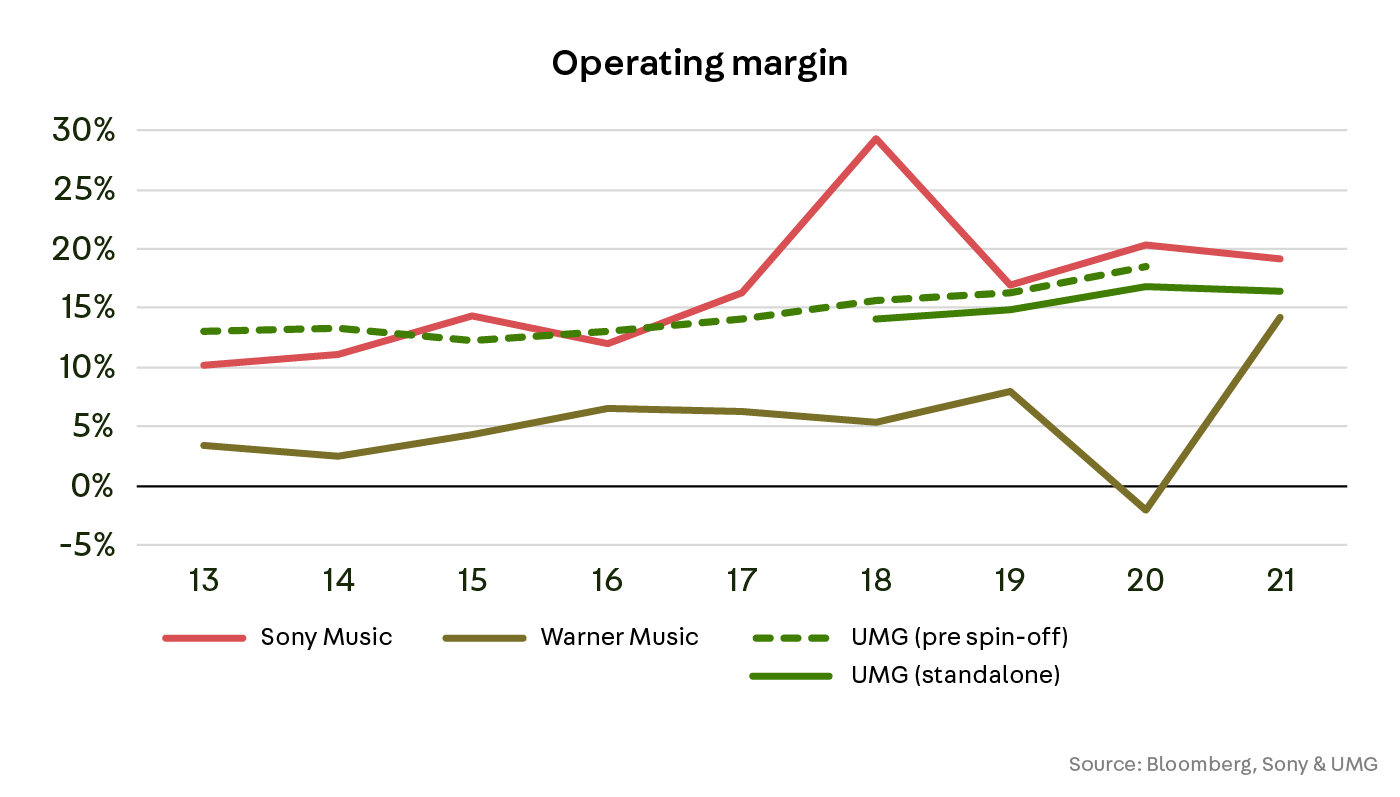

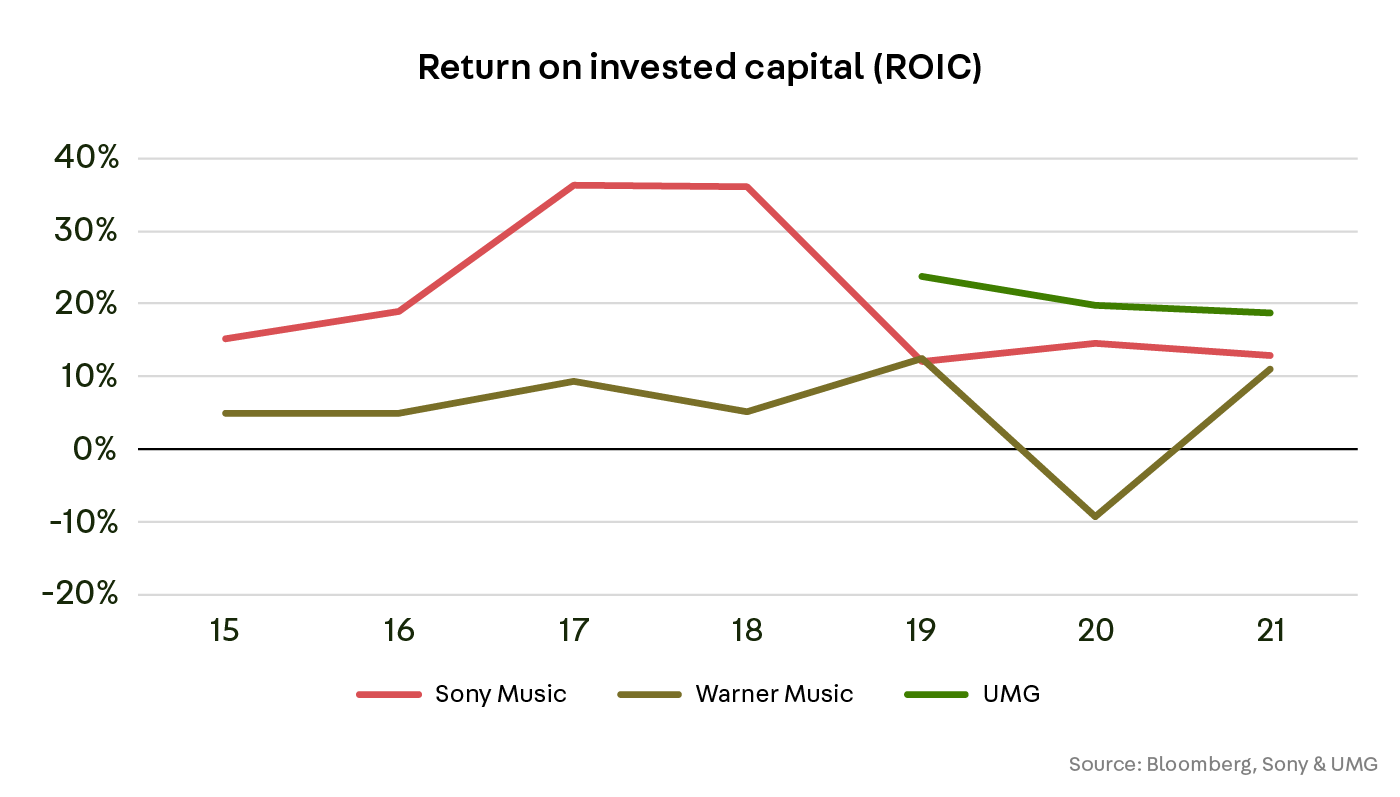

UMG’s track record is healthy also compared to its main competitors, Sony Music, and Warner Music. UMG’s operating margin is in line with the main competitors, but the company’s performance has been more consistent. In addition, UMG’s return on invested capital (ROIC) is clearly above the competition for the last three years.

However, these quantitative factors represent history. How do we know if UMG will perform well also in the future? This brings us to qualitative strengths.

UMG’s content is crucial for streaming services

Music streaming services, such as Spotify, Apple Music, and Amazon Prime rely heavily on record labels for music content. The supply of that content is very concentrated.

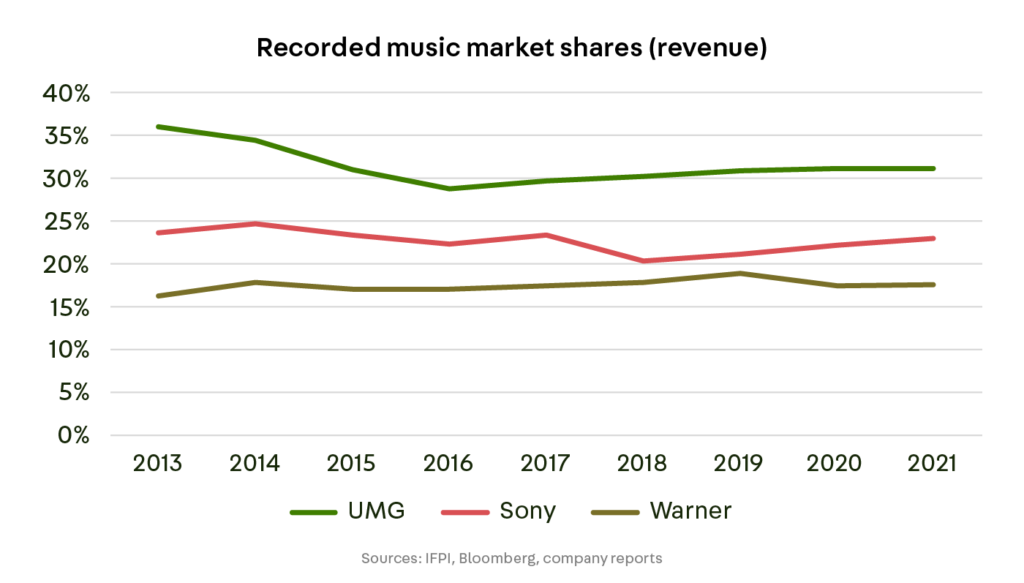

The three major record labels, Sony, Warner and UMG, hold a combined 70% share of the global recorded music market.

Each of these majors owns rights to certain original music recordings, lyrics, or compositions, that the others don’t have. Therefore, none of them can be easily replaced.

UMG is by far the largest major, holding over 30% market share. It would be particularly difficult for a music streaming service to have a competitive offering without UMG. Or would you pay for a streaming service that lacks about a third of your favorite songs?

A large part of UMG’s content will also stay relevant for a long time. As mentioned, the best type of music is listened to over and over again, for years, sometimes for decades.

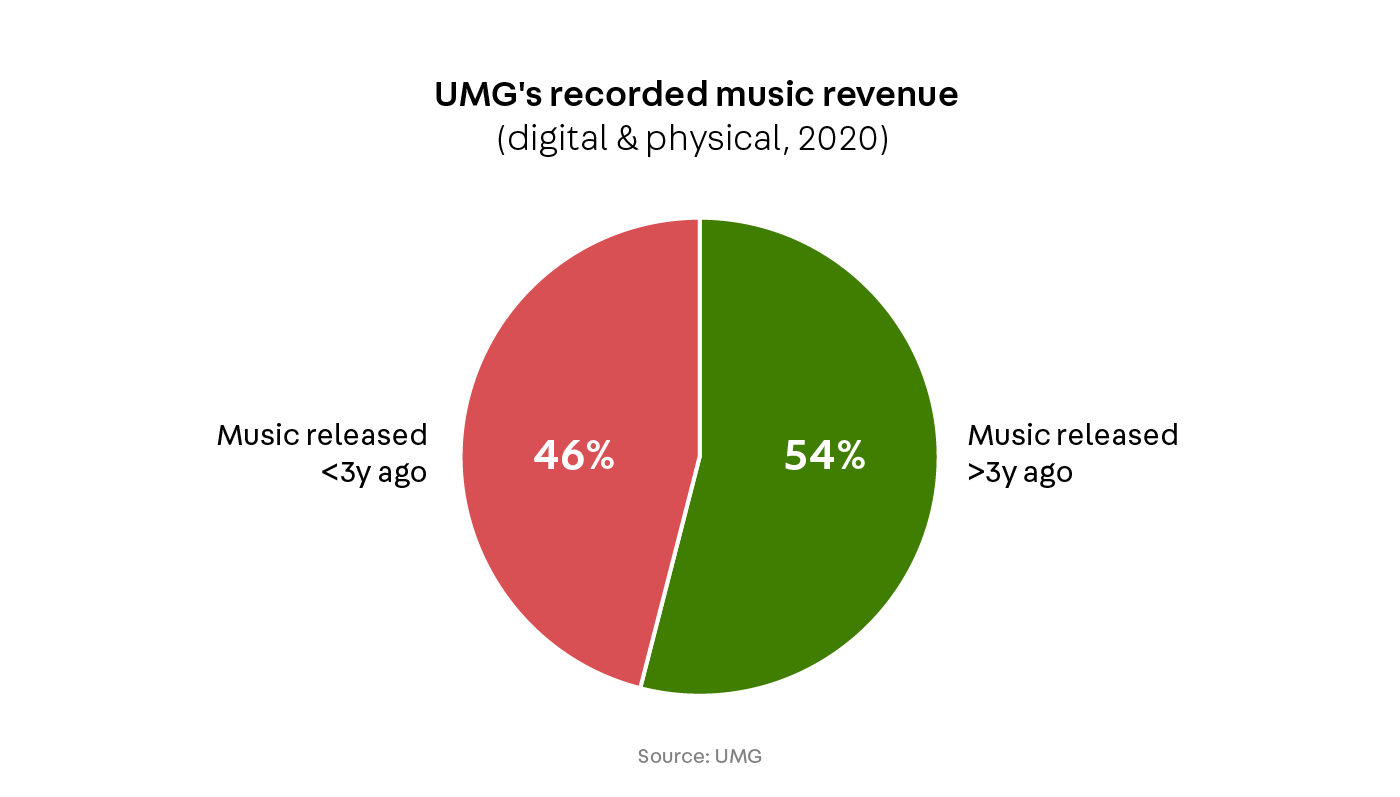

A large share of UMG’s revenue originates from long-lasting content.

For example, in 2020, over half of UMG’s recorded physical and digital music revenue originated from songs that were released over 3 years ago. This suggests that UMG will remain an irreplaceable partner for any music streaming service for a long time.

UMG helps artists stand out

But what about the artists? Why do they choose to sign to UMG, or to a record label to begin with? Firstly, it is not always practical to do everything on your own. Record labels offer the equipment, services, and expertise for every stage of the music-making process, and cover some related activities, such as merchandising.

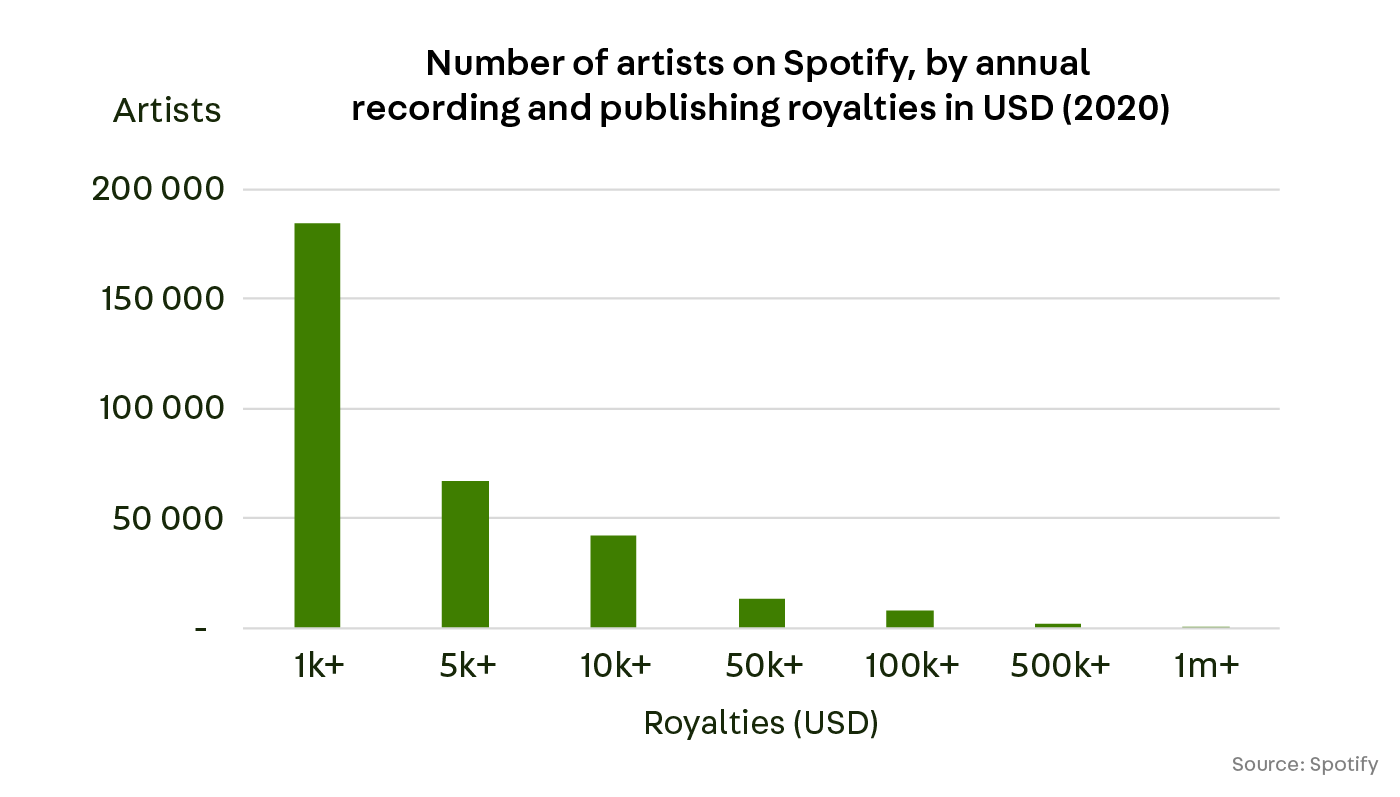

Secondly, record labels have marketing resources and industry contacts that are crucially important to the artists. This is because, on average, it is very unlikely that an artist is discovered by the public.

For example, there were as many as 8 million creators on Spotify in 2020, but only about 13 thousand artists that generated more than 50k USD in annual royalties.

That ratio has become more and more challenging over the past three years, suggesting that standing out requires ever more effort.

In other words, artists have the incentive to look for maximum support, and major record labels can provide that.

The majors have industry-leading risk-taking capacity and networks. In addition, their content is crucial to music streaming services. That crucial role might allow the majors to subtly influence how music is showcased in those services, including the content of editor-created playlists.

Obviously, the more successful an artist becomes, the less dependent that person will be on record labels. Once the contract with UMG expires, the artist may choose to continue without UMG or sign a much more favorable deal for themselves.

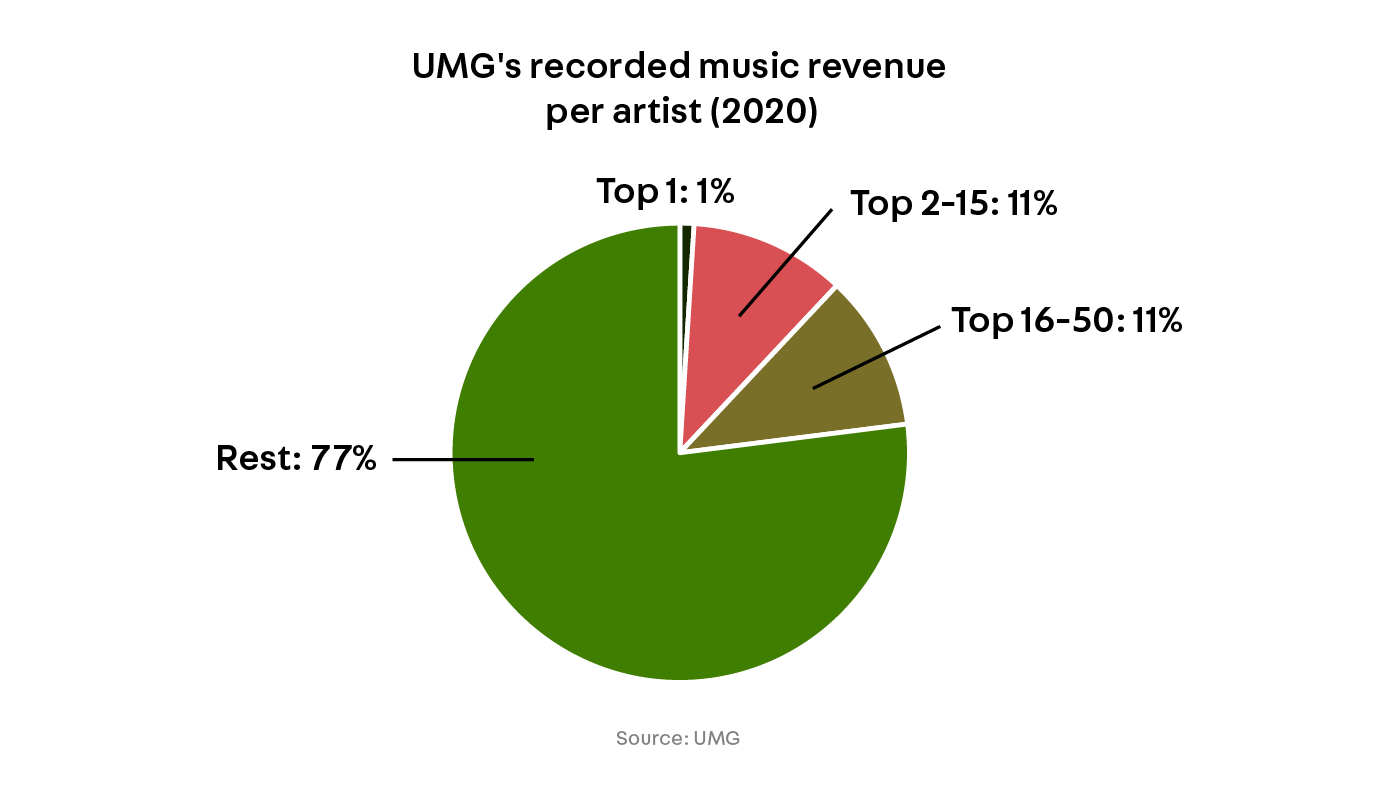

Fortunately for UMG, no single superstar poses a material risk.

In 2020, even the most successful artist generated less than 1% of UMG’s recorded music revenue, while the top 50 generated a bit less than a quarter.

Room for growth in paid music streaming penetration

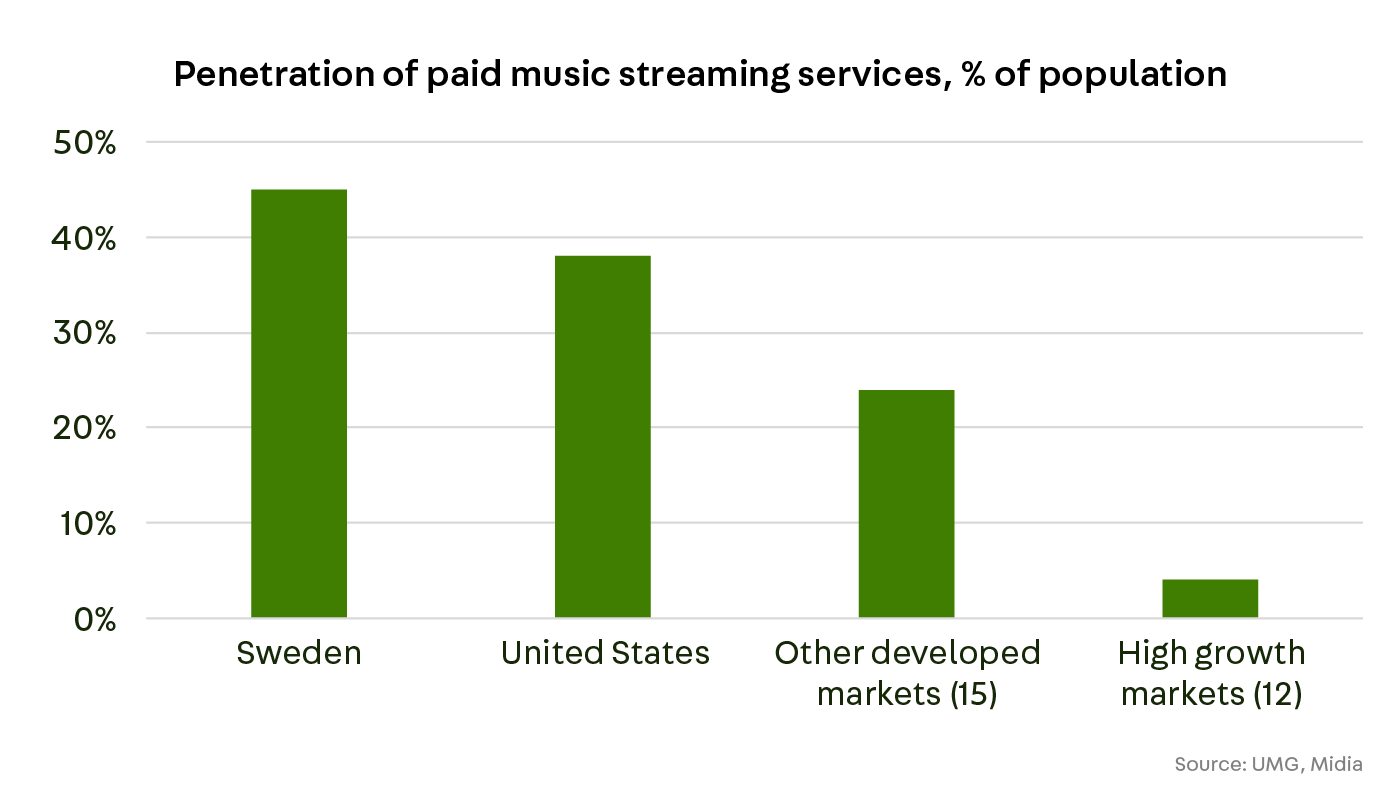

What does UMG’s future look like? In our view, the penetration of paid music streaming services still has plenty of room to grow.

The penetration is 38% in the US, 24% in other developed markets, and just 4% in high-growth markets, according to the research company Midia.

By comparison, the penetration is as high as 45% in Sweden, which is the mature home market of Spotify. This suggests that the global penetration rate still has some meaningful upside potential.

UMG’s own medium-term target is to grow revenue at a high single-digit annual rate from the 2020 level and expand the adjusted EBITDA margin by about 5% points from the 2020 level to the mid-twenties.

Sifter’s current top-line estimates are slightly more cautious than UMG’s targets. We expect UMG’s top line to expand at a ca. 6% annual rate from the 2020 level until 2026, driven by the growing penetration rate of paid streaming services.

Meanwhile, we expect operating margin to expand by a low single-digit amount in 2020-2026, driven by sales mix and scale economies. Over a five-year period, our estimates imply an acceptable valuation relative to Sifter’s portfolio.

Overall, we see that UMG fits Sifter’s quality criteria. UMG operates in a growing market, generates predictable and improving results, has sustainable competitive advantages, and it is available at a reasonable price.

Olli Pöyhönen

Analyst

Sifter Capital Oy