In the short term, share prices react to headlines, sentiment and individual quarterly surprises. Over the long term, a share price tends to follow the development of a company’s earnings power.

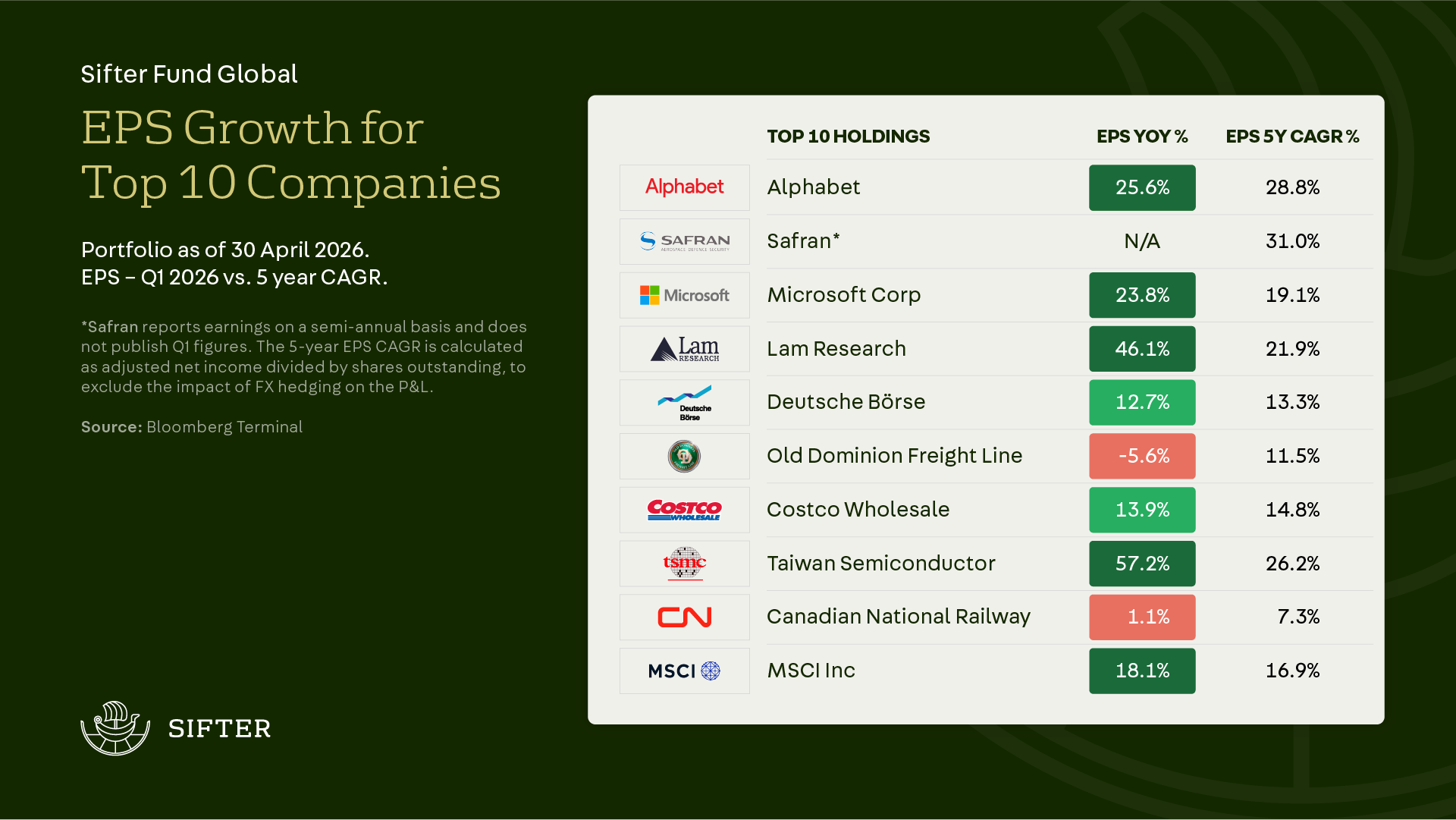

For us, earnings seasons are a way to assess whether our portfolio companies’ earnings growth is progressing as expected. Based on Q1 of 2026, the earnings power of Sifter’s companies was strong.

An estimated 65% of the fund’s capital was in companies that clearly beat expectations. Companies that reported more weakly accounted for around 13% of the portfolio.

The fund’s largest sectors are technology (35%) and industrials (28%), and it was precisely between these two that Q1 revealed a clear difference.

The first-quarter results showed that the earnings slope of technology companies continued to steepen, while for industrial companies earnings growth is only just beginning.

Technology companies benefited from AI at different points in the value chain

AI demand is often spoken of as a single thing. The earnings season showed that it is in reality a multi-layered value chain, where growth arises at different points and at different speeds. Sifter’s technology holdings are spread across the different stages of this value chain.

Alphabet – Cloud services and applications

A common fear has been that AI erodes Google Search. The company’s Q1 result eased those fears. Google Search continued to grow strongly while the cloud business accelerated significantly: the search business grew +19% and the cloud business +63%. At the same time, the cloud business’s order backlog nearly doubled.

This suggests that enterprise customers’ AI and cloud investments are not just experiments, but part of long-lasting infrastructure building.

The most important question for Alphabet’s business is not demand growth, but the return on capital of the investments made.

Microsoft – Cloud services and applications

Microsoft reported strong growth figures: Azure revenue grew +40% and Microsoft Cloud +29%. The market wondered whether AI weakens the pricing power of traditional software companies, and partly for this reason the share price was trending downward during the early part of the year.

From our perspective, Microsoft is not a narrow software company but a cloud, data and ecosystem company.

AI may eat into the margins of some software products, but at the same time it increases the use of Microsoft’s infrastructure. The market’s short-term deliberation does not change the company’s long-term position.

TSMC – Advanced semiconductors

AI applications do not appear out of nowhere. Before a language model responds to a user, chips and memory are needed. TSMC is one of the most critical links in the AI value chain, and its revenue grew +35% in Q1 and net income +58%.

Lam Research – Semiconductor industry equipment makers

Lam Research manufactures equipment used, among other things, in the production of memory chips, which account for the majority of wafer revenue. Lam Research benefited from the investment wave: revenue grew +24% and operating profit +31%.

Company management described the quarter as a record one.

It is important to remember that the semiconductor value chain is cyclical, and an excellent business does not automatically mean an excellent entry point.

This is one of the hardest balancing acts for a long-term investor: quality and valuation must be kept separate. Based on Q1, the earnings power of TSMC and Lam has strengthened, but discipline on valuation must be kept in mind.

Texas Instruments – Semiconductors for industry

Texas Instruments’ end demand comes mainly from industry, automotive, data centers and electronics. This makes the company an early thermometer for industrial demand. In Q1 revenue grew +19% and operating profit +37%, and the company said growth came particularly from industry and data centers.

This is a strong data point in favor of industrial demand awakening more broadly than merely in the shadow of the AI theme, and it leads us naturally to the outlook for Sifter’s industrial companies.

Industrial companies are waking up at different speeds

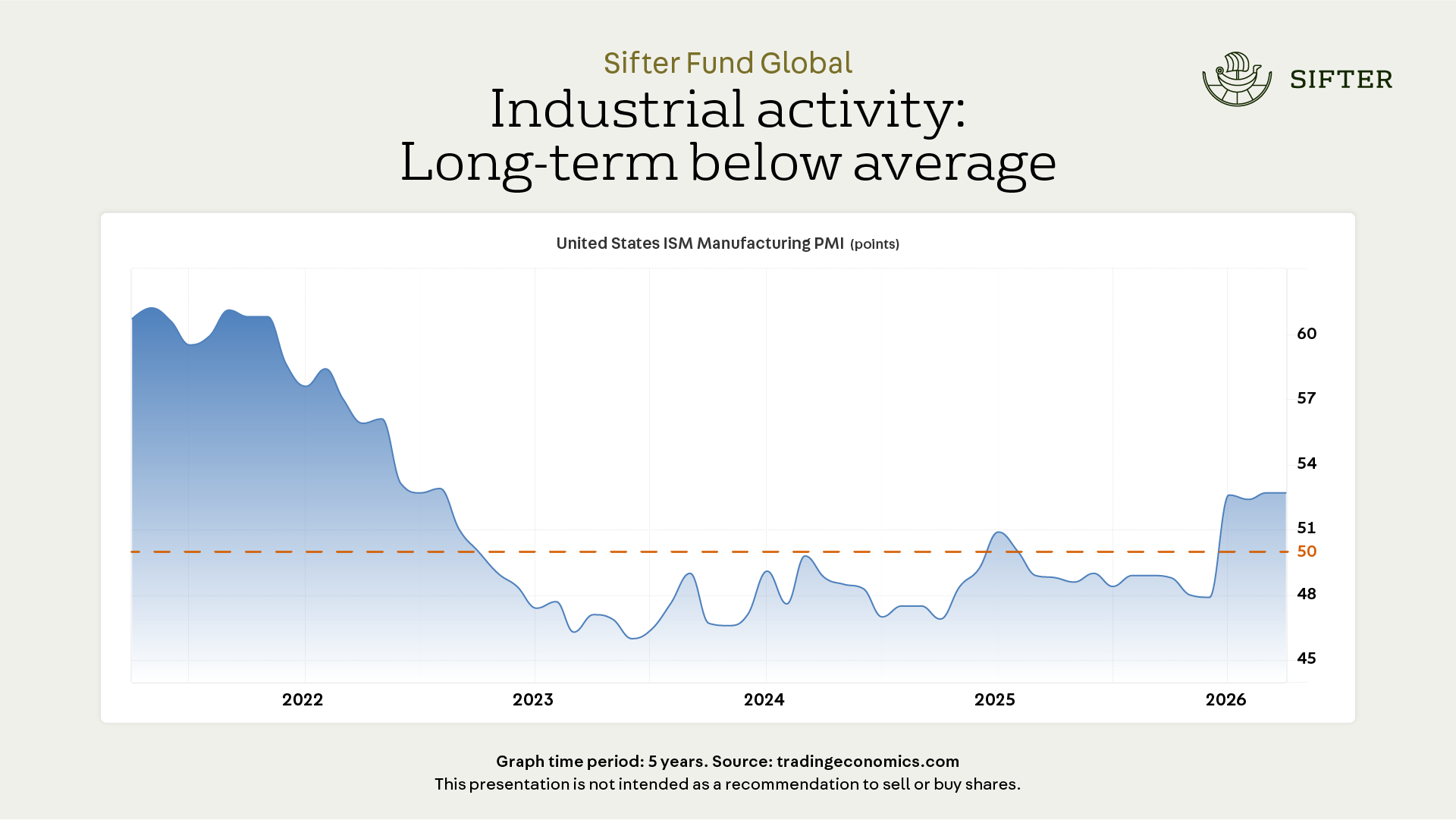

The industrial sector’s multi-year downturn has weighed on the results of Sifter’s industrial companies. Q1 gave first signals of an awakening, but not yet broadly.

The US PMI manufacturing index stood at 52.7 in April, and industry expanded for the fourth consecutive month after a long period of contraction. New orders grew for the fourth and production for the sixth consecutive month.

At the same time, industrial employment weakened and prices rose, so the recovery is not yet painless. This is precisely the environment in which the differences between high-quality industrial companies begin to show. Some capture growth quickly, others are still waiting for volumes to return.

Safran grows at the pace of air traffic, not industry

Safran is classified as an industrial company because it manufactures aircraft engines. However, the company’s growth is not dependent on industrial activity: instead, its growth is driven by the growth of air traffic.

Safran was the clearest success of the earnings season among Sifter’s industrial companies.

Adjusted revenue grew about +19% and organic growth was +23%. Civil engine spare-parts sales grew +29% and services +43%.

Safran’s business does not end with the delivery of an aircraft engine. As the installed engine base grows and flight hours increase, maintenance, spare parts and services bring recurring cash flow for years.

For a long-term investor, this is an interesting combination: a technically demanding industry, a strong aftermarket, high barriers to entry and predictable earnings for years to come.

Canadian National Railway – Industrial activity shows up on the rails

Canadian National Railway delivered record Q1 volumes, and gross ton miles grew +3%. Operationally the network ran well: train speed improved, railcar cycle times shortened and fuel efficiency was, according to the company, a Q1 record.

The bottom line, however, did not yet move at the same pace.

Revenue fell -1% and adjusted EPS -3%. Freight flow is returning, but pricing and transport mix did not yet provide full earnings leverage. This is a typical phase in the cycle: volumes turn first, profitability follows with a lag.

Old Dominion Freight Line – Industrial activity shows up in volumes

Old Dominion Freight Line is a reminder, by contrast, that the everyday reality of freight has not yet properly turned. Revenue fell -2.9% and LTL (Less Than Truckload) tonnage per day -7.7%, even though pricing remained healthy.

Company management saw demand improve as the quarter progressed, but volume pressure is still visible in the results.

Old Dominion is a good example of a company whose quality does not disappear during a weak cycle, but whose real earnings driver returns only when LTL volumes recover.

Sifter’s industrial holdings tell the same story that the ISM and Federal Reserve data point to: industrial activity is returning, but not yet broadly or evenly.

What should we make of this?

A single quarter does not yet draw the earnings slope. But every quarter in which our portfolio companies continue to grow their earnings reinforces the direction we believe will determine returns over the long term.

Based on Q1, the earnings power of Sifter’s companies was strong.

Our technology holdings’ earnings growth continued, for the most part, clearly in double digits, and among our industrial holdings Safran grew strongly for its own reasons, while Canadian National and Old Dominion indicate that the sector’s recovery is still in progress.

The most important question in 2026 is not whether the growth of AI investment continues. It appears that it will. The more relevant question is at what point in the value chain growth turns into durable shareholder value, and how broadly industrial activity spreads from semiconductors, the cloud and data centers to goods flows, freight and traditional industry.

Our task is to stay disciplined. To own companies whose competitive advantages endure, but not to overpay even for a good story.

Q1 confirmed that high-quality companies do their work even in an uncertain market. For us, that is a more important observation than any single share-price reaction.

Santeri Korpinen

CEO