Active funds draw two main criticisms: they often cost too much, and most lag the index over the long term. Much of that criticism is justified.

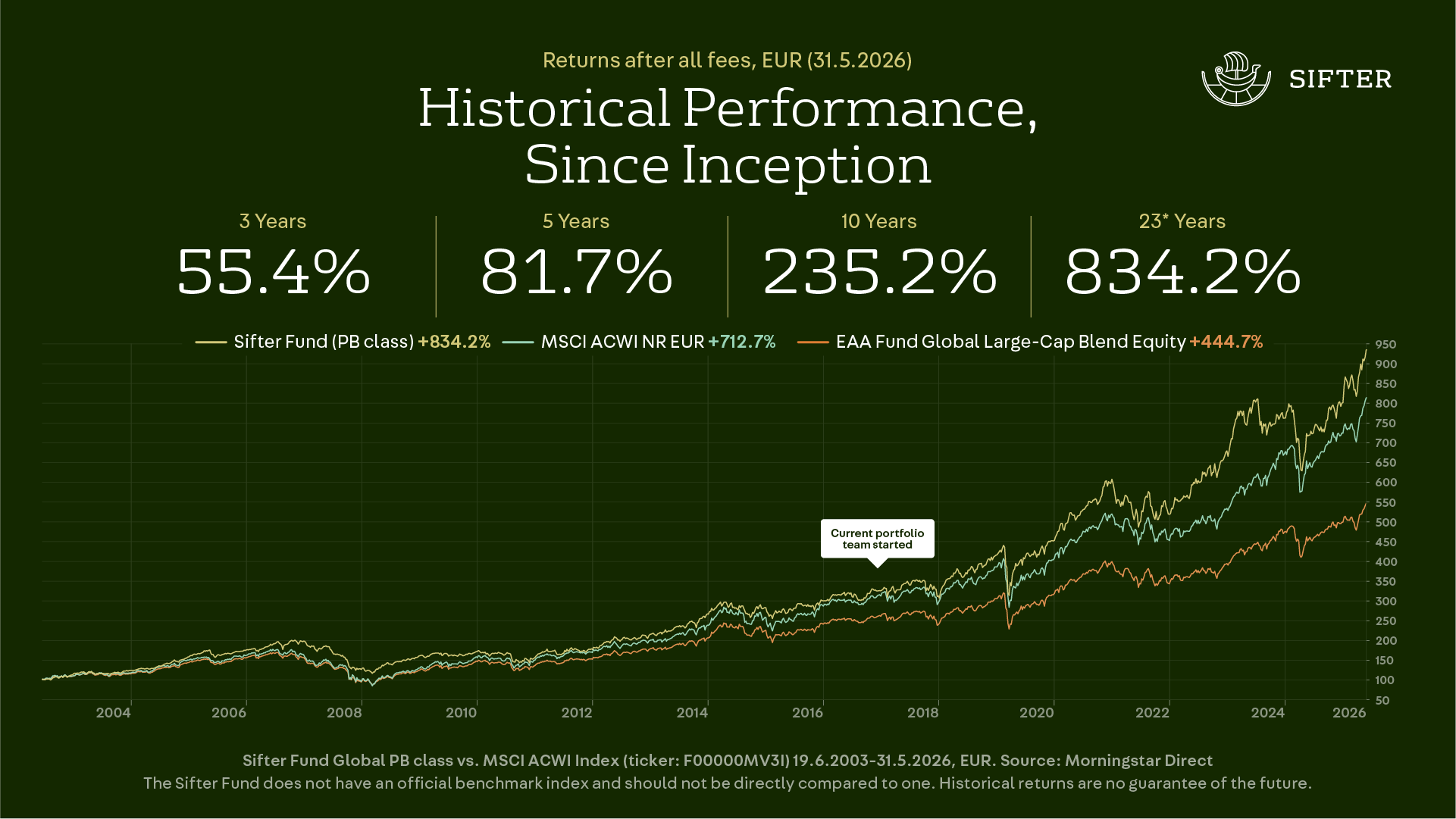

In June, Sifter Fund turns 23, and over that period it has outperformed the global equity index and its peer funds, after all fees.

equity index and a Morningstar category of more than 800 funds, 31 May 2026.

How can a fund lag the index in individual years and still end up well ahead of it over the long term?

The answer is not in timing the market correctly or in forecasting it correctly. Quite the opposite. It comes down to the patience to own the right companies even when they do not, for a time, move in step with the market.

Sifter Fund’s investment strategy is rational in an almost engineering-like way:

We own a small group of carefully chosen, exceptionally high-quality companies that have the ability to grow their earnings over the long term.

Behind this lies a simple observation distilled over decades: over the long term, a share price follows the company’s earnings growth. Over the short term, a share price can swing for almost any reason, but over the years the soundest reason for a rising share price is the company’s earnings growth.

In Sifter’s investment philosophy, we do not try to guess next year’s hottest theme or which sector is in strongest favour right now.

We invest in companies whose earnings have realistic potential to grow over the long term, and we let time do its work.

This requires the chosen companies to have certain characteristics. Let us look at this through an example.

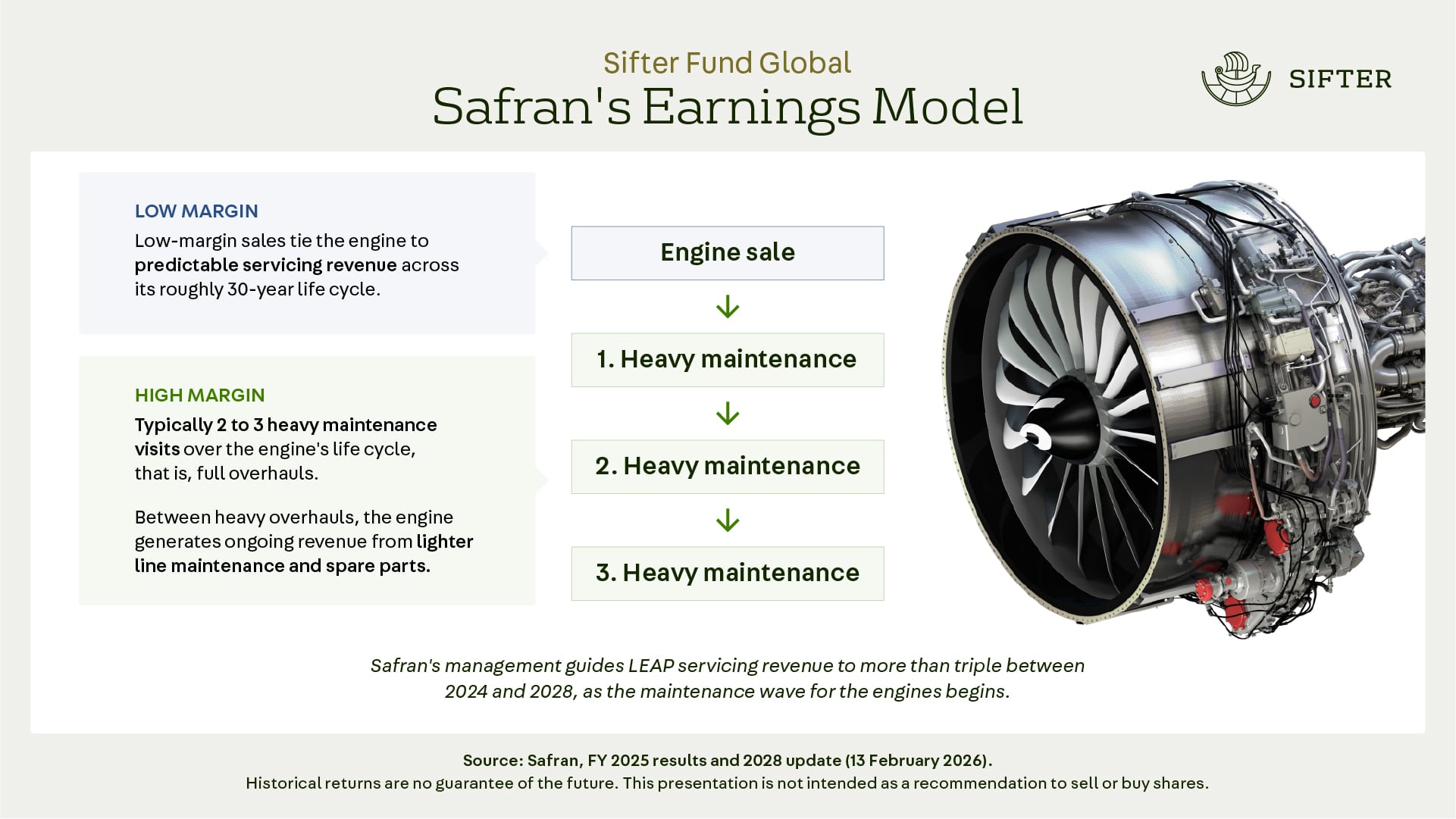

The beauty of Safran’s business model lies in its predictability

The French company Safran makes aircraft engines and has been in our portfolio since 2015. Together with GE, it is the market leader in engines for narrow-body passenger aircraft, with a share of around 70 per cent, and its LEAP engine is a key standard in commercial aviation.

With air travel growing structurally and the aircraft fleet expected to double by 2040, Safran’s earnings growth has an exceptionally long runway.

Safran’s market position is protected by high barriers to entry, patents and industry regulation. In practice, competing against the company is very difficult. Safran is therefore well placed to capture the lion’s share of growth in the end market for air travel.

But how does Safran make money?

There are no large margins in selling Safran’s engines, but the profit is made in servicing.

An aircraft engine has a very long life cycle, and the vast installed base generates servicing revenue that continues for decades after the engine is delivered.

In practice, every time the company builds an aircraft engine, we know that the engine will need spare parts and servicing throughout its life cycle.

The beauty of Safran’s business model lies in its predictability.

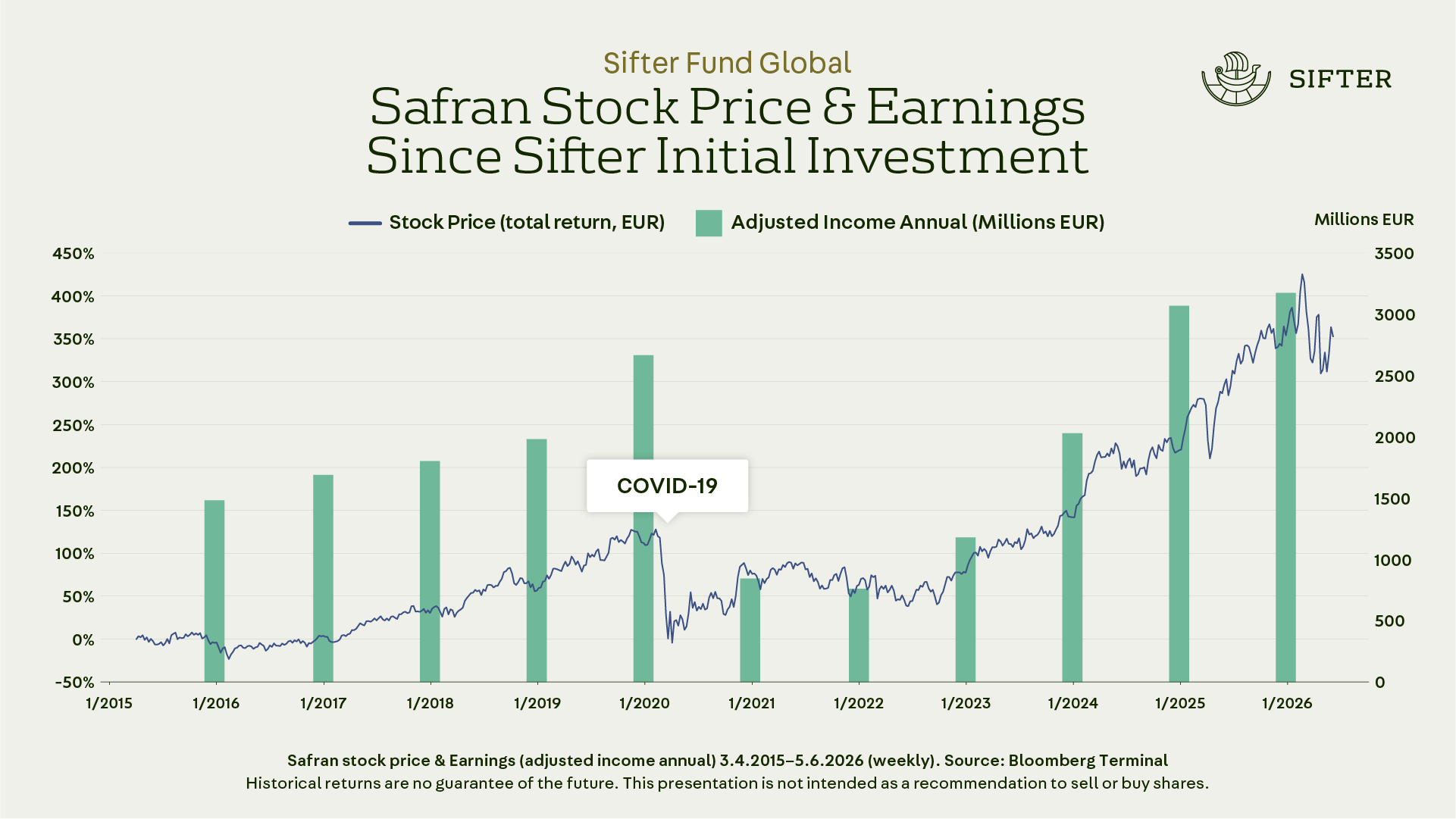

Safran’s share has not, however, risen in a straight line. Its share price took a heavy knock during the COVID pandemic.

During the pandemic, flying stopped as if it had hit a wall, and no one knew when aircraft would take to the air again. Safran’s future looked uncertain.

The most important question for a long-term investor was: would air travel and its growth end with the pandemic? Did the company have what it takes to come through a temporary headwind?

A strong business model and a practically debt-free balance sheet carried the company through the difficult years, and the patient owner was rewarded. Situations like these are exactly when a long-term investor can buy a quality company’s future cash flows at a substantial discount.

Safran is a good example of Sifter Fund’s investment philosophy. When you own a carefully chosen group of very high-quality companies, there is no need to panic over them.

This takes self-discipline, because it is psychologically hard to own shares in a company that are falling for a time while the future looks uncertain.

Even a quality company stumbles now and then, and that is precisely when it matters whether the owner stays put.

Many Sifter Fund investors have described the same experience. When prices fall from time to time, sometimes sharply, they are reassured by knowing what they own: strong companies whose long-term earnings growth rests on rational grounds.

The most valuable skill for a long-term investor is learning to recognise the signs that make a company’s long-term earnings growth possible.

I have written a 20-page guide on the subject. It distils what we have learned over 23 years, including the four pillars that help you identify a quality company. Download the free guide.

What kind of company can grow its earnings year after year over the long term?

Identifying a quality company rests on two things. The historical numbers tell you whether a company has potential:

- Revenue and earnings grow steadily, without large swings

- High return on capital (ROIC), clearly better than competitors

- A healthy, preferably debt-free balance sheet

- High and stable operating margins through the cycle

- Strong free cash flow yield

But numbers only tell you about the past. Only deeper research reveals whether a company’s competitive advantage will hold in the future too:

- High barriers to entry that protect against competition

- Recurring revenue that carries the company through weaker years and provides predictability

- A product or service so critical to the customer that it is not switched lightly

- Pricing power, the ability to pass rising costs on to prices

- Capable management that allocates capital prudently and builds a durable corporate culture

These are only a few examples. If you want to learn more, explore the full framework we use to assess quality companies. Download the free guide: Long-term quality investing.

Santeri Korpinen

CEO

The author is the CEO of Sifter Fund and chair of its investment committee. 80% of his personal equity investments are in Sifter Fund.