The making of processors and memory chips is often associated with near-scifi sounding technology. In contrast, the role of Disco Corporation’s products sounds charmingly modest, primarily involving sawing.

However, the company is surprisingly critical to its customers and may contribute to the extension of chip performance as Moore’s law gradually approaches its limits. The company has also other special characteristics, such as an internal currency system, which encourages entrepreneurship and increases flexibility.

What does Disco do?

Disco is a Japanese company that manufactures and sells equipment which are critical in the manufacturing of chips. Those chips power our everyday electronic devices, such as smartphones and computers. The chips are mainly manufactured on round discs of silicon called “wafers”. The role of Disco’s equipment is to thin, polish and cut such wafers.

In this field, Disco is a giant, with most market estimates implying well over 60% market share in the sale of machines that cut and grind silicon wafers.

Why did we invest in Disco?

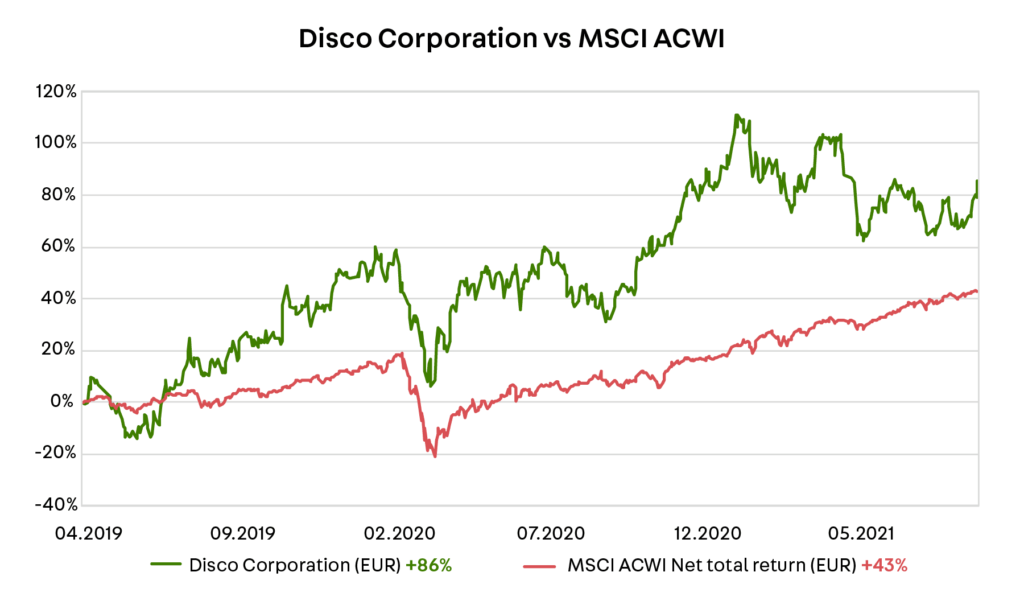

Sifter originally invested in Disco in April 2019. At the time of writing (8.9.2021), the share had appreciated 86% in euros since the initial investment and offered ca. 2% annual dividend yield. Over the same period, the global equity index, MSCI ACWI, generated just 43% return in euros.

At Sifter, we see that Disco fulfills our quantitative and qualitative criteria for a quality company.

Numeric superiority factors

- Turnover grows steadily

- Net profit is increasing and predictable

- Gross and net margins are higher than among competitors

- High return on invested capital (ROIC, over 15 %)

- Healthy balance sheet, preferably a net debt-free company

Qualitative superiority factors

- The earnings model has a clear competitive edge

- High barriers to market entry

- The products and services are critical to customers

- The product represents a minor share of the customer’s total costs

- A large share of the revenue is recurring

- The company’s products have pricing power

- There is growth in the industry

- Skilled management and strong company culture

Interested in long-term quality investing? Download our 20-page guide: Long-term quality investing. Our guide explains how time and high-quality companies work in an investor’s favor.

Disco’s business has significant entry barriers

For Disco’s customers, the cost of failure is high. Disco’s equipment are mainly used at a point where the silicon wafer’s surface is already filled with precious integrated circuits. The wafer may have gone through months of processing – sometimes involving equipment that cost well over 100 million dollars each.

At that stage, inaccurate cutting, grinding, or polishing could spoil the product. Given these risks, Disco’s clients are unlikely to experiment with unproven equipment vendors. Meanwhile, Disco’s equipment are astonishingly accurate.

The machines cut materials with up to a micrometer (1/1000 of a mm) accuracy, which is comparable to cutting a human hair 30 times crosswise.

Disco’s machines can also grind the backside of a wafers down to 5 micrometer thickness, reaching a point where the material is turning translucent. Over the past 10 years, Disco’s has spent on average 10% of its revenue on R&D to maintain its technological edge.

Disco has close customer relationships

Disco’s customer relationships are built on R&D services. In practice, Disco’s engineers perform test cuts and determine the optimal combination of equipment, consumables, and processing methods for the client.

This is no simple task, as Disco’s selection of consumables, such as sawing blades and grinding/polishing wheels, is counted in tens of thousands. The relationships are further strengthened by Disco’s after sales services, such as maintenance and training.

Disco operates in a niche market

According to the semiconductor industry association, SEMI, global investments in semiconductor manufacturing equipment will amount to 95 billion USD in 2021. When we compare SEMI’s estimates to Disco’s modest USD 2 billion revenue and high market share, it seems clear that Disco operates in a niche.

Disco’s small market size offers two advantages: First, it limits incentives for large players to enter Disco’s territory, as the rewards would be relatively modest. Second, Disco’s critical role and small-scale business reduce price pressure from clients’ side, as the most effective cost savings are probably found somewhere else.

Disco’s margins and returns reflect a healthy competitive position

In the latest fiscal year, Disco’s gross margin amounted to 59% while the EBITDA margin was 33%. The average return on invested capital over the past 5 years amounts to 15%. Disco’s closest competitor, Tokyo Seimitsu, generates about 1/3 lower margins and returns.

Long-term outlook – Promising

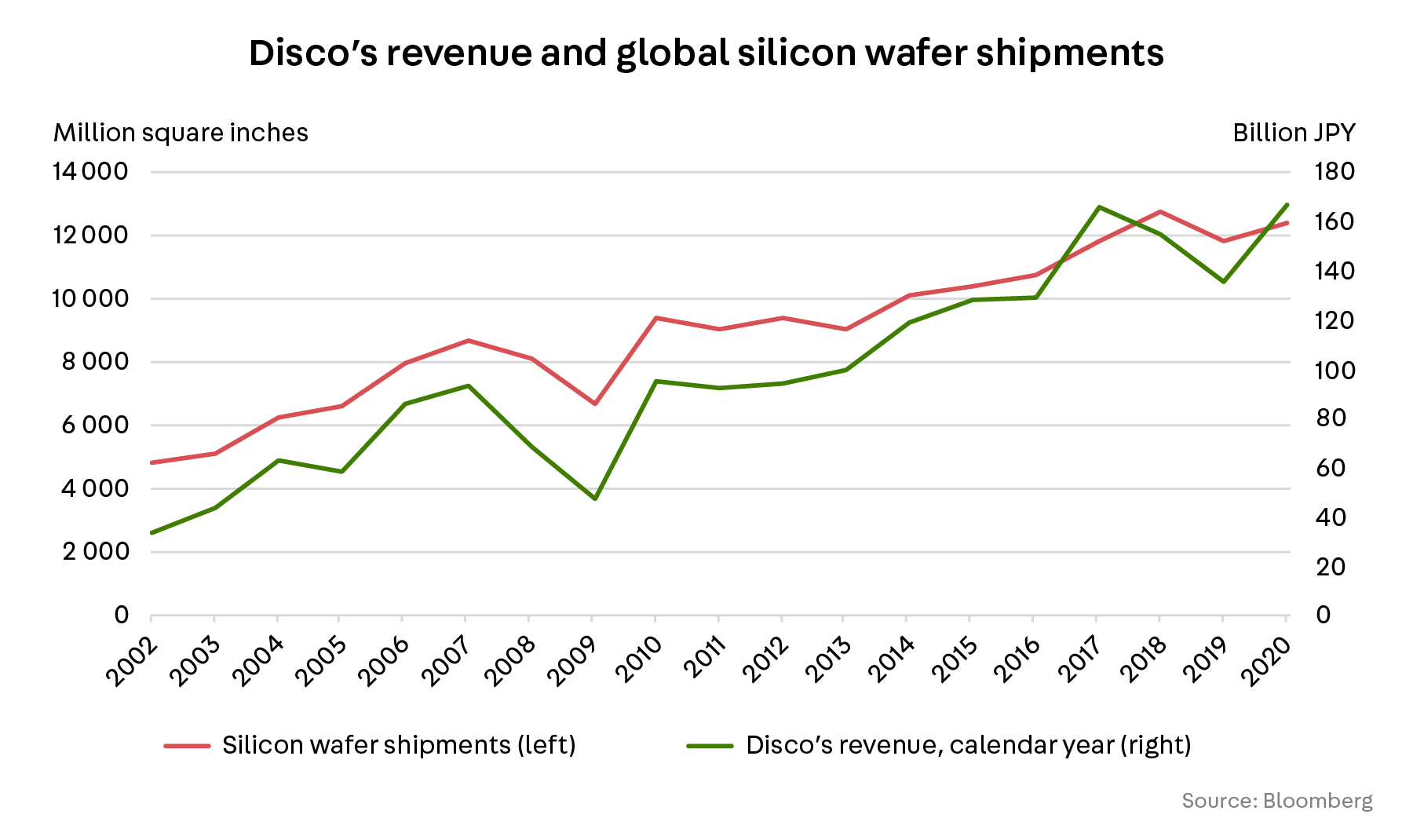

Global wafer volumes seem likely to increase further, as the number of smart devices increases.

Historically, Disco’s annual (calendar year) revenue has correlated strongly with the global wafer shipment volumes. In 2010-2020, the correlation coefficient was 0.95. Going forward, the wafer volumes seem to have further upside.

For example, 5G networks will better support a network of connected devices (also known as Internet of Things), by facilitating a larger number of devices, while offering lower latency and faster data speeds. This is good news for Disco, as a larger number of smart devices should result in a larger number of wafers to grind, saw and polish.

The physical limits to transistor size could offer further upside for Disco

Historically, chip performance has been increased by cramming a larger number of ever smaller transistors into the same chip. The number of transistors has increased at a predictable pace, reflecting the so-called Moore’s law. However, the process has become increasingly costly and should eventually slow down, restricted by the laws of physics. As a result, chip manufacturers will have to increasingly turn to other methods to achieve performance improvements.

One such method is 3D packaging, where several chips are stacked on top of each other. Disco is optimistic regarding this trend and sees that it could drive higher margins and revenue. We see that 3D packaging could increase the demand for thin chips and boost the use of Disco’s equipment.

Short-term outlook – Disco’s main source of revenue is volatile, but balanced by several strengths

Some 52% of Disco’s revenue originates from the sale of precision equipment which are essentially a capital expenditure for Disco’s clients. The semiconductor industry’s capex has been volatile through the years, and this has reflected on Disco’s equipment sales.

Currently, the short-term outlook is positive. The semiconductor industry association, SEMI, forecasted in July that the global sales of semiconductor manufacturing equipment will soar by 34% in 2021 and grow by 6% in 2022.

Disco’s Japan-centric operations expose the company to fluctuations in exchange rates and tariffs.

Some 80% of Disco’s workforce and 100% of manufacturing operations are located on the Japanese soil, while 86% of the revenue originates outside Japan, primarily in Asia. As a result, appreciating yen and higher tariffs would add to Disco’s costs and put pressure on Disco’s profitability.

Disco’s financial resilience helps it to manage short-term shocks

Disco’s financial resilience is built on three factors:

- First, Disco holds no debt on its balance sheet. Instead, the company has cash worth some 1.5x times its past 12-month EBITDA. This financial buffer helps Disco to weather through storms.

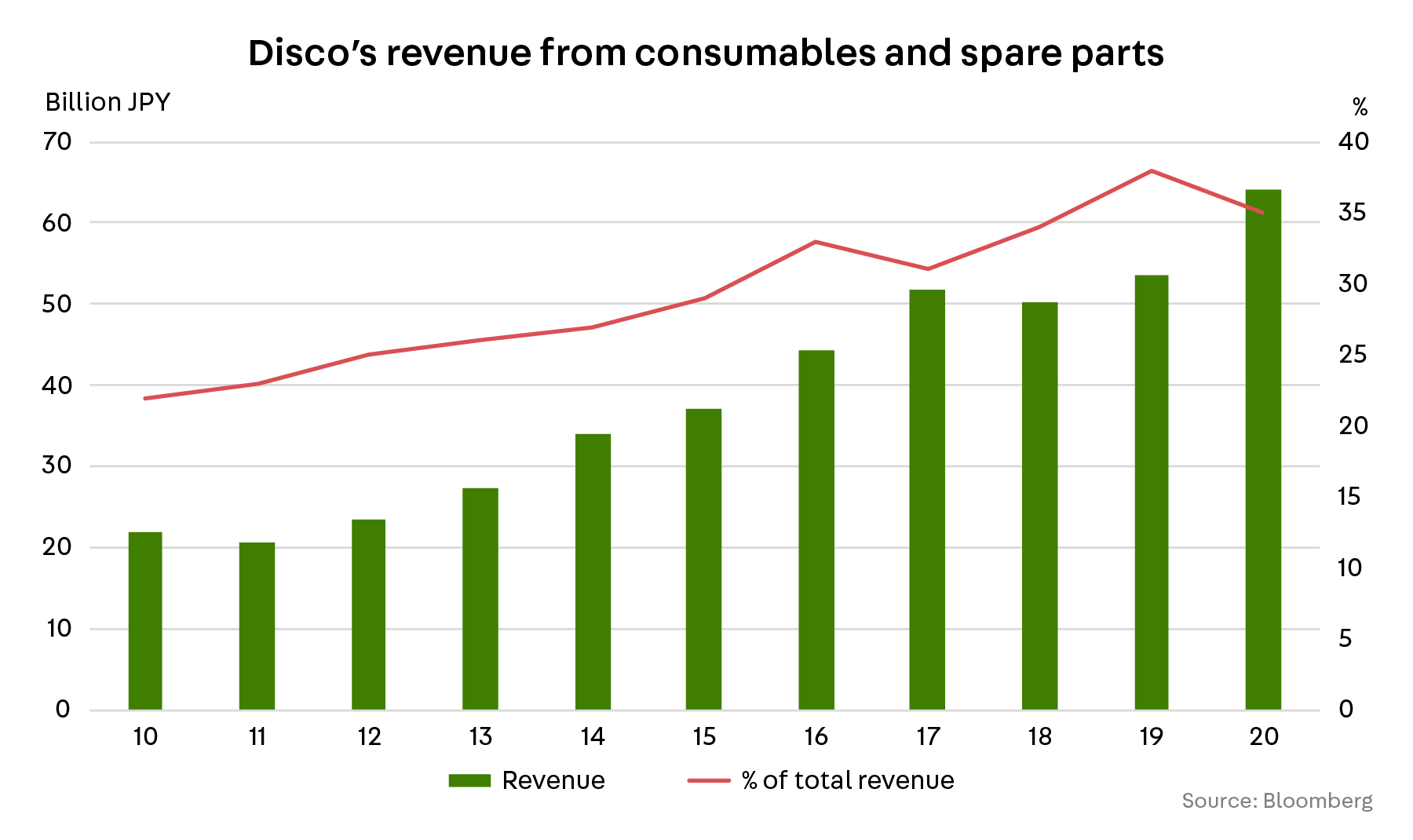

- Second, Disco generates one third of its revenue from consumables and spare parts, where margins are high. The demand for these products is driven by clients’ capacity utilization rate which is less volatile than capital expenditures. Disco’s consumable and spare part sales have gradually grown through the years, likely supported by growth in Disco’s installed base (See Chart 4).

- Third, Disco’s strong market position supports the company’s pricing power. This in turn helps Disco to offset cost increases with higher prices.

Exceptional corporate culture may add to Disco’s resilience

Disco’s culture incorporates strong entrepreneurial spirit and continuous improvement. To boost this culture, Disco has created its own internal currency, called “Will”. Since 2011, Disco’s employees and teams have used “Will” to pay for the use of company resources, such as office desks and PCs.

In the bigger picture, sales transactions generate “Will” which trickles through the organization, as different teams compensate each other. For example, a sales team might compensate the manufacturing team for building a product for the client. At the end of each quarter, the balances of “Will” are paid in yen – resulting in hefty bonuses for some.

At first sight, “Will” seems to merely complement Disco’s rewarding systems and discourage the waste of company resources. However, “Will” can also be used to rapidly solve unexpected management issues. For example, during the COVID-19 pandemic, Disco had to ensure that its factories had enough employees working on-site. Instead of hand-picking the on-site employees, Disco distributed a set amount of “Will” among those employees who chose to turn up at the factory.

As a result, Disco’s internal market forces chose the optimal on-site employees, and adjusted the per-person reward automatically, reflecting the evolving popularity of remote work.

Overall – Disco meets Sifter’s quality criteria

Disco holds significant competitive advantages which are reflected in the company’s historical performance. In addition, Disco’s market has a positive long-term growth outlook, and the company is able to weather short-term storms along the way.

Olli Pöyhönen

Analyst, Sifter Capital