The stock market is falling, but corporate earnings expectations are still strong. This is a paradox that merits further investigation. Has the market again overreacted to the noise of the macro world, or are the profit forecasts too rosy? In the short term, probably both.

We looked at the matter through the investment criteria of the Sifter fund, which we use to search for reasonably valued quality companies worldwide with upside potential.

One important measure is to screen companies whose earnings can be maintained, even in a recession. We believe that the upside potential of such companies in the market turnaround is unparalleled, and thus the current down market creates buying opportunities.

What factors affect company results?

We think it is pretty clear that companies will perform differently in the current economic environment, and their results will vary greatly. Firstly, it is necessary to analyze how the company’s demand changes, i.e., the increase or decrease in sales.

Demand is influenced by the criticality of the company’s products and services to customers.

Secondly, company results can be burdened by a surprising increase in expenses, which significantly weighs on the manufacturing companies in the form of rising raw material prices.

Also, heavily indebted companies find themselves in a new situation where the increase in financing costs weakens their results. The examples given are from the portfolio of the Sifter fund.

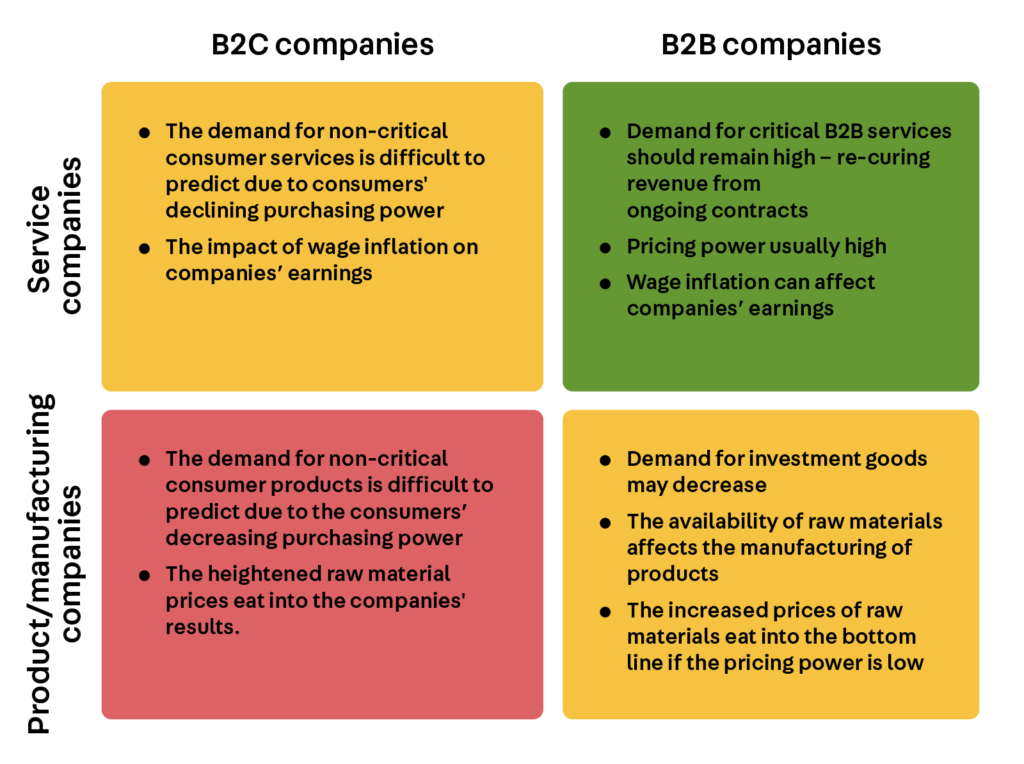

What does the company sell, to which customer group and how critical is the service?

The picture below is a simplified model for evaluating the company earnings models, i.e., what does the company sell, to which customer group, and how critical is the service?

We estimate that B2B companies offering purely critical services (upper-hand corner) are perhaps the best recession-proof companies to maintain the demand and earnings in the current market. These quality companies have strong pricing power, continuous service contracts, and the ability to successfully pass on any increased costs in their products or services to the customer.

Critical service companies have an advantage

The customer lock-in for critical services is entirely different from, for example, consumer goods companies, which have to compete for the consumer’s shrinking paycheck and everyday choices.

Examples of companies that offer critical services are the US company Automatic Data Processing, which provides payroll software, Verisign, which offers .com and .net domains, and Microsoft, which includes cloud services and licenses for businesses and consumers.

Similarly, products or services that have been purchased during a high economic cycle may suffer in a recession. For example, the most significant investments in the home, such as buying a car, renovating the home, or the demand for vacation trips, may decrease because consumers only have money to spend on the essentials.

Pricing power keeps margins high

One of the characteristics of a quality company is pricing power. As the purchasing power of consumers decreases, ruthless competition for the affordability of products and services begins. Price wars lead many companies to unload their inventories and lower their prices to maintain demand at the expense of lower margins.

Companies with critical products and services are better able to defend their prices because there is often less competition and steady demand.

For example, pharmaceutical companies can often maintain both demand and margins quite well, including during a recession. The Sifter portfolio has a long-term investment in the Danish company Novo Nordisk, the global market leader in diabetes medicines.

Novo’s sales margins have long been over 80 percent. Even if the company’s expenses rise due to inflation, the high margins guarantee company maintains high earnings. For example, a critical drug provider has pricing power, and the ability to increase prices with little or no impact on sales.

Product businesses suffer from increased raw material costs

We estimate that companies that manufacture products will suffer more from the increased prices of raw materials and supply shortages than pure service companies.

In particular, the availability of raw materials has already weakened the results of many high-quality product companies because they have not been able to manufacture their products in sufficient quantities.

The low availability of critical components has, for example, weakened the sales of Sony, which manufactures the Playstation 5 game console. Another example of this is Autoliv, which manufactures car safety equipment, and has suffered from rising raw-material costs and supply chain bottlenecks.

When car manufacturers can’t finish cars because of missing chips, car safety devices don’t sell either. The consequences of supply chain disruption may be far-reaching and their analysis is complicated. Service companies do not have this problem on the same scale.

Debt-free companies become stronger

With the rise in interest rates, companies with a heavy debt load must pay a high price for money borrowed, which eats into their profits.

According to some estimates, up to 20 percent of US stock-listed companies are so-called zombie companies, which have only remained afloat after the pandemic thanks to cheap loans. Even if the company is not a zombie company, the management of the indebted company has to focus its time, energy, and resources on restructuring the loans and keeping the cash flow positive.

During a recession, the management of debt-free companies can accordingly concentrate on developing their company’s business and, if necessary, buy market share, i.e., away from their indebted competitors.

The strong get stronger when times are tough.

Rising interest rates increase the results of some companies

Sifter’s portfolio includes Automatic Data Processing or ADP, which offers payroll management software for companies. Every fifth private employee’s salary in the United States goes through ADP software. At the same time, ADP receives billions of dollars, which it can invest in the bond market.

According to our analysis when interest rates rise by one percent, ADP’s operating profit increases by an additional 8 percent.

However, this was not the original reason we invested in the company, but it has turned out to be quite a positive thing in a market of rising interest rates.

Sifter Fund companies are in high quality

The reliability of the business results of quality companies is high. That is why, during the fund’s 20-year history, we have wanted to invest in stable quality companies, regardless of the economic situation. At the time of writing (end of September 2022), the holdings in the Sifter portfolio are:

- 50% of the companies are pure service companies

- 80% engage in B2B business

- A large majority of companies provide critical B2B services which are expected to maintain their sales, pricing power, and earnings.

- The Portfolio companies’ sales margins are, on average, 50 percent

- The portfolio companies’ average operating profit is 27 percent

- The portfolio companies in the portfolio are, on average, debt-free (0.1x EBITDA)

What are the opportunities for a long-term investor in a down market?

During the drop, doubts about the weakening of the economy have lowered share prices. Even very high-quality shares have fallen, often excessively.

At moments like these, the long-term equity investor looks away from stock prices and the next quarter’s results and focuses on evaluating company earnings models, pricing power, and competitive advantages over the next five years.

When the investor comes across high-quality companies whose business the long-term investor believes in and whose future cash flows can be bought cheaply, the investor reaps the harvest and waits for the market to rise. This is also, in essence, how the Sifter fund works.

Santeri Korpinen

CEO, Sifter Capital