When comparing investment options, an investor’s attention often drifts to returns and fees – concrete figures that indicate how much one has to pay for investing and what the investment has historically yielded.

A more experienced investor possesses the expertise to evaluate the risks associated with returns. They aim to strike a balance between risk and return, prioritizing risk-adjusted returns.

Three Key Measures of Risk-Adjusted Return

Understanding risk-adjusted return requires some effort, but in return, you get a better idea, for example, of the quality of portfolio management in an equity fund.

Risk-adjusted return can be examined using three typical measures: the fund’s volatility, Sharpe ratio, and Alpha.

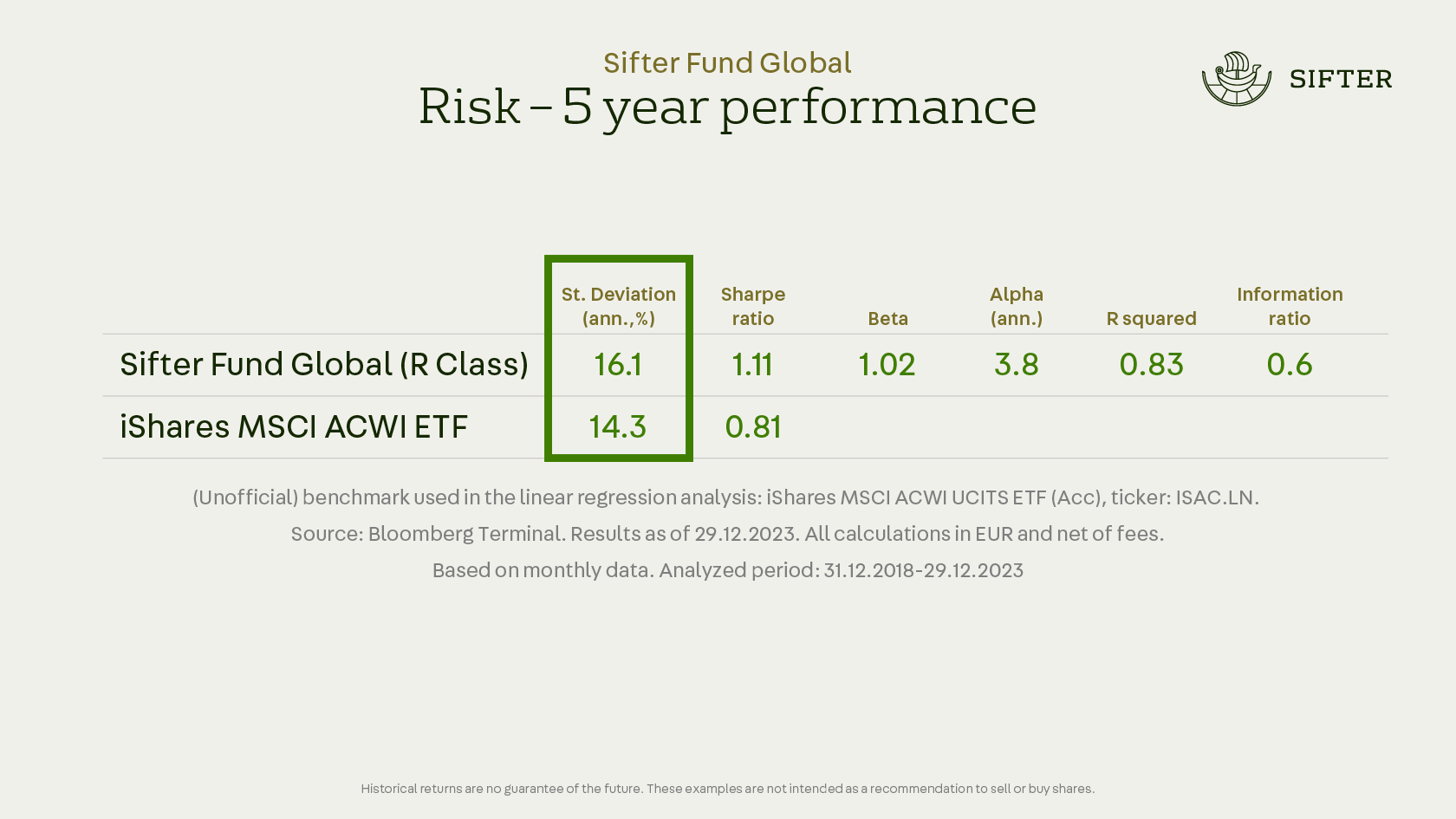

Volatility Indicates Price Fluctuations

Volatility tells us how much a stock or fund price has changed over a certain period.

Higher volatility may indicate a greater risk, but also the possibility of a higher return.

When we examine the volatility of the Sifter Fund and compare it to a global index fund (iShares MSCI ACWI ETF), we see that the Sifter Fund’s volatility is slightly higher than that of the global index fund.

The primary cause of the marginally higher volatility, compared to the ETF, is that a concentrated group of companies with larger weightings exhibits greater sensitivity to fluctuations in individual stock prices than an index fund, where the holdings of individual companies are considerably smaller. On the other hand, achieving excess returns would not be possible without a larger weighting in carefully selected companies.

The Sifter Fund has about 30 companies, and the iShares MSCI ACWI ETF has over 2,300 companies.

In the Sifter Fund’s investment strategy, we do not regard volatility as a significant measure of risk, as it merely reflects stock price fluctuations and reveals little about the company’s underlying business.

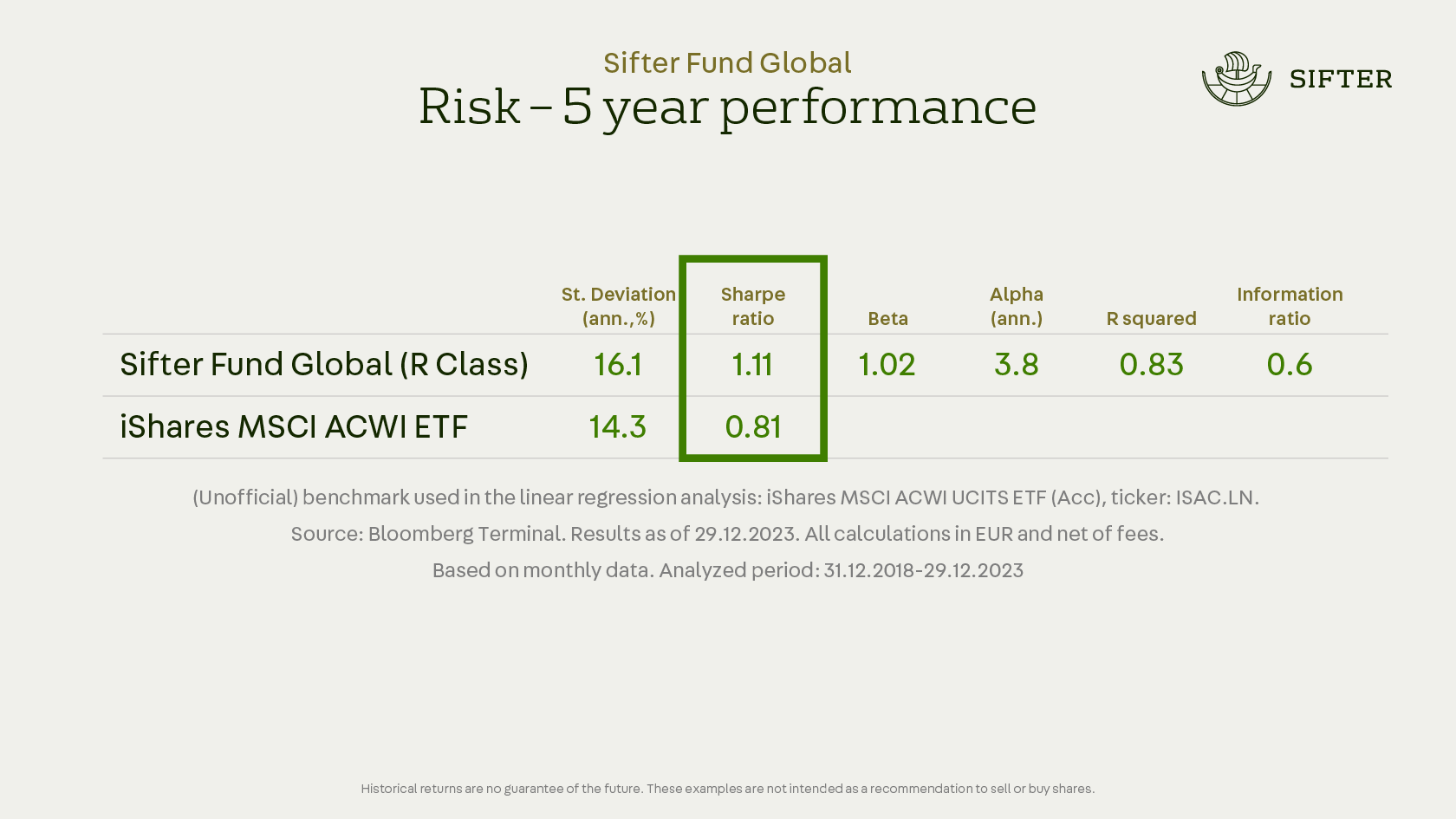

The Sharpe Ratio is a Measure of Excess Return Balance

The Sharpe ratio measures the excess return of an investment in relation to its volatility, thus offering a view of the balance between the investment’s return and the risk taken.

The Sharpe ratio is calculated by subtracting the risk-free return (for example, the return on government bonds) from the total return of the investment and dividing this difference by the investment’s average volatility over the same period.

The Sharpe ratio measures how much extra return the investor gets for each unit of risk to which the fund is exposed.

A high Sharpe ratio indicates that the investor is receiving a relatively high return considering the level of risk taken, while a low ratio indicates a relatively low return for the risk level.

The advantage of the Sharpe ratio is its comparability; it facilitates the comparison of risk-adjusted returns across different investment options. While the Sharpe ratio for individual years may not provide much relevance for a long-term fund, a five-year period offers a solid indication of whether the risks taken have been advantageous to investors.

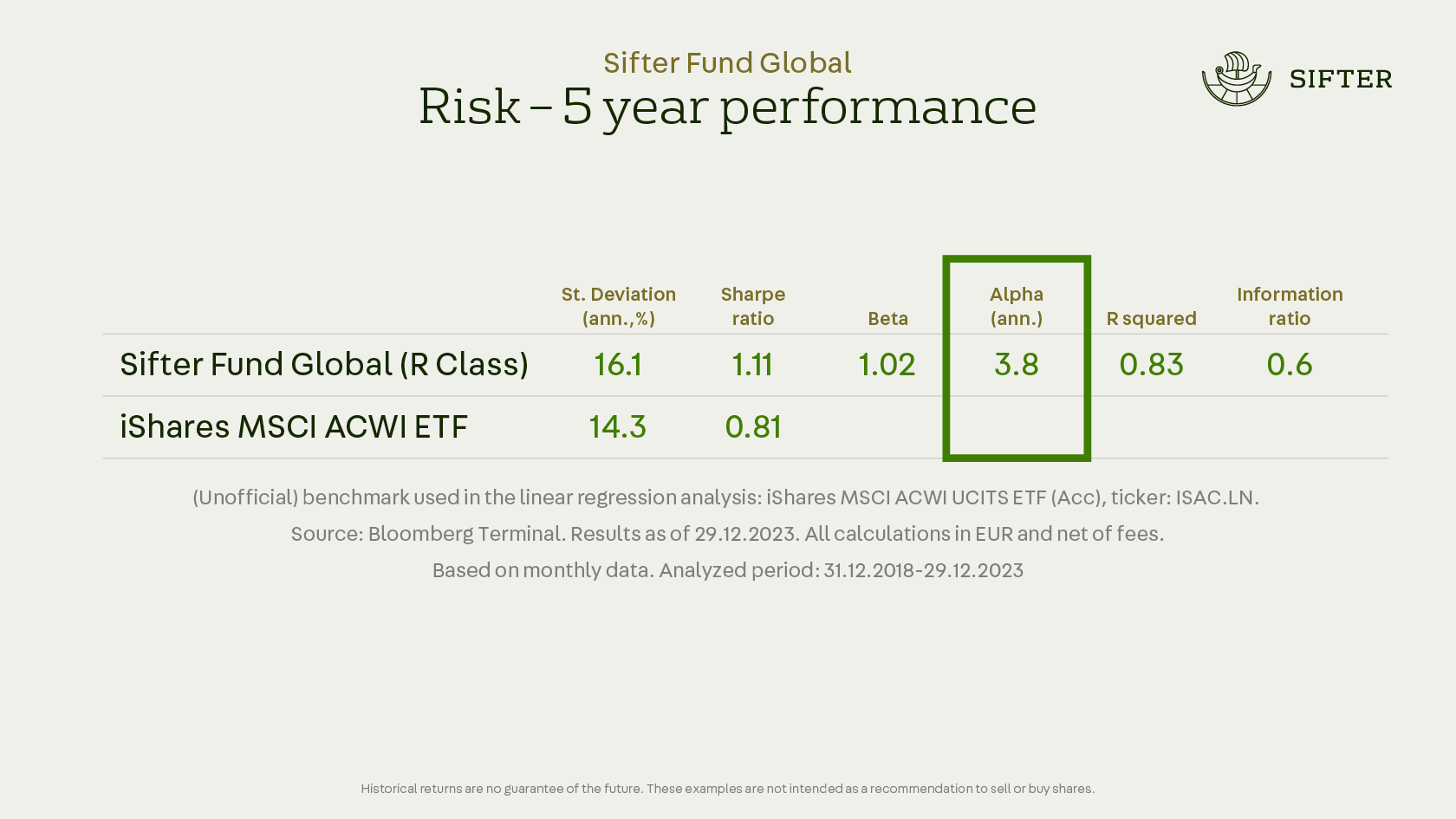

Alpha Distinguishes Good from Bad Portfolio Managers

Alpha provides an insight into how much value the portfolio manager has been able to create relative to the risk taken.

Alpha measures the return that exceeds or falls short of comparison index returns, considering the investment’s risk level.

A positive Alpha indicates that the portfolio manager has succeeded in providing excess return at the given risk level.

As a practical example, we can compare the Sifter Fund to a popular low-cost index fund (iShares MSCI ACWI ETF). The Sifter Fund does not have an official comparison index, but this ETF is well-known and reflects the global stock market’s performance well.

The Alpha of the Sifter Fund demonstrates that over a five-year period, Sifter has generated an average annual excess return of 3.8%, compared to the global index fund, iShares MSCI ACWI ETF.

Sifter’s beta (1.02) suggests that Sifter’s value has not been particularly sensitive or insensitive to changes in the comparison index’s value. Sifter’s beta is just slightly over one, which means, in practice, that Sifter’s value has on average moved about one to one with the index when the portfolio manager’s influence is not considered.

Can an investor achieve high returns without the risk level rising in proportion?

Over the past five years, the Sifter Fund has secured notably high excess returns relative to the benchmark index fund, without incurring significant additional risk.

The extra risk assumed by the Sifter Fund, in comparison to the index fund, is minimal, yet it has yielded favorable returns for that additional risk. While the Sifter Fund presents an appealing option in terms of risk-adjusted return, it’s crucial to acknowledge the uncertainty surrounding future stock market directions.

Historical return or risk is not a guarantee of future performance.

How Has Sifter Prepared for Risks?

Stock price fluctuations are influenced by the global economic landscape, market momentum, and the business performance and outlook of companies. Through experience, we’ve learned that our control extends only to selecting the types of companies we wish to own.

We assure our investors that we hold stakes in exceptionally high-quality companies and actively oversee their business progress.

We make proactive decisions when we identify threats to the competitive edge and profitability of a company within our portfolio, or when we discover another company that, in our opinion, offers a superior return potential.

While we’re not immune to fluctuations in global markets and stock prices, we firmly believe in the long-term growth of global economies and the innovation that introduces new services and significant efficiency improvements.

Thus, we are confident that investing in high-quality companies will afford us adequate risk protection in the stock market.

Santeri Korpinen

CEO