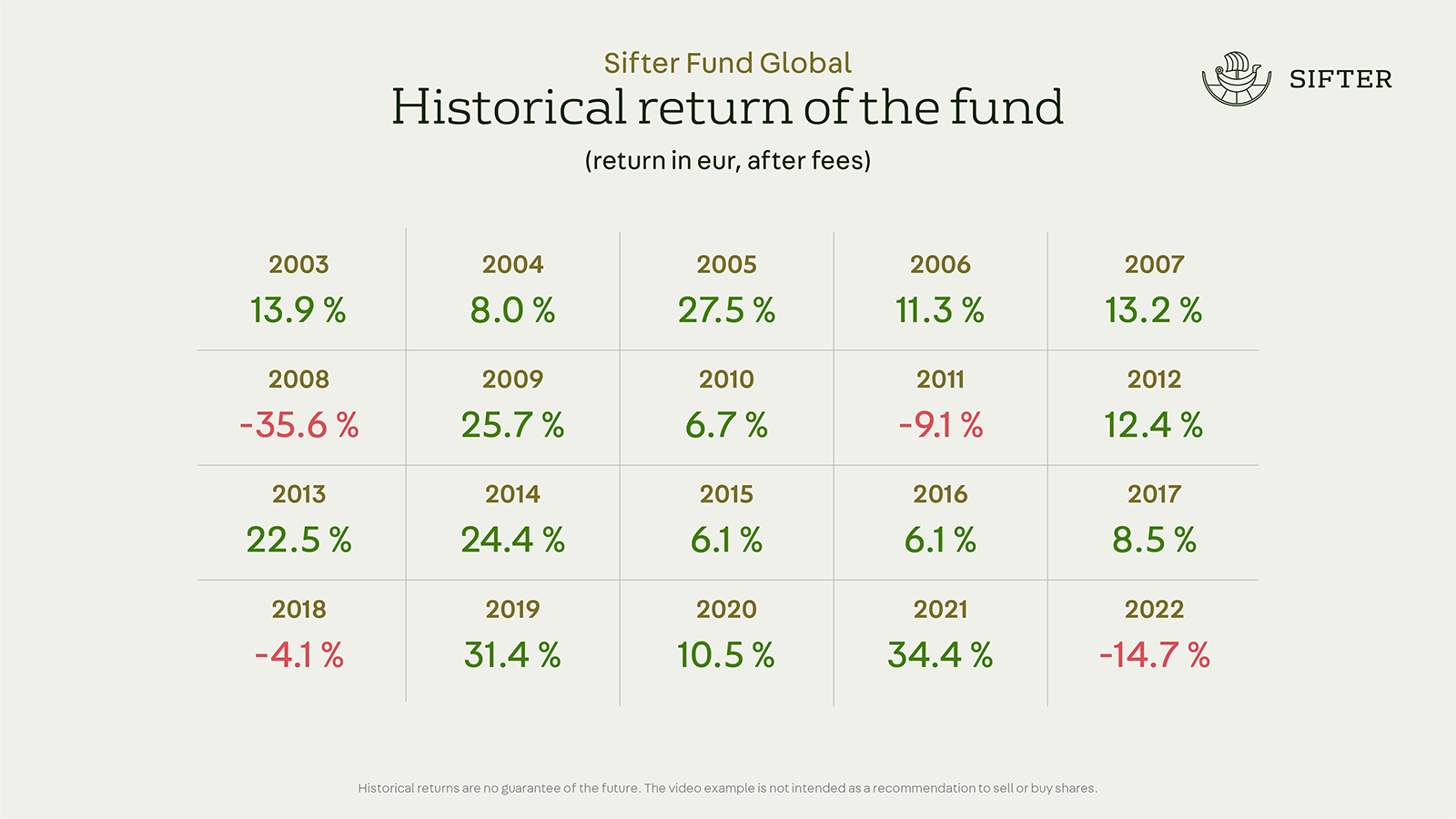

2022 was the fourth negative year in the 20-year history of the Sifter fund (-14.7%). For sixteen of those 20 years, the fund has generated a positive return. Since the beginning of its history, the fund has produced an average annual return of 9.0 percent for its investors (September 16, 2003–December 31, 2022).

2022 was a challenging year for equity investors. The war in Ukraine reminded investors of the importance of geographical diversification. However, the war has had surprisingly little effect on share prices globally. Still, it has caused difficulties in company supply chains and accelerated inflation in Europe.

Although uncertainties grew during the year earnings were excellent in many companies. Another reason that weighed heavily on share prices was the rise in interest rates that stemmed from increased inflation.

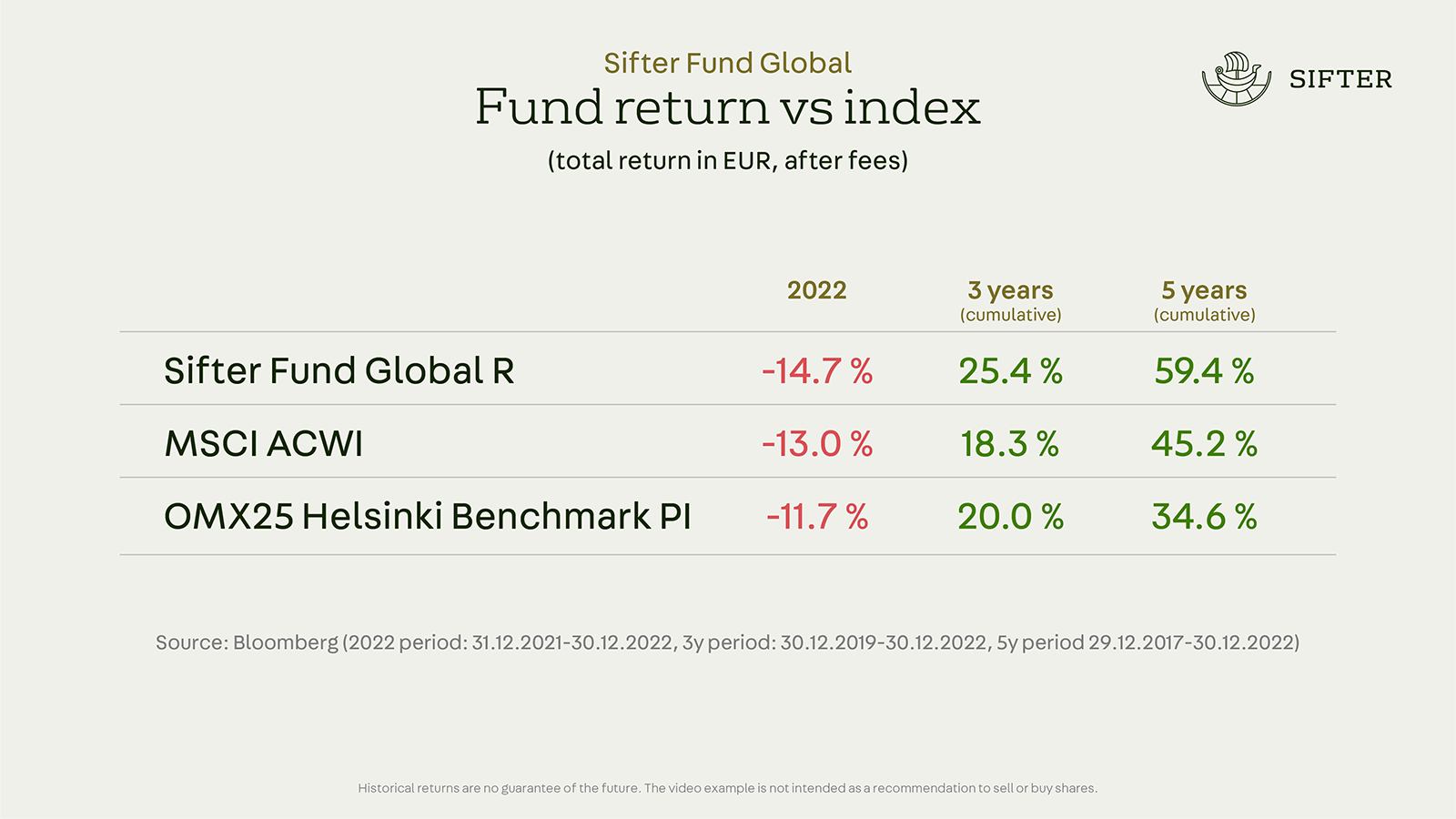

How has the fund performed?

The Sifter fund does not have an official reference index, but we can get an idea of the fund’s returns by comparing it to the world stock index.

During 2022, Sifter underperformed a few percent in both indexes.

When looking at the 3- and 5-year annualized return figures, Sifter’s long-term quality strategy has beaten both indexes.

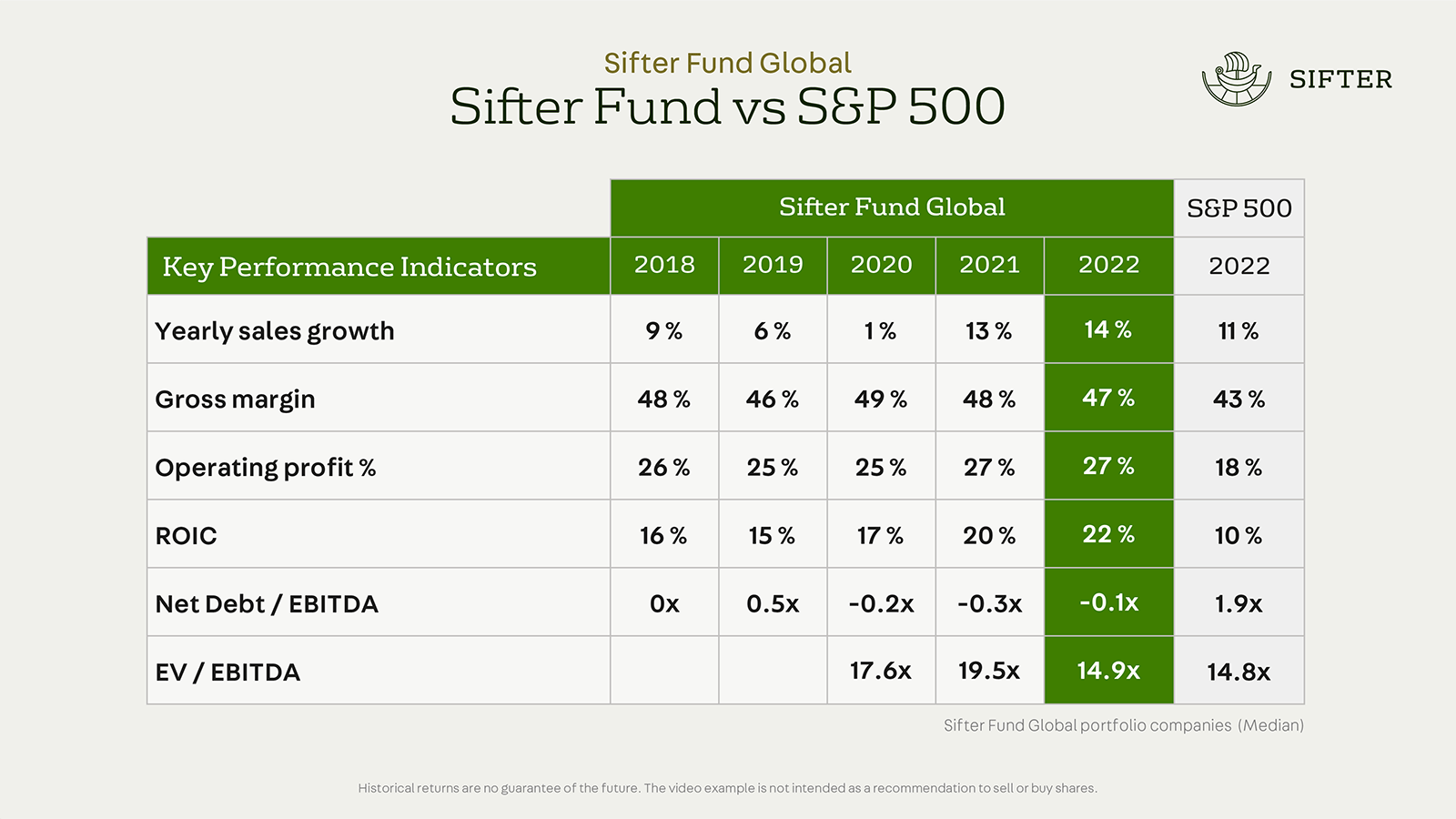

The quality indicators of the Sifter portfolio strengthened

Although share prices fell during the year, the quality indicators of the companies in the Sifter portfolio strengthened compared to the beginning of the year. The sales growth of our companies was higher than a year ago. Also, the profitability indicators remained at a record level, the companies remained debt-free, and the return on invested capital increased.

The Sifter portfolio valuation ratio is at the same level as the average of the S&P 500 companies. However, the business metrics that tell us about the business quality are substantially better.

2022 contributors and detractors

Among the biggest gainers in the portfolio were players from the pharmaceutical industry and the financial sector (Deutsche Boerse), which acted as defensive stocks in a falling market. The weightings of rising stocks (Novo Nordisk, Johnson & Johson, Deutsche Boerse) are among the largest in Sifter’s portfolio.

Contributors (Total Return in EUR)

- Novo Nordisk +29.6%

- Johnson & Johnson +13.0%

- Deutsche Boerse +11.9%

- Safran +9.2%

- North West Company +7.8%

Detractors (Total Return in EUR)

- Koito Manufacturing -38.6%

- Lam Research -36.8%

- Sony Group -35.1%

- Alphabet -35.1%

- TSMC -32.6%

There is no clear denominator among the declining shares in the portfolio. Share prices of companies in the semiconductor industry were falling during the year, anticipating a possible recession and a drop in demand.

At the beginning of 2022, we reduced the exposure of Lam Research in the portfolio, because among other things, its share had risen fairly high during 2021. Koito Manufacturing, a very tiny investment in our portfolio, suffered from weak automotive production volumes in 2022, however, we expect demand to rebound in the future.

We made four new investments in 2022

The share price decline in 2022 created new opportunities to buy high-quality companies at reasonable prices. During the year, we investigated more than fifty new quality companies worldwide.

In the end, we invested in four companies. These new companies have strong earning models, high money-making potential, and a favorable five-year valuation.

We acquired: Universal Music Group, Disney, West Pharmaceuticals, and Applied Materials

We exited companies that no longer met our quality criteria or whose valuation level was too high. In these cases, we wanted to transfer part of the assets to new quality companies with higher return expectations.

We sold entirely: S&P Global, Starbucks

By calmly making changes to both the content and exposure of the portfolio, we will be able to improve the portfolio’s return expectations for the coming years.

The sum of uncertainties is constant – a disciplined strategy determines success

Certainly, macroeconomic uncertainties will not disappear anytime in the future, they just will have different names. Possible new themes will be the cooling economy, the depth of the recession, changes in currencies, and many other things we don’t yet know.

The strong bedrock of Sifter’s investment strategy is the company’s business fundamentals.

We believe that, in long-term investing, the share price will reflect increased earnings in the long term. And finally, we will remain fully invested in high-quality companies and make calm, thoughtful portfolio changes.