After a strong July, the stock market took a breath, and the return of the Sifter fund was -3.0%. Since the beginning of the year, the Fund’s return is -10.7%. Instead of staring at stock price movements, we focused our time on what we know, analyzing the money-making of the companies we own.

In August, we gathered the companies’ quarterly results and evaluated their competitiveness in the current high inflation and rising interest rates environment. The main findings are summarized here.

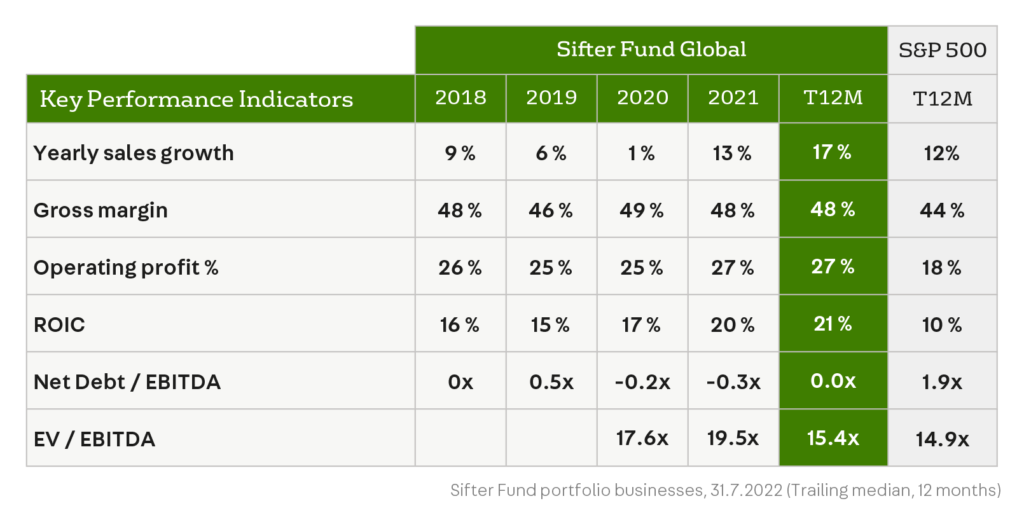

The table shows figures for Sifter companies over several years. The green column shows the latest numbers (July 31, 2022, Trailing median, 12 months), and on the right the corresponding numbers for the 500 largest US companies.

Revenue up +17% from a year ago

One of the quality company’s hallmarks is that it operates in a growing end market. The growth of the end market explains up to 60% of the company’s future success. Even if the market is a narrow niche, the company must find growth pockets where it grows faster than the market.

The pent-up demand after the corona lockdowns increased the revenue of many companies too much last year. Therefore we have focused on monitoring whether the growth continued after pent-up has diminished.

In light of the sales growth figures, the companies’ growth seems to continue.

Sifter companies’ revenue growth increased by 17% (median Q2/2021 vs Q2/2022). Among the fastest growing were the Japanese Disco corporation +36% and the American Old Dominion Freightline 31%. The growing sales are explained by the bigger volumes and price increases that the companies have implemented. Correspondingly, a momentary drop in revenue was seen at Autoliv -7% and Cisco -3%.

We prefer to invest in companies whose products and services are critical for customers. We believe that demand for essential products will remain high even during a downturn.

For example, our newest investment, West Pharmaceutical, makes rubber parts for drug packages, which are critically important for the medicine’s shelf life and, therefore, not easily replaceable.

Investors need to remember that revenue growth alone is not enough. The company must also make increasing profits.

Gross margins 48%, despite cost pressures

Sifter Fund is not only looking for growth companies, but we emphasize very much companies’ predictable and growing money-making ability in our investments. We actively monitor the development of our companies’ gross and net margins.

Companies with a high gross margin can better withstand, for example, price competition and cost pressures brought by high inflation.

The companies’ gross margins (median) in the Sifter fund have remained around 50% for years. Based on Q2 results, margins decreased moderately by two percentage points (48%). The result indicates the companies’ raw material and salary costs have slightly increased during the period. We will monitor this closely in the future.

Operating profit percentages remained high at 27%

Sifter companies generate growing profits. The operating profit margins remained very high (27%, median), although gross margins declined slightly. This figure is the most evident difference to, for example, the corresponding 18% operating profit of S&P 500 companies.

In several earnings calls, the company management explained how they had implemented cost savings programs successfully. For example, Verisign’s operating profit percentage increased, currently at 66%, and correspondingly, Texas Instruments’ operating profit rose to 62%.

It’s nice to own such great money-making machines. In our mind, for a long-term investor, it doesn’t matter if the stock prices are volatile because, as the owner, you own a small piece of the company’s growing profits.

Return on invested capital of 21% (ROIC) swears faith in the future

ROIC is an important metric for investors, which tells a lot about the company’s profitability. We have selected companies with higher than average ROIC for the Sifter portfolio. The median ROIC for Sifter companies is 21%, and for comparison, the average ROIC for S&P 500 companies is 10%.

We believe that when companies invest annually in developing their own business operations (new products, factories, markets, or distribution channels), they can constantly improve their competitive position and make growing profits for their owners in the coming years.

Many investors prefer big dividends. We like the fact that the company invests in the development of its own business. This snowball effect, in our opinion, often offers a better return than dividends (after taxes).

Debt-free companies provide peace of mind against rising interest rates

Sifter companies are, on average, debt-free, unlike S&P 500 companies, which have an average of twice (1.9x) annual EBITDA in debt. We don’t want the owners’ money to be spent on financing costs or a large part of the company’s management time on debt restructuring.

Of course, there are a few exceptions, such as Disney, one of our newest investments. However, we have calculated that Disney can pay off its debt with increasing free cash flows.

Needless to say, the rise in interest rates can affect consumers’ spending, for example, Disney services. That’s why we have calculated very conservative growth and profit forecasts for all our companies and still decided to invest in them.

Quality is never cheap – is it still worth owning quality companies?

In the valuations of our companies, we use the EV/EBITDA formula. Currently, the valuation of the Sifter portfolio is 15.4x EBITDA, and correspondingly, the median of the S&P 500 companies is 14.9x. Sifter’s valuation ratio has decreased by 21 percent from a year ago, i.e., 19.5x last year’s Q2. Why has the valuation come down? First, the share prices have dropped and secondly, the operating margins (EBITDA) have increased.

The decreased valuation levels give indications that quality stocks are cheaper than a year ago.

Factually that is true, but on the other hand, valuation levels are always related to time i.e. mood in the market. In other words, share prices may fall further if the market feels very insecure about the future and doesn’t want to pay too much for companies’ expected cashflows. On the other hand, the market could be ready to pay even more for the growing earnings of the companies, and thus share prices could rise.

What we have learned over the years is that it is worth paying a little more for a growing quality company because the growth of its future cash flows often surprises.

For example, Microsoft’s P/E was as high as 46 at the end of 2017. In hindsight, the high P/E number was justified because Mircosoft’s money-making grew significantly. During the next five years (2017-2022), Mircosoft’s operating profit has increased by c. 25% per year and the share price by more than 300 percent in euros.

What does Sifter do?

Same as before. Our promise to our investors is that we are constantly looking for new quality companies for our portfolio, monitor money-making metrics, and remain 100% invested in chosen quality companies. We don’t know where the market will go next. No one knows.

Santeri Korpinen

CEO, Sifter Fund