For years, Sifter Fund’s largest investments have been Taiwan Semiconductor Manufacturing Company (TSMC) and Lam Research Corporation (LRCX), which operate in the semiconductor sector.

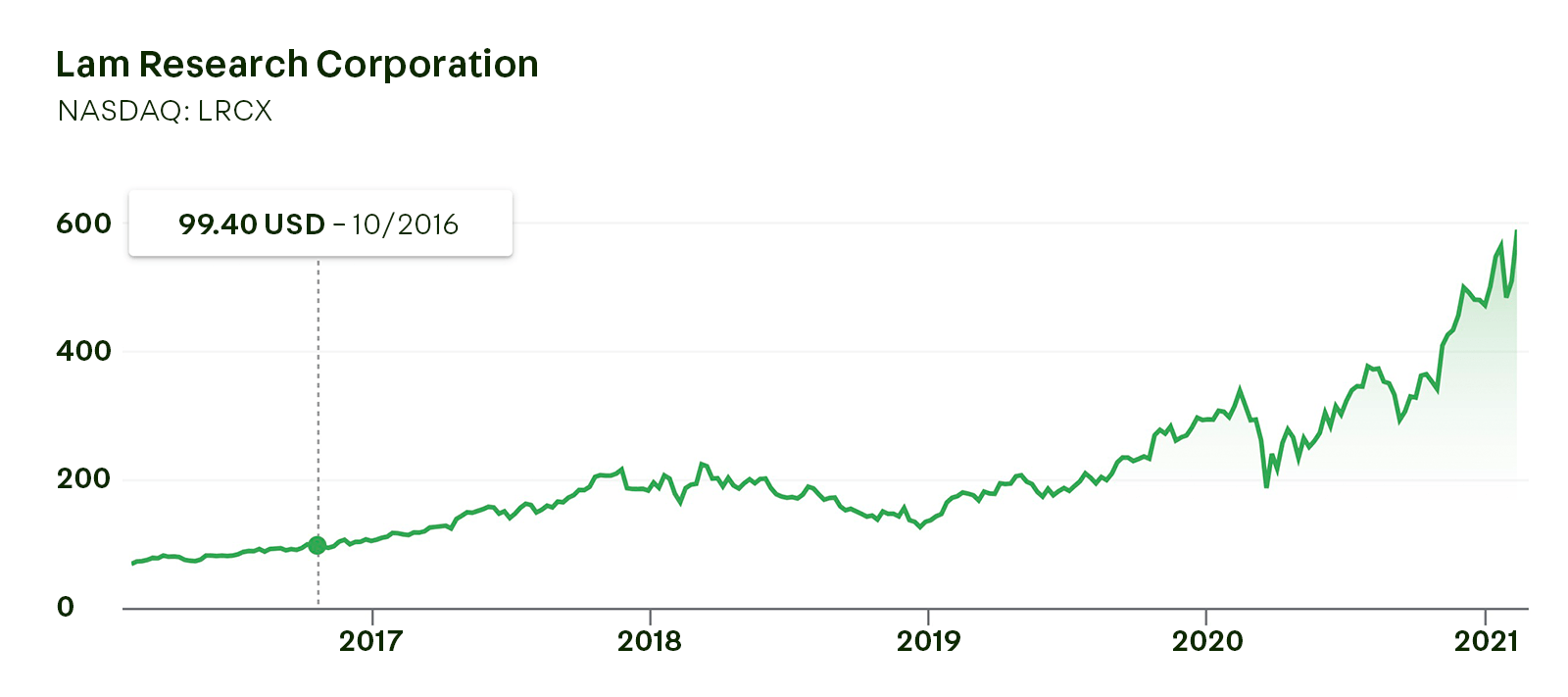

Together, these two semiconductor companies amount to 17% of Sifter Fund’s entire portfolio. They have returned to the Fund since the acquisition, TSMC +464% (6.8.2015–22.2.2021) and Lam Research +416% (18.10.2016–22.2.2021). The returns are in euros excluding dividends.

Why do we find these two semiconductor stocks strong and suitable for Sifter Fund’s long-term equity investment portfolio?

Semiconductors are among the least understood industries, although people use products manufactured by the industry daily – common examples include home electronics and vehicles. At the same time, the semiconductor sector is among the fastest-growing industries in the world.

More than 60% of a company’s future growth is explained by industry growth.

This is why industry growth is one of the five main qualitative criteria we use in selecting companies for Sifter Fund’s long-term portfolio. In this article, we give an overview of the semiconductor’s value chain, the size and growth prospects of the market, and the type of companies included in the value chain. Finally, we give a brief summary of Sifter Fund’s two largest investments.

Learn more about Sifter Fund’s qualitative criteria. Download our Long Term Quality Investing Guide.

The semiconductor industry in a nutshell

What are semiconductors used for? Semiconductors, such as chips, integrated circuits, and processors, are the basic components used in all types of electronics. Today, semiconductors are widely applied in almost every industry, especially in consumer electronics, communication technology, cars, the defense industry, and aviation.

Semiconductors are an “invisible infrastructure”: the consumers, the businesses, and the society could not function without them.

We take it for granted that we can take photos and save thousands of them in our phones. This was not possible 20 years ago. This is one of the things that ever more powerful chips and processors have made possible. During the next ten years, the development of semiconductor technology will enable new things that seem impossible today.

The value chain of the semiconductor industry is diverse

The value chain of the semiconductor industry is long and includes very different kinds of companies. The Bloomberg database, for example, contains around 1,000 listed companies under the Semiconductors class. In addition, there are certainly twice as many unlisted companies.

These companies can be roughly divided into three groups:

Tool and machine manufacturers for semiconductor production

One part of the value chain consists of various manufacturers of tools and machines used by companies in the semiconductor industry. For example, the Japanese Disco Corporation in Sifter’s portfolio manufactures precision dicing saws for cutting microchips. Another company in Sifter’s portfolio, Lam Research, produces devices used in the manufacture of various memory chips.

Contract manufacturers in semiconductors

The machinery mentioned above is used to manufacture technology such as microchips and integrated circuits. These products are mass-produced in laboratory conditions, which is especially demanding and requires significant amounts of capital. This has led to the emergence of contract manufacturers, also referred to as semiconductor foundries, that specialize in certain products. In Sifter’s portfolio, a good example of contract manufacturers is Taiwan Semiconductor, which is the largest player in its field.

Designers and industrial end-users of semiconductors

Finally, companies such as Apple, Nvidia, and others design and integrate ready-made microchips manufactured by foundries in their own products or sell them forward for use in other applications. Semiconductors are everywhere, such as in computers and mobile phones but also in various other industrial applications.

Size and growth prospects of the semiconductor market

It is estimated that the size of the semiconductor market is more than USD 500 billion (2020) and it will grow to 700 billion by 2027. The market demand is estimated to grow moderately by around 5% per year. Of course, growth levels will vary by company and by their role in the semiconductor value chain.

For example, the revenue of TSMC, the largest player in the industry, is expected to grow by 10–15% per year during the next five years.

However, the industry typically suffers from cyclical fluctuations and there is a risk of overproduction.

What trends will increase the demand for semiconductors?

In recent years, factors such as the growing number of smart devices and the decreasing size of electronics and chips have led to increased demand for more and more demanding components. Faster data transfer and storage capabilities also enable totally new business opportunities.

The most important trends include 5G communication, artificial intelligence (AI), self-driving cars, and the Internet of Things (IoT).

5G technology can transfer over 10 times more data than the most advanced forms of 4G technology. Semiconductors, too, must be able to meet these new requirements to keep up in the 5G ecosystem.

The spread of the Internet of Things is another crucial driver in the semiconductor industry. The Internet of Things can be adapted for industrial automation as well as smart devices, which all use semiconductors. As more advanced IoT products enter the market, this offers new and more diverse opportunities for semiconductor manufacturers.

The deployment of artificial intelligence technology is a growing trend in the semiconductor industry. Technavio’s market report forecasts that the growing demand for both AI chips and AI-based applications in various industries will create new growth opportunities for semiconductor companies.

Sifter Fund’s two largest investments in semiconductor stocks

Together, Lam Research Corporation and Taiwan Semiconductor amount to around 18% of Sifter Fund’s entire portfolio. Why do we think these companies are quality long-term investments?

Lam Research Corporation (LRCX)

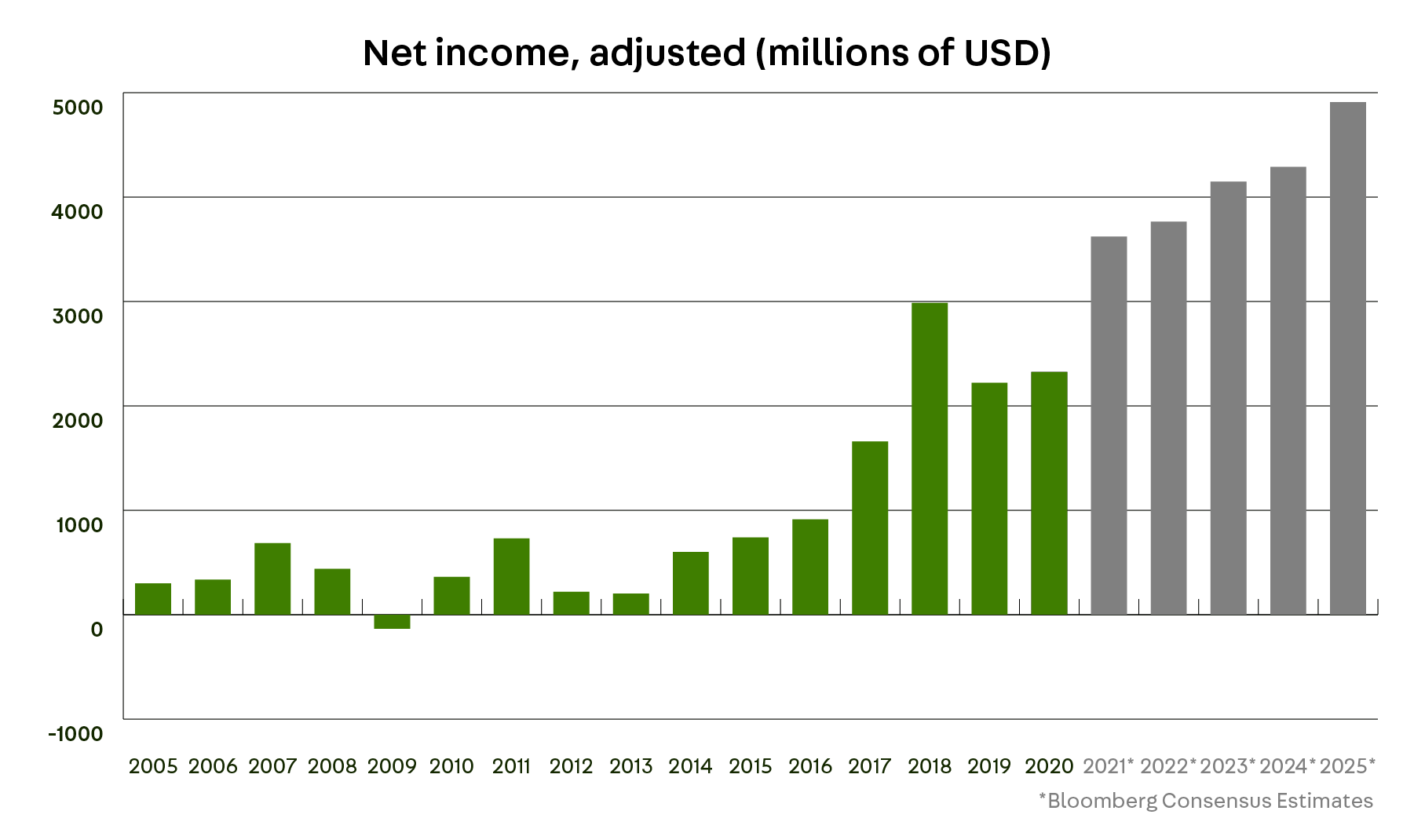

Lam Research is a technology company headquartered in California manufacturing devices for the semiconductor industry. Its client roster includes the largest chip manufacturers in the world, such as Samsung, SK Hynix, Micron, Intel, and Taiwan Semiconductor. The company is the market leader especially in the manufacture of devices used in industrial memory chip production.

Numerical qualitative factors

- The last 5 years’ sales margin steadily around 45% and EBITDA 24–32%

- Return on invested capital (ROIC) 20%, on average, over a 5-year period

- Revenue growth 14% per year, on average, over a 5-year period

- Growth of earnings per share (EPS) 30% per year, on average, over a 5-year period

Competitive advantages and growth prospects

Lam Research is a dominant player in its niche and its competitive advantages stem from its technological superiority.

Lam Research’s customers are expected to increase their investment budgets in the coming years, which will likely further increase the demand for the devices manufactured by Lam Research. According to a forecast by SEMI, global investments in the production equipment of semiconductors will increase by 4% and 6% in 2021 and 2022.

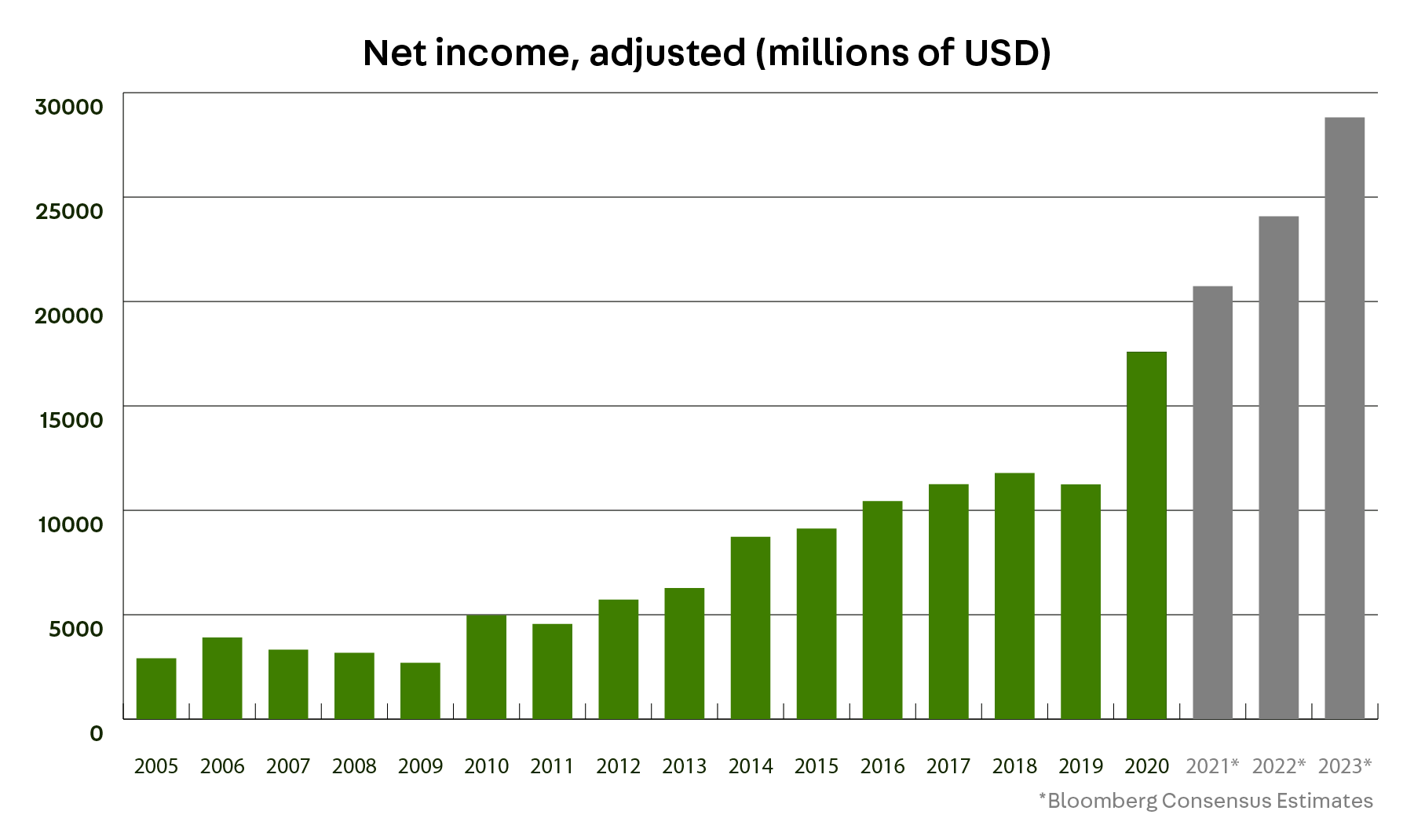

Taiwan Semiconductor Manufacturing Company (TSMC)

TSMC, which is headquartered in Taiwan, is the largest contract manufacturer in the semiconductor industry (also referred to as a semiconductor foundry). Among its other products, TSMC produces 5-nm microchips that manufacturers such as Apple use in their smart phones and other devices.

Apple accounts for more than 20% of TSMC’s revenue.

The company could possibly be the first in the world to launch a 3-nm microchip. TSMC is the only independent foundry able to manufacture the most demanding chips of the next generation. As a result, the company has a strong competitive advantage and high margins. It could be said that TSMC almost has a monopoly in a growing market where the threshold for entering the industry is high and the cumulative learning process is long.

Numerical qualitative factors

- The operating margin 65%, on average, and the EBIT margin 40% over a 5-year period

- Return on invested capital (ROIC) 20%, on average, over a 5-year period

- Revenue growth 9.7% per year, on average, over a 5-year period

- Growth of earnings per share (EPS) 12% per year, on average, over a 5-year period

Growth prospects

The manufacturing of state-of-the-art semiconductors will narrow to fewer and fewer companies and this will grow TSMC’s volumes. At the same time, the price of the services will remain high. TSMC forecasts that its revenue will grow by 10–15% per year, on average, during the next five years.

Industry growth is one of our qualitative investment criteria

When selecting companies for Sifter’s long-term portfolio, industry growth and the intensity of competition is some of the key criteria we assess. However, there are many more qualitative criteria when analyzing companies.

For information on the other criteria, download Long Term Quality Investing Guide. This 20-page guide takes a deep dive into Sifter’s five key investment criteria and also includes five case studies on their application.

Santeri Korpinen

CEO, Sifter Capital Oy