West Pharmaceutical Services (WST) company is not a household name, but every one of us has likely used its products without realizing it. With its roughly $3 billion in annual revenue, West is a goliath in a small but profitable and quickly growing market. There are plenty of reasons to believe the company’s position is firmly entrenched.

Sifter Fund invested in West in June 2022, so let’s dive deeper why we chose to do so, what makes it a quality company and why it is suitable for the Sifter portfolio.

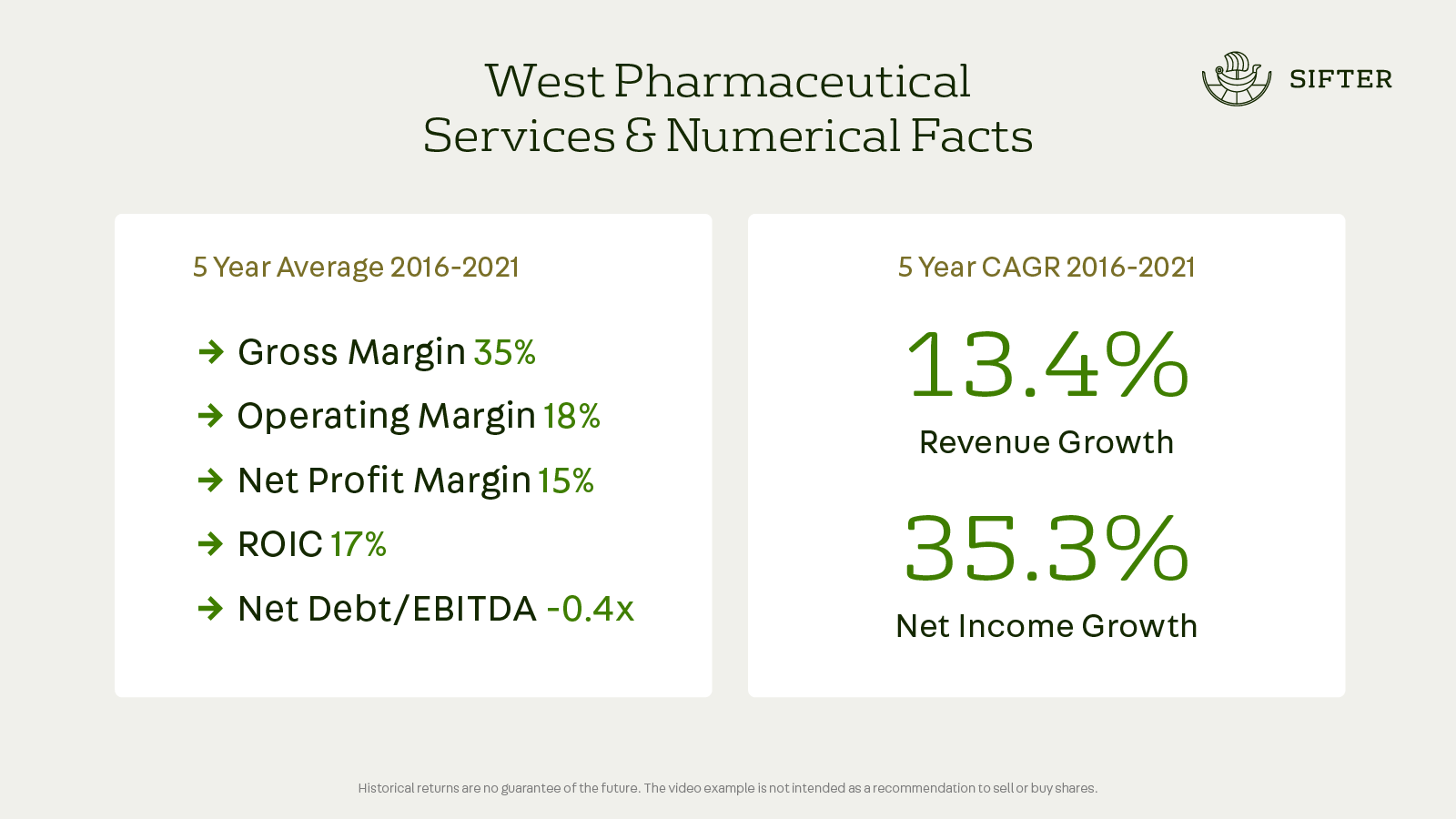

The identification of a quality company always starts off by looking at the numerical facts. These tell us whether the company has demonstrated the ability to produce superior financials, at least historically.

This is in short, the first step in our research process that gives us a reason to believe the potential candidate is worthy of further investigation.

However, numerical superiority indicators are only backwards looking and therefore the heaviest workload for a quality investor is to study the company’s qualitative advantages.

Qualitative superiority factors enable future success

When we find a potential quality company among thousands of candidates we analyze the company’s business using qualitative criteria.

- The earnings model has a clear competitive edge

- High barriers to market entry

- The products and services are critical to customers

- The product represents a minor share of the customer’s total costs

- A large share of the revenue is recurring

- The company’s products possess pricing power

- There is growth in the industry

- Seasoned management team and strong company culture

Essentially, we assess and calculate the firm’s ability and likelihood of producing the same superior, or better financial profile in the future, as it has done in the past.

In this article I’ll summarize our key findings on West and it’s qualitative superiority factors.

How does West Pharmaceutical make money?

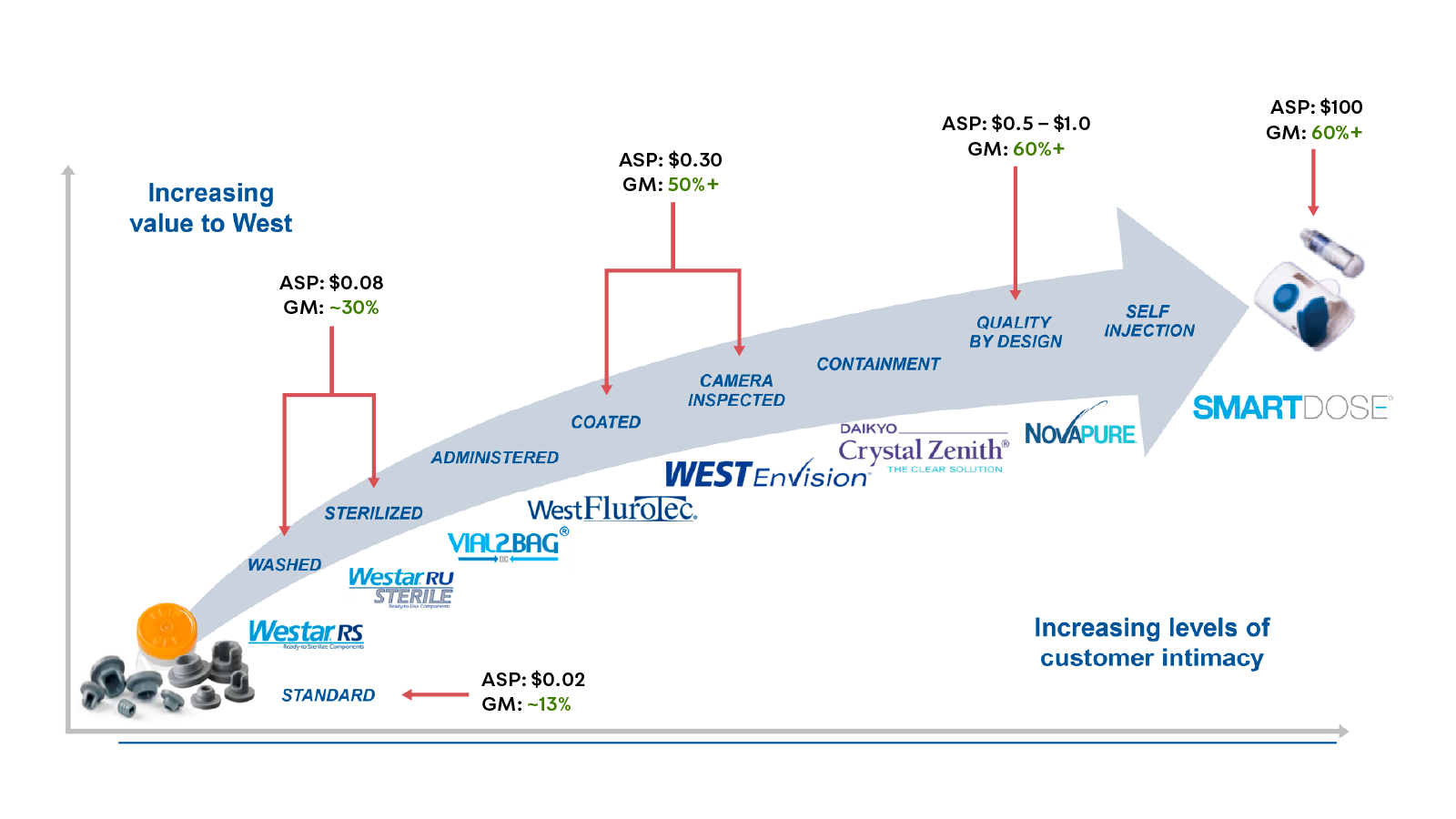

West designs and manufactures drug packaging and delivery products for pharmaceutical companies. More precisely, West’s products are the rubber components that come into physical contact with the drug, such as the cap, stopper, seal, and plungers.

At first glance, these might seem like commodities, low-value products that ought to be mass-produced in a low-cost country, but since this is the pharmaceutical industry, there is a catch. That catch is, of course, that it is of utmost importance that whatever touches the drug does not interfere with its safety and efficacy.

Consider that pharmaceutical companies spend billions and closer to a decade on developing drugs, bringing them to market as soon as possible to get a return on their investment. If the drug must pulled from the market due to contamination from a low-quality rubber stopper, that’s a massive waste of resources and opportunity.

West’s products, although a tiny fraction of the drug’s final cost, are a small but critical piece of the puzzle that ensures pharmaceutical companies can sell safe and effective medicines.

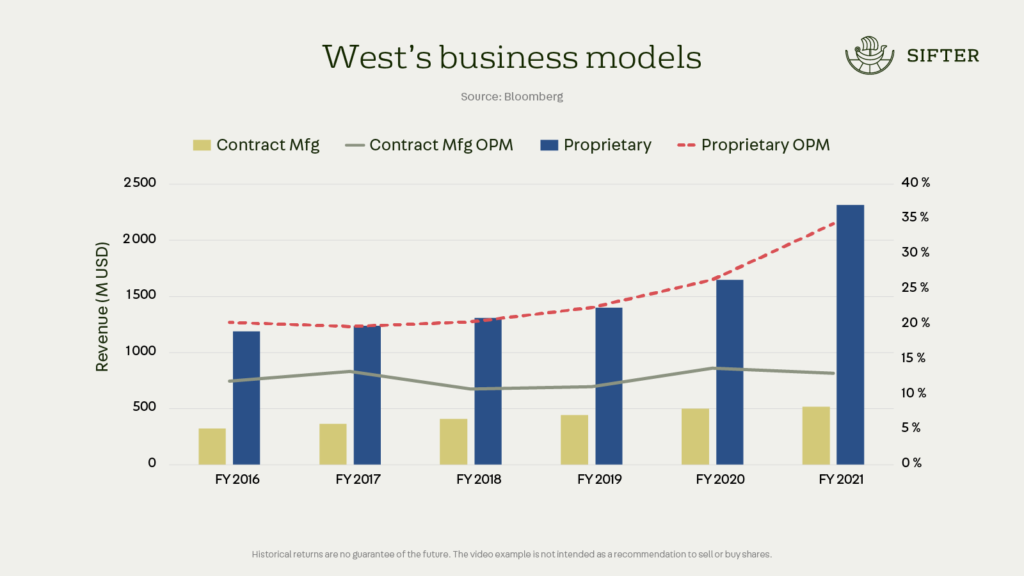

West Pharmaceutical has two business models

Contract manufacturing is roughly 15% of the business in terms of revenue. It is a reasonably stable but uninspiring business where West manufactures medical devices based on its customer’s owned intellectual property. West is, for example, the world’s largest manufacturer of insulin auto-injectors.

The proprietary business is, however, where the magic happens.

West produces a lot of simple rubber components – roughly 40 billion pieces annually. This is the lowest value offering – a standard simple rubber component. But these pieces are not ready to be fitted into the vial or syringe just yet – somebody must wash, sterilize, coat, and inspect them.

Over time, as drug manufacturers have looked to drive down costs, reduce non-core operations, and maintain consistently high-quality components, West has been positioned perfectly to take over this value-add process from its customers.

Through performing increasingly high value-add to the simple rubber components, West has carved out a profitable business.

And again, for the final price of the drug, the cost of West’s operations is a rounding error, but customer’s drug quality cannot be jeopardised.

West Pharmaceutical business is protected by high entry barriers

Now, It wouldn’t be a Sifter business if just anyone could do it. So what are the entry barriers?

If the margins get too attractive, what’s stopping competitors from entering the market?

The answer is the quality risk of switching supplier, technological expertise or resource requirements to build out manufacturing facilities.

The biggest barrier to entry is called the Drug Master File (DMF)

The goal of regulators around the world is to protect the consumers by ensuring the safety and efficacy of drugs. Therefore, very strict regulation requires pharma manufacturers to specify the methods, facilities, manufacturing controls, processing, and, of course, the drug packaging components.

In essence, pharmaceutical companies are required to lock in a recipe for how to make the drug.

While changing the Drug Master File is theoretically possible, it is a very costly process requiring testing and re-approval from the authorities. Therefore, drug manufacturers are, in practice, hesitant to do so, especially for components whose costs are counted in cents per finished product like West products.

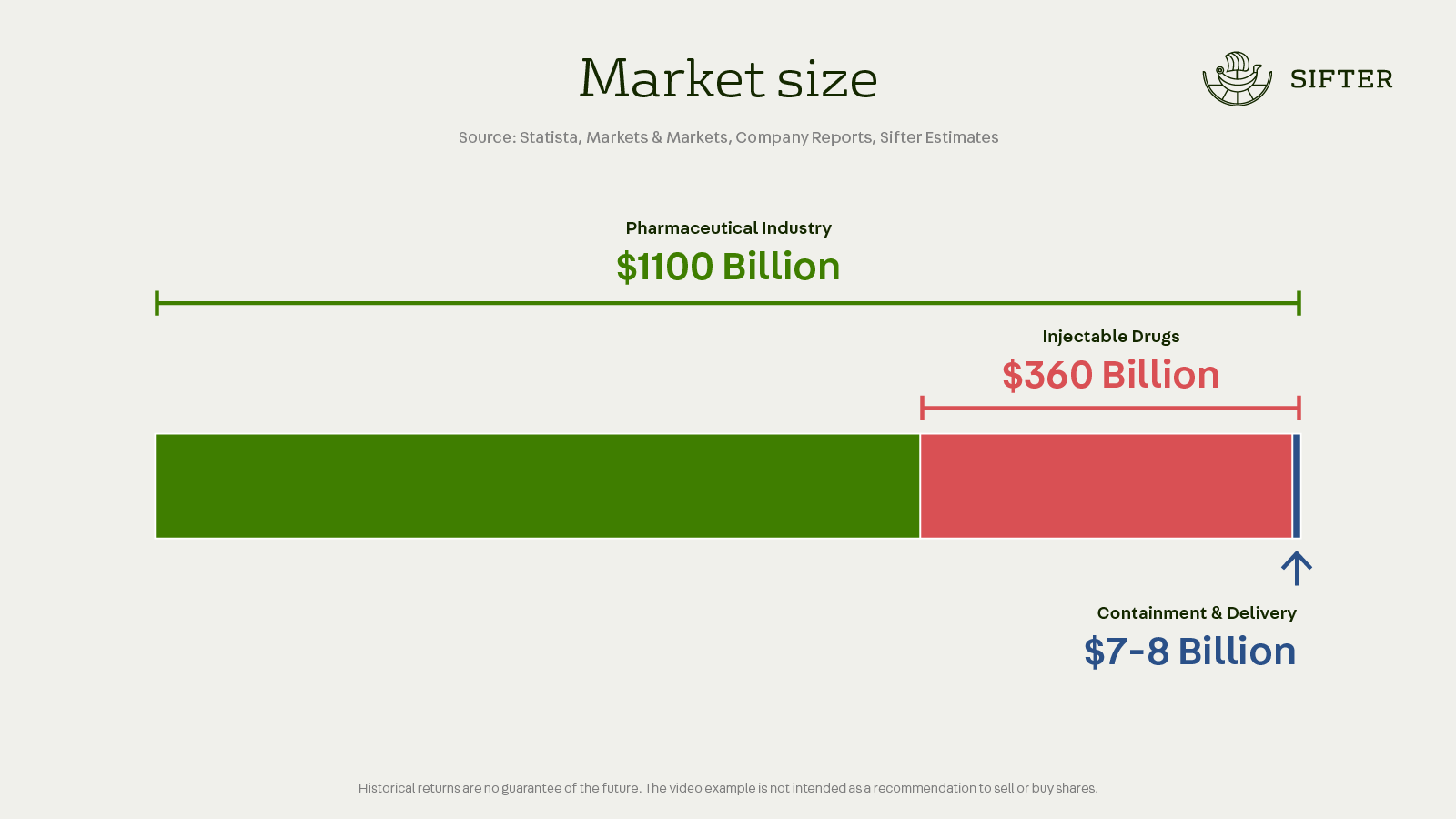

West Pharmaceutical is a market leader in a growing niche-market

So, West has seemingly carved out an attractive niche for itself, but is the underlying market growing? To answer that, we must look closely at the end market – meaning the pharmaceutical industry.

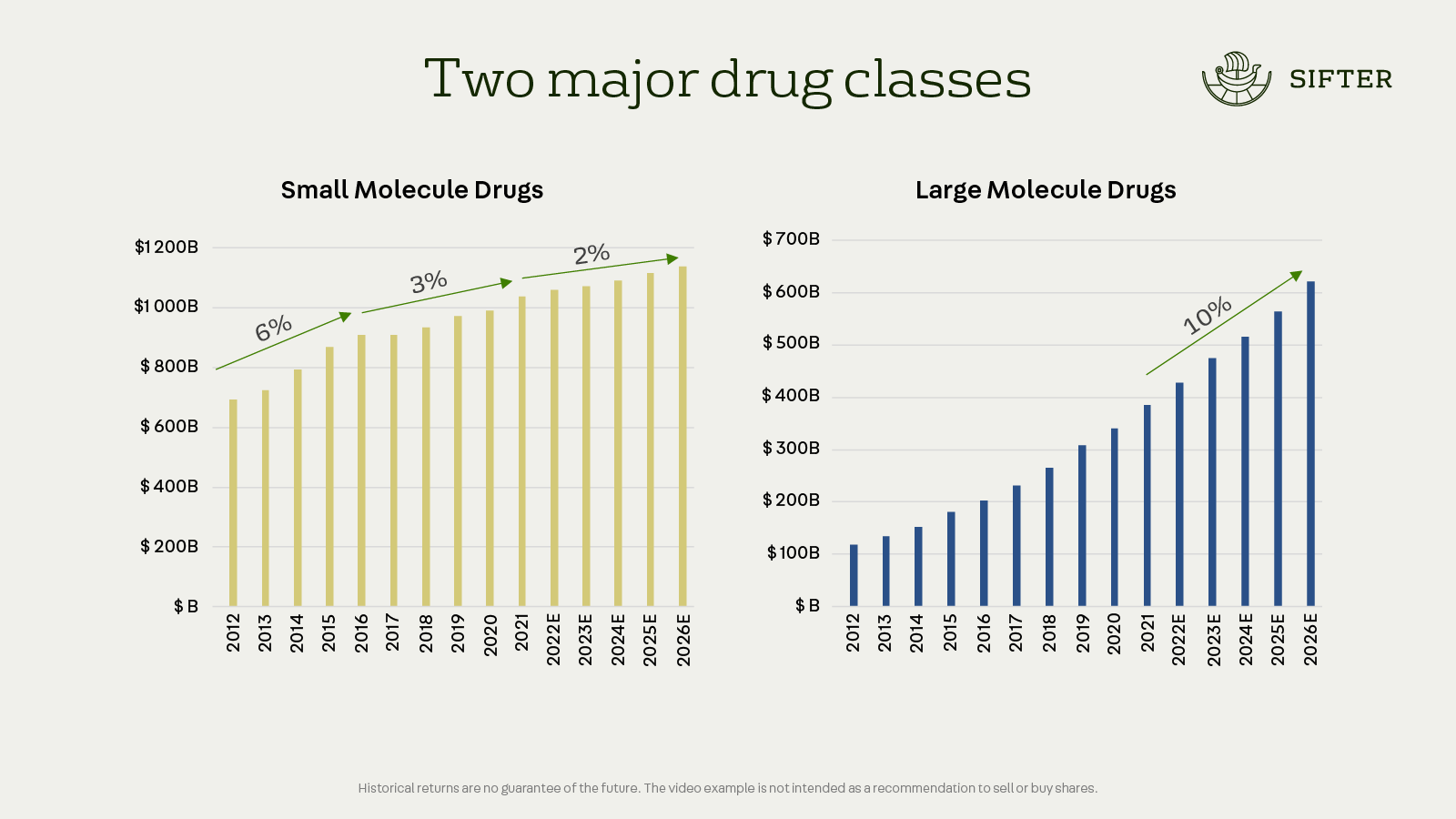

A high-level distinction can be made between two major classes of drugs: small molecule drugs, and large molecule drugs.

Small-molecule drugs are the class of drugs that first comes to mind for most people. Pills that are orally consumed treat an endless variety of ailments and diseases, like simple painkillers. The market growth has been driven by simple factors such as population growth.

Large molecule drugs are, as can be seen in graph, expected to be the growth engine of the wider industry. These are biological drugs, complex molecules made in living cells.

Biologic drugs already make up most of the best-selling medicines treating age and lifestyle-related diseases such as cancer, autoimmune disorders, and diabetes.

A catch of large molecule drugs is that they cannot be orally consumed but are generally injected.

These drugs are also generally more susceptible to contamination and sensitive to heat and light. These factors further increase the demand for high-quality, purposefully designed rubber components.

What are the competitive advantages of West Pharmaceutical?

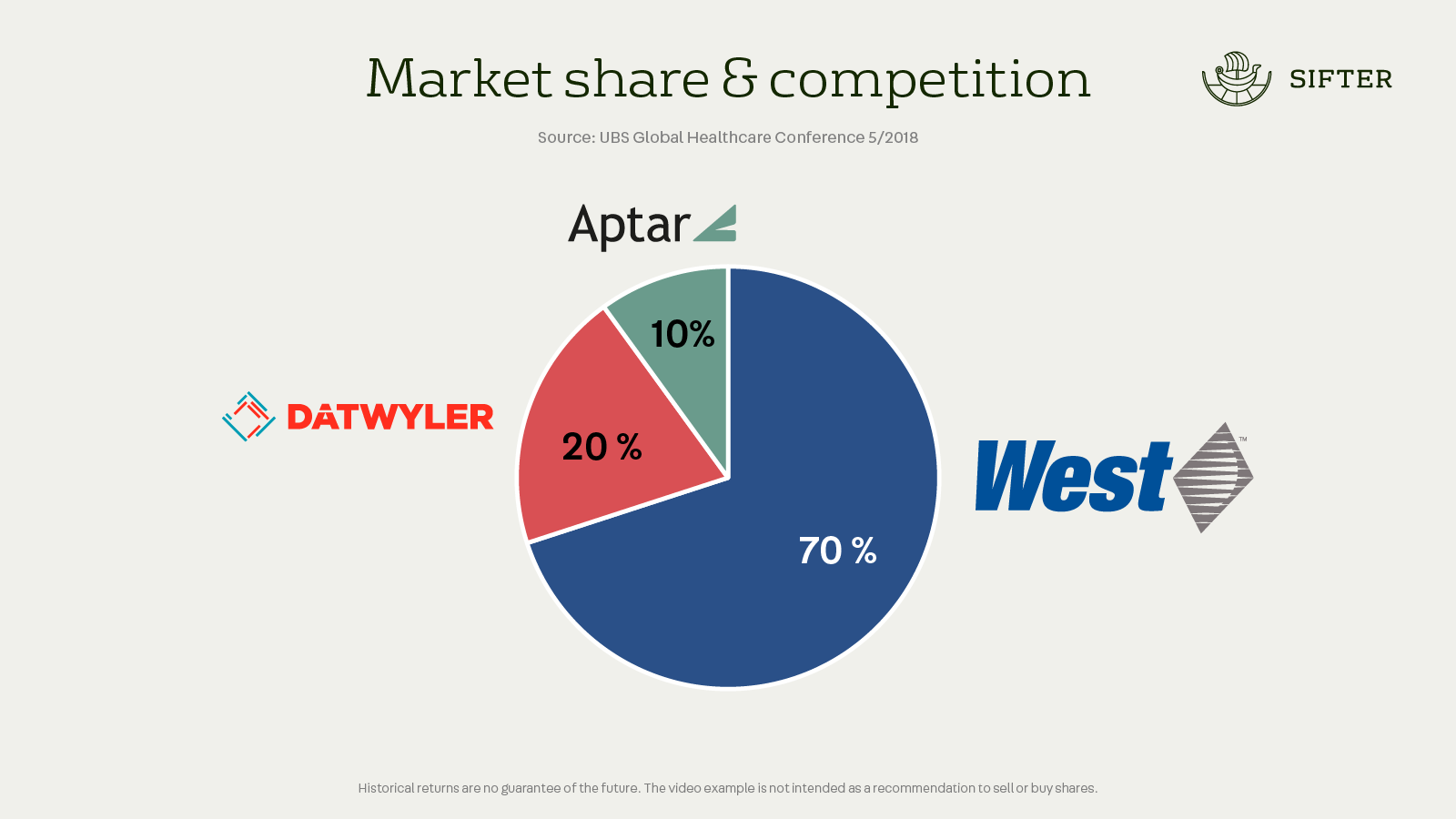

Although West dominates the drug packaging industry with a roughly 70% market share, it is not the only supplier. Dätwyler and Aptar are two formidable competitors with significant elastomeric expertise. So what competitive advantages does West have over these players?

Thanks to West’s leadership position, the company is at the forefront of solving customers’ newest and most demanding challenges and anticipating future needs. West can then apply this accumulated knowledge to serve subsequent customers facing similar issues.

This expertise advantage is visible to us because West has shown an almost monopolistic participation in helping pharmaceutical companies bring the demanding injectables drugs to market.

Secondly, as the largest manufacturer, it has the most significant global manufacturing facility footprint. As a reminder, the components are not interchangeable, so choosing a supplier is done with utmost care. West can best secure supply chain resilience in this regard.

And lastly, choosing a company like West that can fully support you from the start-up to commercialization and whose products have been tested more than anyone else’s, is an attractive prospect for risk-averse pharmaceutical companies.

West Pharmaceutical and investment risks

Finally, we have to consider the risks – What could hurt this business? The general answer is anything that would reduce demand for drug packaging, especially high-quality packaging.

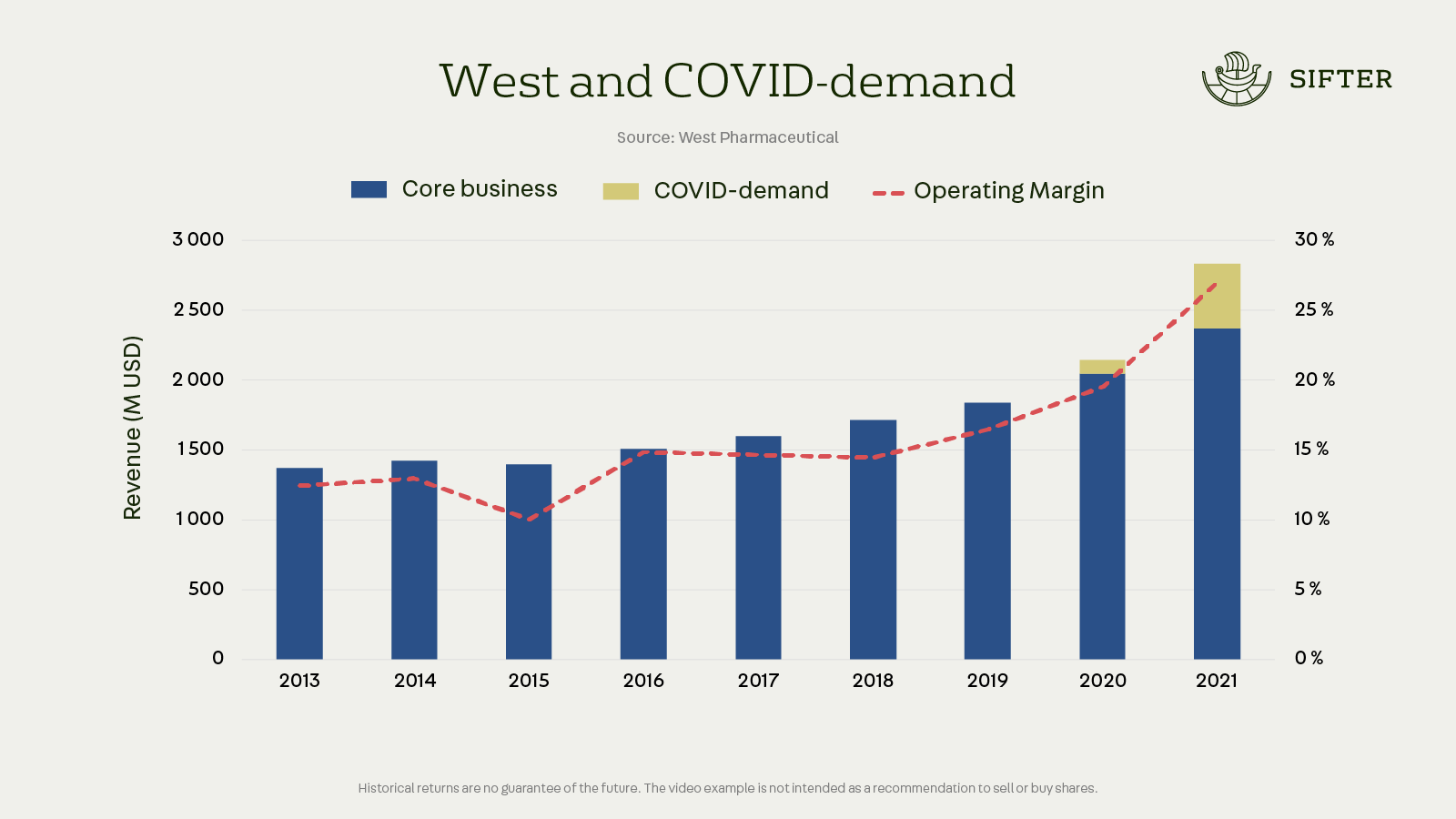

The mRNA-based COVID vaccines are, in fact, biologic drugs, and as you should be able to deduce by now, the explosion in demand resulted in a considerable boost in revenue and profits for West in 2020 and 2021.

And from an investor’s perspective, the company’s valuation is on the high end of our portfolio – the market is not oblivious to the company’s enviable position.

Why did we choose to invest in West Pharmaceutical?

The fundamental strength of West’s business is, without a doubt, very attractive.

1. It has dominant competitive positioning in a growing profitable industry with multiple high entry barriers.

2. The products are critical yet a tiny fraction of the final cost of the products, which are in demand regardless of economic conditions.

3. The company’s management is experienced and consistent, growing nearly solely organically and preserving a clean balance sheet with a net cash position.

We, therefore, see West as an investment that should compound earnings beyond the short-term headwinds and reward the long-term investor.

Karl Lidsle

Analyst