An investor called me somewhat concerned because the Sifter Fund’s performance curve over the past few months is almost vertical. He speculated that the fund’s price increase is due to the US mega-companies, the AI hype, or the rise in Novo Nordisk shares. All these factors are partly true, but there’s more behind the surge.

Disclaimer: The historical performance of the Fund is not a guarantee of future performance.

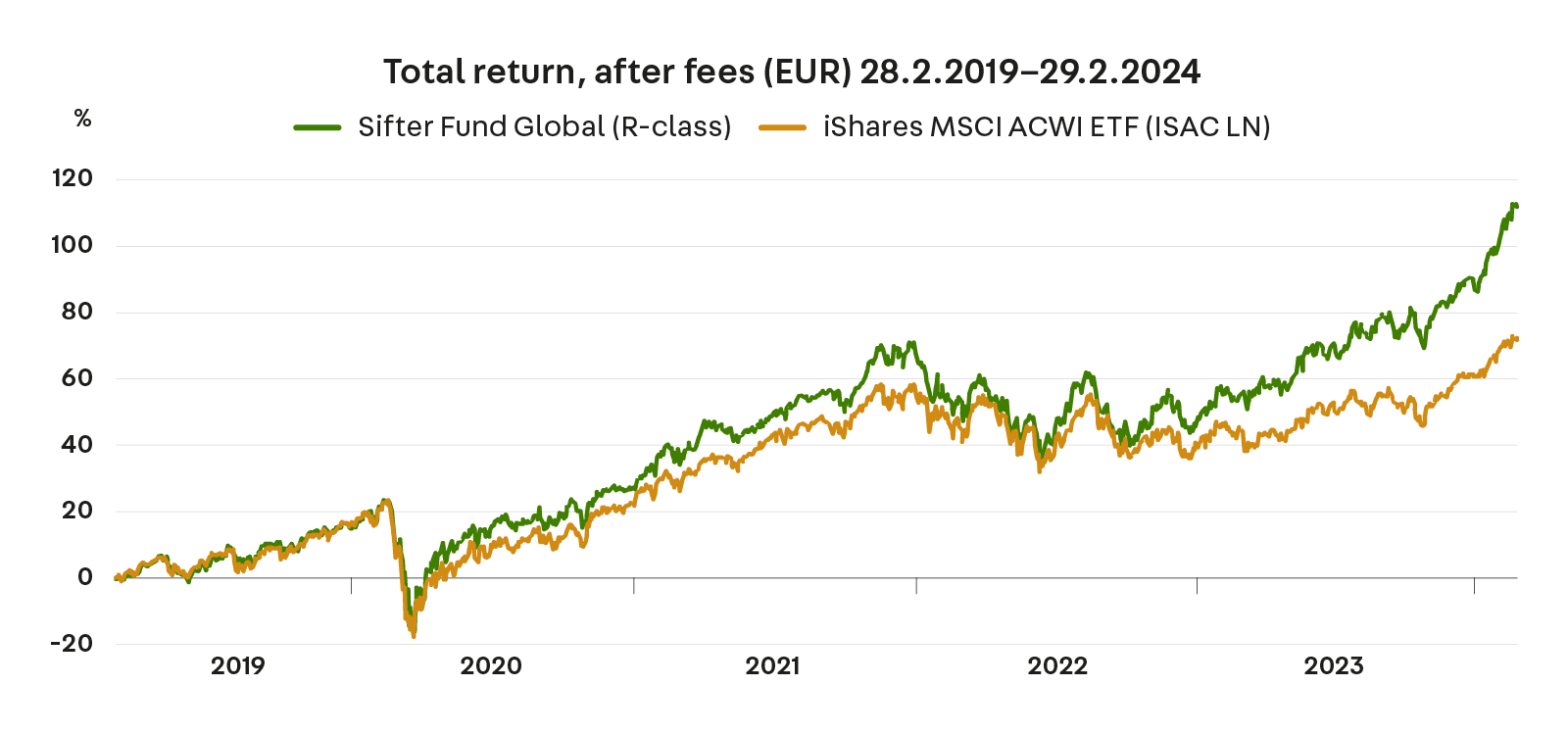

Source: Bloomberg

The value of the Sifter Fund rose by 6.3% during February, and since the beginning of the year, it has accumulated a return of 11.2% (as of February 29, 2024). Adding the exceptional performance of 31% in 2023, one might question if there are justified reasons for the stock price growth.

I aim to clarify the factors leading to the fund’s rise, one by one, below.

1. The United States accounts for 44% of the portfolio

The United States’ share in the Sifter Fund’s country allocation decreased by 5.6% during 2023, ending the year at 44% of the entire fund. The global stock index (MSCI ACWI) has a corresponding figure of 63%.

In other words, compared to the index, the Sifter Fund does not have an excessive weight in the United States. Of the so-called Magnificent Seven companies, Sifter owns only two, Microsoft and Alphabet (Google).

Thus, Sifter’s return does not rely solely on American mega-companies, although they are good businesses.

2. The impact of the AI hype on Sifter is indirect

The impact of Artificial Intelligence (AI) on the Sifter Fund’s portfolio and returns is indirect. For example, we do not own Nvidia, which stock has been skyrocketing in recent years. This is somewhat regrettable since we seriously analyzed the company about five years ago. We should have invested.

However, the uptrend in stocks of AI-related companies has impacted Sifter’s returns.

The demand for chips needed for AI and the equipment to manufacture them currently faces tremendous expectations. These effects are best seen in the results and stock prices of semiconductor companies in the Sifter portfolio such as TSMC and BE semiconductor.

The semiconductor sector’s share is 28% of Sifter’s portfolio, less than a third. This figure does not include, for example, Microsoft, which has also utilized AI in its latest Copilot service.

We estimate, for now, the biggest business benefit for Microsoft has been the use of cloud services needed for AI development, significantly benefiting their cloud service (Azure). This business is growing at about 25–30% annually.

The AI hype has thus supported Sifter’s portfolio returns this and last year, but only with about a third’s weight.

We closely monitor the permanent outcome and competitive advantages AI brings to our companies while assessing whether stock prices have too high expectations in our holdings.

3. Which Sifter stocks have risen over 20% since the beginning of the year?

If it’s not just the AI boom and the United States, what has driven the Sifter Fund’s rise?

For example, the Danish pharmaceutical company Novo Nordisk has been an excellent investment for Sifter in recent years. We managed to buy Novo shares in spring 2020, before the company launched its obesity treatment drug. However, we have steadily reduced Novo’s weight in Sifter’s portfolio.

This year, Novo Nordisk’s stock has risen about 20%, supporting our early-year performance.

However, Novo Nordisk is not the only stock to rise over 20% in January-February 2024. To our pleasure and relief, The Walt Disney Company has also increased over 20% since the beginning of the year and a whopping 36% from its November 2023 lows. Most importantly, it seems like Disney’s business is on the right track after challenging years.

Our newest investment, the Norwegian Tomra Systems, and the French aircraft engine manufacturer Safran, in our portfolio for 7 years, have both risen about 20% this year (January 1, 2024, to February 29, 2024).

In other words, better business results and outlooks for several companies have boosted Sifter’s returns.

Additionally, we have avoided major company-specific price crashes that could occur during earnings announcements.

4. Have risks and valuations grown too much?

I have previously written a more in-depth report on risks. In that article, I noted that the Sifter Fund has not taken on extra risk to achieve returns over the last five years (2019–2024). Risk here refers to traditional portfolio management metrics (Volatility, Alpha, and Sharpe) and compared them to a global stock index.

Despite the rise in stock prices, our five-year valuation metric (earnings yield) has not significantly dropped compared to a year ago. This is because we have received encouraging data on our companies’ long-term outlooks and have modestly adjusted their earnings upwards over a five-year period.

As a precaution, we have always calculated our companies’ forecasted earnings lower than the market expectations.

It’s entirely possible that stocks may generally correct downwards at some point, but this should not be a concern solely for Sifter Fund’s stocks.

5. Is Sifter’s outperformance earned?

Although the Sifter Fund has performed excellently in recent years, not all stocks or indexes have shared in the joy. Many European indexes have been down for several years, not to mention the Helsinki stock market.

Most companies in the US S&P 500 have underperformed in recent years, and only a handful of companies have produced magical returns. In other words, the story of an overheated market is unfamiliar to some investors.

Over the last five years, the Sifter Fund has provided an average annual outperformance of about 4% compared to the global index.

If Sifter’s historical outperformance were so-called debt, it should appear as taking on greater risk. However, this is not the case. According to risk metrics (Volatility, Sharpe), we have not taken on extra risk to achieve returns.

6. Only a handful of companies drive the entire stock market’s gains

If the outperformance is earned, have we just been lucky over the years? Luck’s role can never be underestimated. It’s always a factor. Historically, however, only about 4% of stocks explain the total rise in indexes. 96% of stocks do not perform well. This is evident in the S&P 500 index even now.

A study by Hendrik Bessembinder (2017) analyzed the long-term returns of the US stock market between 1926 and 2015.

The study showed that a few stocks generated most of the market’s total returns, while the majority of stocks did not provide any returns to investors or even lost value.

In other words, identifying the right winning stocks has been a significant factor in attempting to achieve outperformance in the stock market.

An active equity fund must succeed in finding and holding onto winning stocks, of course, following its investment strategy.

Sifter’s strategy is even more precise because we look for only very high-quality companies, which are even fewer among the 4%.

I’d like to believe that over our 20-year history, we have learned to focus and find enough of these 4% winning stocks.

7. What have we done to keep the portfolio healthy?

In February 2024, we re-evaluated the Sifter Fund’s portfolio and consequently decided to make minor changes. The weight of companies that had become too expensive was slightly reduced, and profits were shifted to new companies.

Calmly but decisively, we aim to maintain a high-quality portfolio at a reasonable price.

In addition to the Norwegian Tomra Systems purchased in January, we will invest in at least one entirely new company in March. It is a very boring but predictable and stable medical equipment manufacturing company. More on this company later.

And finally: We still cannot, nor do we want to, predict where the stock market will head in the future. Will growth continue, will AI create an unprecedented super leap in the economy, or will there be a correction in stocks?

We will continue on the chosen path. We own a small group of very high-quality companies globally, monitor them, and swap them out when we find better alternatives.

Santeri Korpinen

CEO