Most investors spend their time thinking about what to buy. Understandably so. Financial media is full of the latest trends, the next high-flying stocks, and companies still offering attractive dividends. What rarely gets discussed is the other side of the trade – when to sell.

A long-term quality investor buys excellent businesses and holds them for years, benefiting from long-term compounding. Yet there are situations where even good companies must be let go.

Sifter Fund’s annual turnover is low – around 10%. In practice, we sell roughly three companies each year and replace them with three new holdings.

Sifter Fund’s strategy defines six situations in which we exit a holding. The first five relate to changes in the business itself, and the sixth to price – specifically, a decline in expected earnings yield.

We sell a stock when:

- the company’s business model or competitive position deteriorates permanently,

- growth in the company’s end market slows,

- significant changes occur in the company’s leadership,

- the company is acquired or completes a major merger,

- we find a better business to replace it,

- the stock price rises too far relative to earnings, causing the earnings yield to fall.

1. The Crumbling Moat: The company’s business model or competitive position deteriorates permanently

We call this the Crumbling Moat scenario – when a once-strong and high-quality company has run into a permanent problem or can no longer evolve beyond its old strategy. It happens.

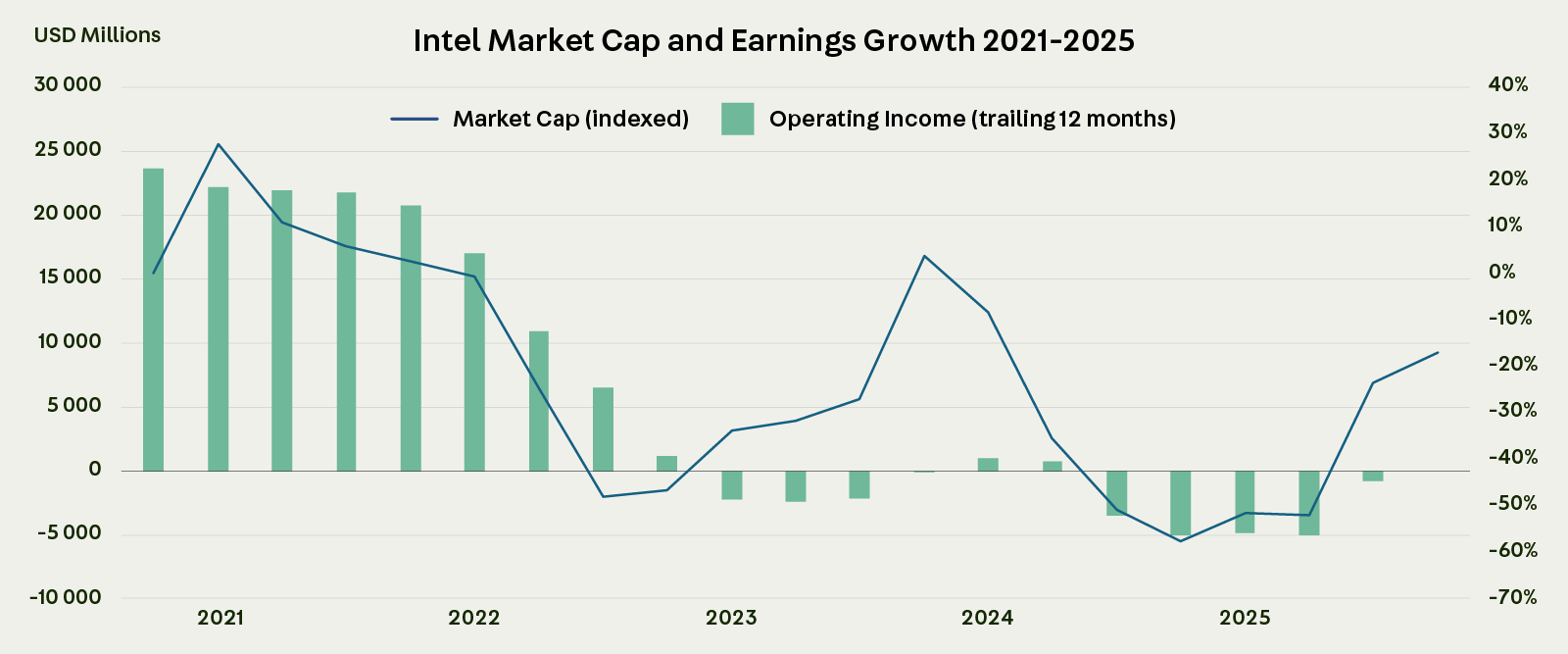

For a long time, Intel was one of the great winners in the semiconductor industry. In 2019, the company ran into serious technology challenges and began losing its lead in manufacturing processes.

We monitored this worrying development closely for over a year, and in October 2020 we thanked Intel for more than 7 years of shared journey – and sold our position.

Over time, Intel’s market share declined, its competitive advantage eroded, and the company fell behind on critical process upgrades.

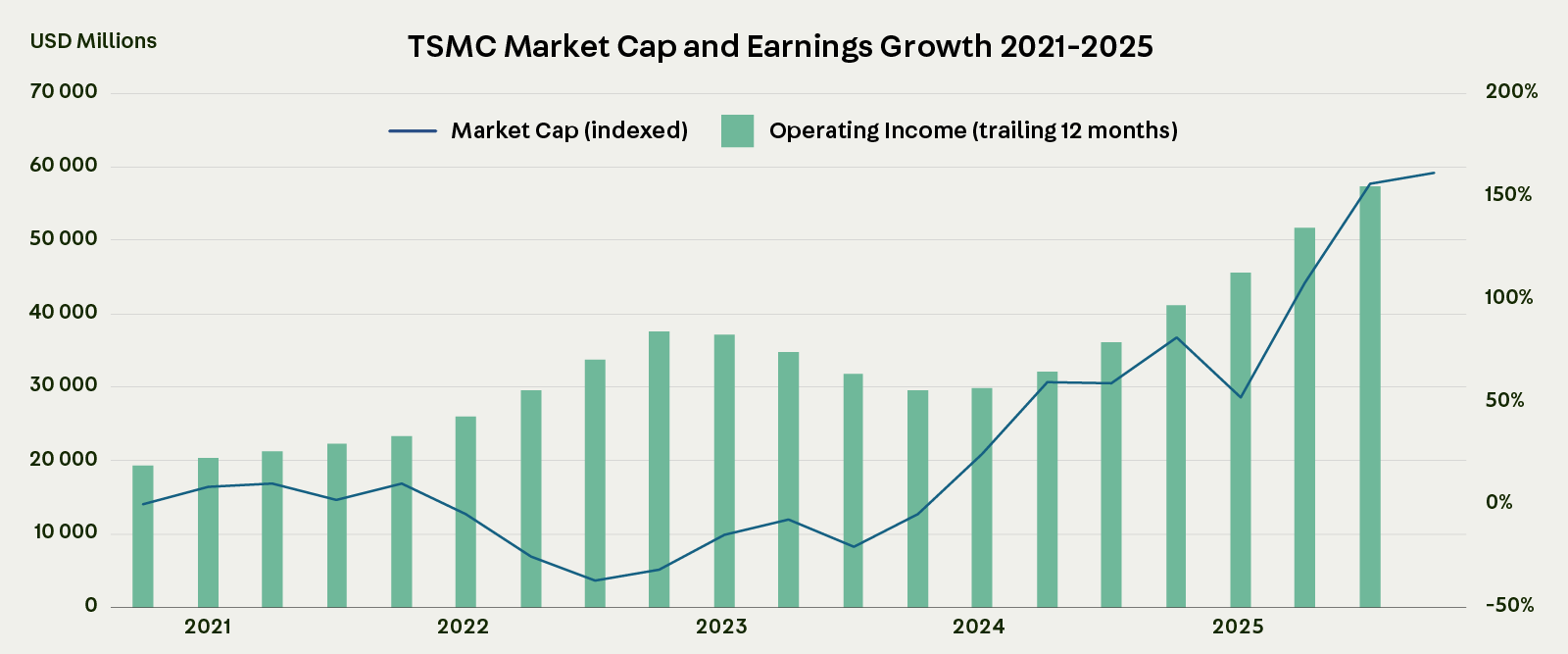

Meanwhile, Intel’s main rival TSMC was consolidating its position as the leading manufacturer of advanced chips. Its technology edge, scale, and reliability ensured that the majority of growth in demand for advanced chips flowed to TSMC.

As the Intel example shows, when competitive advantage weakens and earnings power follows, the share price comes after – and the slope determines the direction.

In our view, there is little reason to own a crumbling moat – even at a low price. For the same reason, we avoid investing in companies that make reckless, last-minute pivots. These stories rarely end well.

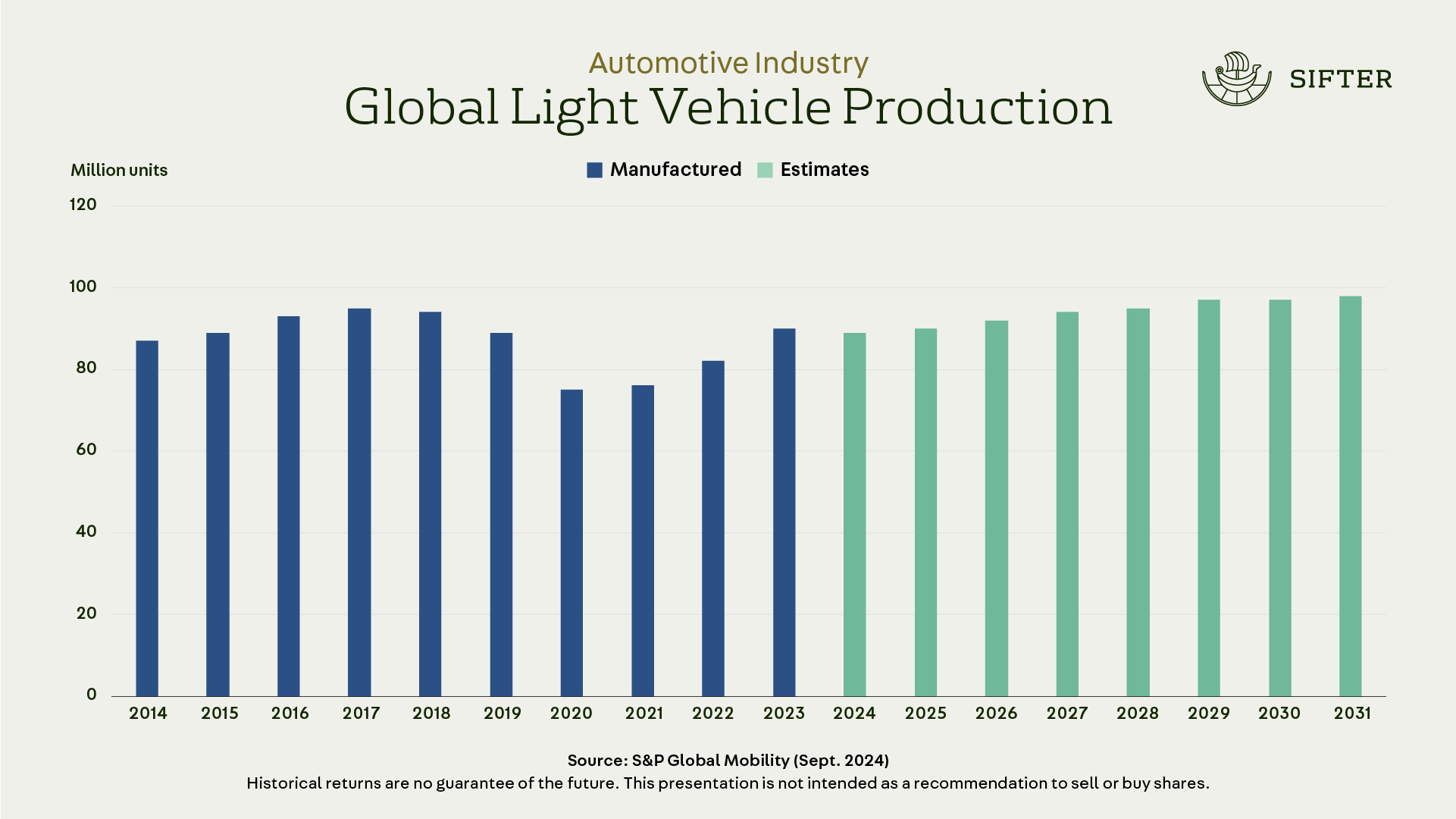

2. Growth in the company’s end market slows

A shrinking end market tends to show up as stalled organic growth, with new growth coming primarily through acquisitions. In our experience, end market demand growth accounts for more than 60% of a company’s long-term success – and is a prerequisite for meaningful cumulative returns over time.

We owned Autoliv for approximately seven years. Autoliv is dependent on new car production volumes. The company manufactures passive safety devices for automobiles, such as, airbags, seatbelts, and related safety components.

By the first half of 2025, it had become clear that Autoliv’s market position was deteriorating. Chinese automakers, notably BYD, were increasingly manufacturing their safety devices in-house rather than sourcing them from external suppliers.

In our view, Autoliv’s end-market growth prospects had been permanently impaired. Although the company’s valuation appeared attractive on traditional metrics, its prospective growth was too modest to justify the investment. We sold the position entirely.

A shrinking industry and end market often leads to price competition, margin erosion, or acquisitions – all of which consume returns that should belong to shareholders.

3. Significant and unexpected leadership changes

When a company’s senior leadership turns over, uncertainty rises – and it may lead us to exit the position.

Disney, for example, changed its CEO twice in three years. That is not a reassuring signal about stability or continuity.

We sold our Disney shares following the leadership changes, though other challenges at the company also weighed on the decision.

Unexpected CEO departures can stem from health issues, misconduct, or simply a more attractive opportunity presenting itself elsewhere. In every case, the company enters a period of at least temporary uncertainty – one that tests the strength of its culture and the resilience of its business model.

That said, this criterion is generally less serious than a Crumbling Moat or a declining end market.

4. The company is acquired or completes a major merger

For Sifter’s holdings, this fairly rare situation has occurred only twice in the past five years.

In the summer of 2020, it happened to Varian Medical, a specialist in cancer treatment devices, when a Siemens subsidiary launched a takeover bid at a 25% premium. We sold our Varian shares because the merged entity no longer met Sifter’s quality criteria.

In our experience, large mergers tend to bring new strategies, consume management’s time and focus, and can erode the sharp edge that made a company excellent in the first place.

5. We find a better business to replace it

The guiding principle of managing the Sifter portfolio is to own a small group of companies – around 30 – and to rotate them when we find something better or more attractively priced.

A pure buy-and-hold approach doesn’t work, because companies change – and sometimes you simply have to sell, dispassionately.

At the same time, our experience suggests it is easier to buy and hold truly excellent businesses for a long time than to constantly rotate positions in pursuit of short-term gains.

Each year we conduct in-depth research on around 30 to 50 companies. Typically, only three new ones make it into the portfolio. We always try to find reasons not to invest. When we can’t find a compelling reason to stay out – and the company’s quality and valuation strengthen the portfolio as a whole – we make the decision to invest.

6. The stock price rises too far, causing the earnings yield to fall

We call this the Price Matters scenario – when a stock has, in our view, risen too far relative to the company’s earnings power over a five-year horizon.

In Sifter’s investment philosophy, price plays an unusually small – but ultimately important – role. We believe it is more valuable to own excellent businesses for a long time than to speculate on short-term price movements.

Over the short term, stock prices can swing well above or below the underlying value of a business, driven more by emotion and macroeconomic sentiment than by fundamentals. Over the longer term – five years or more – a company’s true value and its stock price tend to align more often than most people expect.

We never set price targets for any stock, short- or long-term. Instead, all of the fund’s holdings are ranked by risk-adjusted earnings yield over a five-year horizon.

Quality companies do not always need to be sold outright, even after a strong run. Sometimes the more disciplined move is simply to reduce the position – by a third, or even by half.

Trimming a position is risk management

Over the years, we have learned that truly excellent companies are rare. Once you sell a good one entirely, getting back in can be surprisingly difficult. The reason is often psychological: buying back a sold position at a higher price feels wrong.

For that reason, reducing rather than eliminating a position is often the better approach.

Trimming or adding to a position gives the investor two options. If the stock continues to rise, you still participate in the upside. If it pulls back, you have the opportunity to add at a more attractive price.

We update the relative ranking of our holdings four times a year, and make gradual adjustments to the portfolio accordingly. As a rule, it rarely pays to tinker too much.

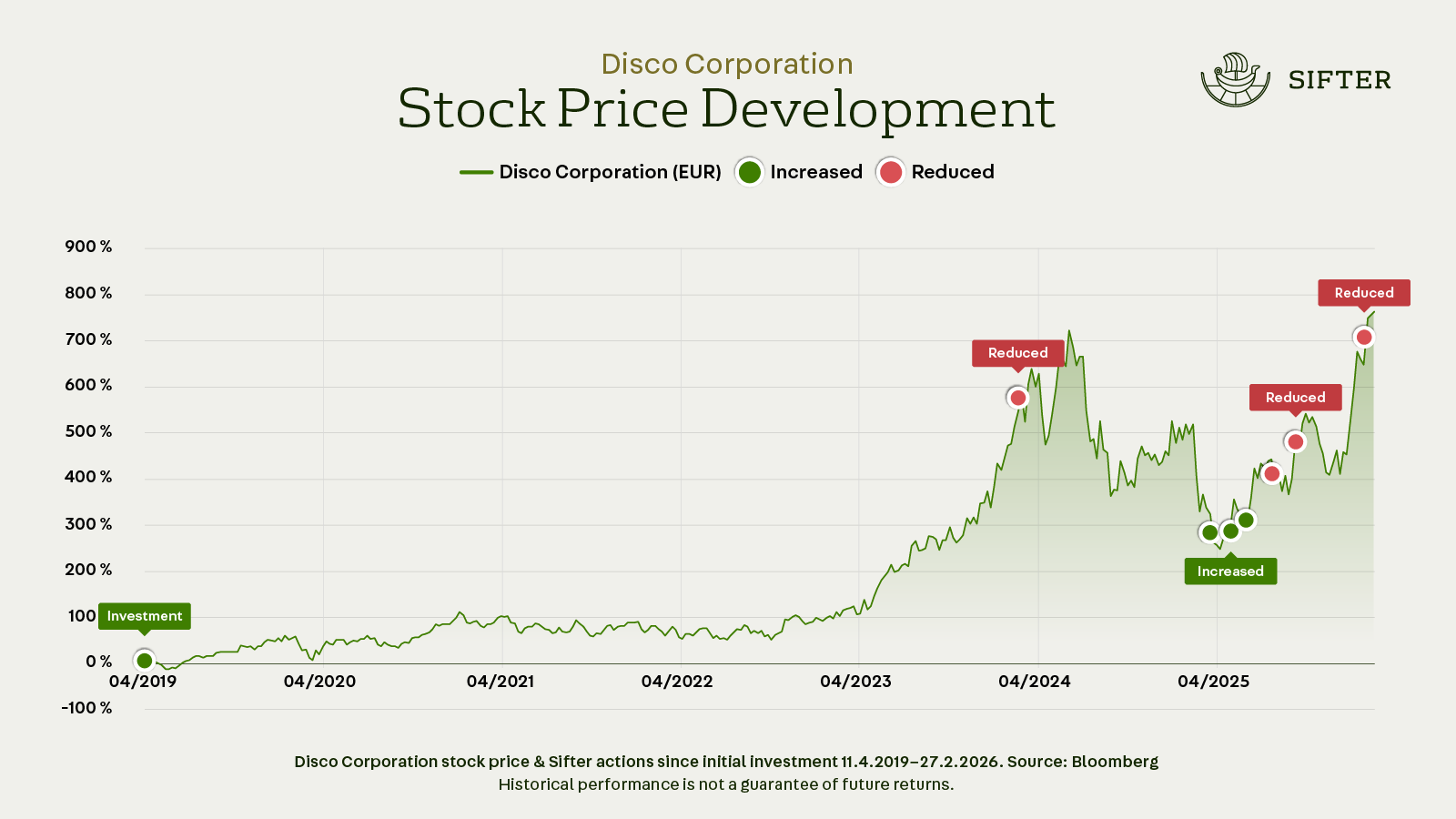

Cyclicality affects position sizing

Some industries are more cyclical by nature than others. In semiconductors in particular, long investment cycles have historically been quite pronounced.

We have often reduced our semiconductor positions ahead of cycle peaks, and added to them near cycle troughs.

This approach is not about predicting short-term market moves. It is about maintaining a longer perspective.

We use a five-year investment horizon, which helps us look through the noise of short-term price fluctuations and earnings volatility. When the time horizon is long enough, cycles become easier to identify. Trimming an overvalued position slightly too early is not a problem.

Reducing a position is an important tool for managing risk.

When selling, there is no room for emotion

Don’t fall in love with your stocks. A frog does not become a prince, no matter how long you wait and hope. If a company’s business is deteriorating, the share price will eventually follow.

There is no guarantee that a troubled business will recover its profitability, or that its stock will return to previous highs. If anything, the evidence suggests that even the world’s best companies eventually meet their match – and what was once a brilliant business fades and disappears.

If you see your investment heading in the wrong direction, sell. The earlier you act, the better off you will be.

Interested in long-term quality investing? Download our 20-page guide: Long-Term Quality Investing. In it, we explain how time and quality companies work in the investor’s favour.

Santeri Korpinen

CEO