During the April market crash, one of our investors asked an honest question: Why do we speak so positively about stocks when the news is filled with threats and uncertainty?

I replied that we’re not optimistic about stocks per se — we’re optimistic about the underlying businesses and their strength.

The stock market is volatile and unpredictable, but the operations of a high-quality company are surprisingly predictable.

In the Short Term, Stock Markets Reflect Investor Sentiment

Economic conditions and key figures do influence share prices, but more often they reinforce the prevailing mood — rarely do they change it.

When strong momentum takes hold, even bad news isn’t enough to extinguish optimism.

Investors check their portfolios even at traffic lights — not because they’re about to make a decision, but because a brief rise in share prices gives a momentary dopamine rush.

If a stock price were an animal, it would be the zoo’s most popular attraction — the one you simply can’t ignore.

In recent years, stock market crashes have become faster. Whereas downturns used to last over a year, today confidence in stocks often returns within weeks or months.

Even though the pace of the stock market has accelerated, the underlying businesses haven’t changed at the same speed.

The Conflict Between Short-Term and Long-Term Thinking

Warren Buffett summed up this contradiction decades ago:

In the short run, the stock market is a voting machine; in the long run, it’s a weighing machine.

In the voting machine, declining sentiment causes concern and rising sentiment brings joy. Many investors move with this mechanism — their moods and decisions fluctuate with market sentiment.

But a company’s business is a different story altogether.

Does a Company’s Business Really Change as Fast as its Stock Price?

Very rarely. Few companies genuinely experience a 30% change in their value over a short time — even if the stock price moves 30% up or down tomorrow.

When that happens, it’s usually due to an exceptional event: a major acquisition, regulatory approval of a new drug, a technological breakthrough, or a serious business risk.

The weighing machine, however, doesn’t lie.

Over the long term, a stock’s price reflects the company’s ability to generate profits — how much real cash flow it delivers to its shareholders.

This is the weighing machine Buffett referred to. And this is the steady truth we rely on at Sifter — not on short-term market fluctuations, but on the quality of the business and its ability to grow it’s earnings.

That’s why we speak optimistically about stocks — or more accurately, about companies — even in the middle of a storm.

Where do Long-Term Stock Market Returns Come From?

Simply put, the expected return of a stock is built on two key components: earnings growth and dividends.

Between 2019 and 2024, the companies in the Sifter Fund portfolio grew their earnings by an average of 12% annually and paid out dividends of about 2%.

So, a 14% annual return would have been a reasonable expectation. But why was Sifter Fund’s actual average annual return around 16% over the same period*?

The answer lies in a third driver of returns — valuation multiples.

When market sentiment is positive, investors are willing to pay more for future earnings — which pushes stock price valuations even higher. This isn’t about changes in business performance, but rather in mood.

*Period from December 31, 2018 to December 31, 2024. Sifter Fund Global PA share class: 15.79%, and Sifter Fund Global PI share class: 16.23%. Please remember that past performance is not indicative of future results.

What do the Next Five Years Look Like?

We’ve selected companies for the Sifter portfolio that we believe will continue to grow their earnings in a predictable way over the next five years.

Our conservative estimate is that the operating profit of Sifter’s portfolio companies will grow by approximately 9% per year on average.

We expect dividends to fall within the 1–2% range. However a high dividend yield is not a key criterion for our investment decisions.

While market consensus expects stronger earnings growth figures, Sifter’s forecasts are almost always more cautious.

Can a Sifter Investor Expect 9–10% Annual Returns?

Unfortunately, we can’t promise that — not because the companies would fail, but because stock markets are inherently unpredictable.

At times, the market behaves like it’s in a mania, pushing stock prices up by 30% in a year. But such excess often ends in a hangover — both emotional and financial. In the years that follow, valuations tend to adjust — sometimes sharply.

Why Do We Believe in Quality Companies?

The short answer: a high-quality business offers its owners predictable and growing earnings well into the future.

When you buy shares in such a company at a reasonable price today, it’s realistic to expect higher earnings per share five years from now.

That means growing cash flow and long-term shareholder value. And often, the stock price tends to follow — albeit unevenly.

What Enables Predictable and Growing Earnings?

Sifter’s team spends over 5,000 hours a year on research — precisely to ensure that our portfolio companies remain high quality and continue to grow their earnings.

1. High Barriers to Entry

Companies whose businesses are protected by high barriers to entry are better shielded from price competition and can grow with less disruption.

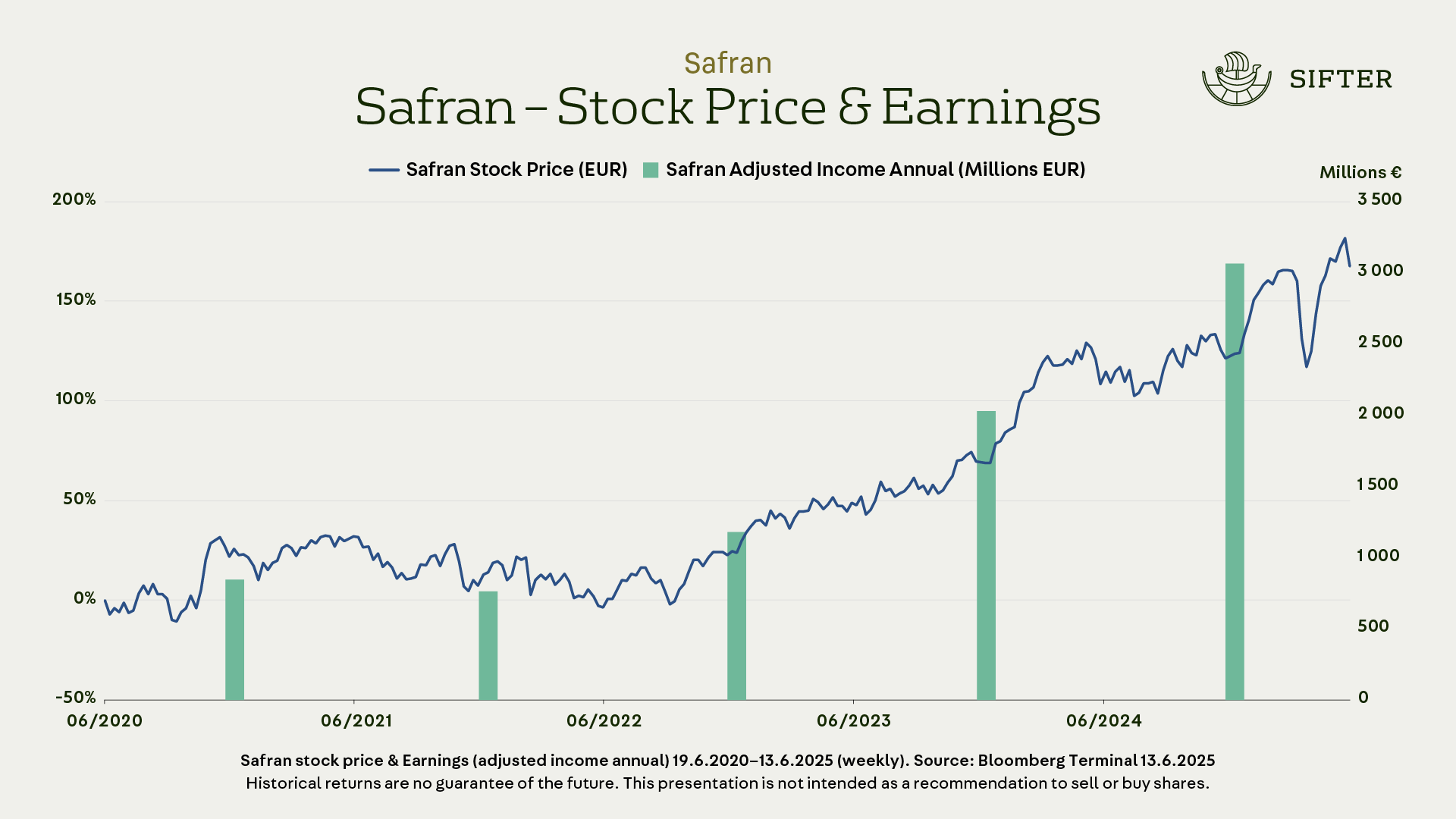

For example, aircraft engine manufacturer Safran operates in a highly regulated industry, which creates predictable and stable business conditions.

2. High Margins and Pricing Power

When a company’s products or services are critical to its customers, it can raise prices without losing significant business.

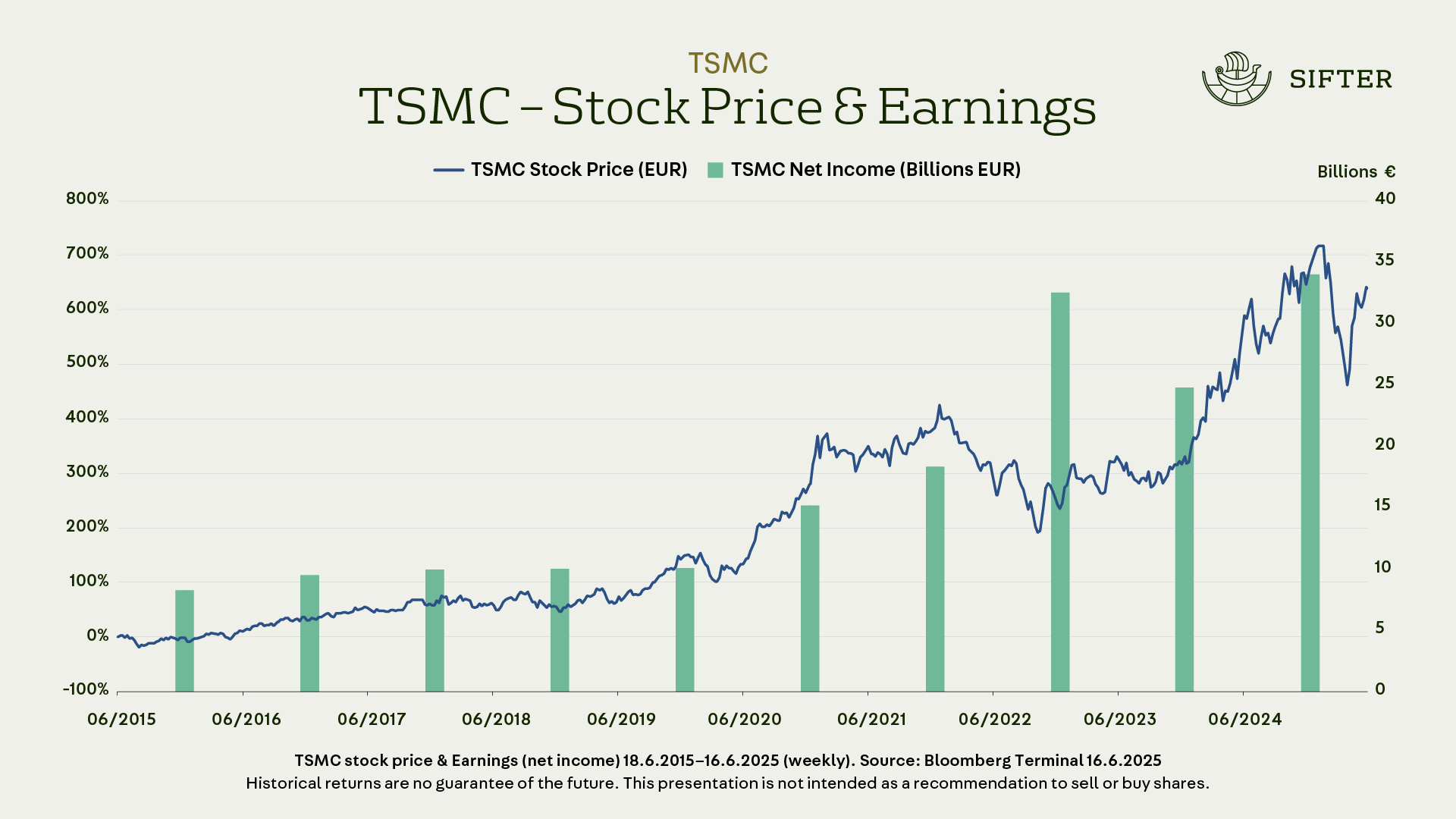

TSMC, the world’s largest independent chip manufacturer, is an excellent example of this.

3. Scalable Earnings Model and Loyal Customer Base

Costco is a great example of this with its membership-based model — membership fees go directly to the bottom line.

At the same time, purchases by new members improve the company’s economies of scale, further boosting profitability.

4. Growing End Market

Quality companies are often market leaders in focused segments — either globally or locally. They operate in industries where end demand is rising, and they capture a large share of that growth.

In addition, they typically invest 5–15% of their revenue in R&D to maintain their leadership position, which in turn earns them higher margins than their competitors.

5. Strong Leadership and Clear Strategy

Quality companies are led by management teams that think like owners. They understand the company’s strengths and follow a long-term strategy.

This strategy brings clarity, predictability, and consistency to decision-making — even in challenging times.

Summary

It’s hard not to like quality companies.

While stock markets react quickly, the underlying business often continue steadily.

That’s why market downturns can offer long-term investors a chance to buy quality at a discount.

And that’s exactly why we speak optimistically about stocks — or more accurately, about the businesses behind them — especially when the rest of the world sees only headlines and fear.

Santeri Korpinen

CEO