Long-term investment and diversification are two of the golden rules of equity investment. Historically, applying these principles has led to good performance.

A diversified portfolio is more resilient to any crises that affect a certain industry or country. During the COVID-19 spring, for example, the role of industry diversification was underscored as companies in the travel and restaurant sectors were hit especially hard.

In this article, we discuss the diversification of the Sifter Fund and how it is accomplished in practice.

A fund helps diversify equity investments

One of the key features and advantages of fund investments is the diversification of risk. The 30 companies in the Sifter Fund currently represent 18 industries and 7 countries. The rules of the fund do not specify the extent to which we can invest in companies in a given industry or country.

Instead, we look for companies that are among the most successful players in their respective industries.

We believe that high-quality companies with strong profit performance can be found in nearly all industries.

The diversification policy of the Sifter Fund

What we believe in

The Sifter Fund has an exceptional investment strategy as we do not believe in pre-defined diversification rules. In practice, this means the following:

- We do not set targets for what proportion of the fund’s shareholdings should be in certain continents or industries.

- What we are interested in are companies and their business. Having a unique business model and a strong capacity to make money is more important to us than a given industry or country. In other words, we apply a bottom-up approach rather than a top-down approach.

- Our investment approach is driven by our elimination process, which leads us to the most attractive companies around the world. When valuations are low in a given industry or country and our quality indicators are satisfied, we focus our research activities on those companies.

We eliminate certain industries

- Banking and insurance – we find that the balance sheets of banking and insurance companies are too hard to understand and may include unpleasant surprises.

- Highly cyclical industries – for example, construction, shipbuilding and other industries in which individual projects are excessively significant and there are dramatic fluctuations in profit performance.

- Industries that are directly linked to raw materials – we exclude oil and gas companies, for example. We do not have an adequate understanding of the development of the prices of these raw materials and their impacts on the companies’ profit performance.

- Bulk industries – for example, companies whose products do not have a clear competitive advantage and who mainly compete on price. We do not believe we will find high-quality and growing companies in these industries.

- Industries that are incompatible with our rules concerning responsibility (ESG), such as tobacco, alcohol, firearms and adult entertainment companies as well as industries in which the reputation and negative environmental impacts of companies are not in line with our criteria.

We also eliminate certain countries and stock exchanges

We exclude countries that have weak investor protection and eliminate countries – such as countries in Africa and the Middle East – where access to high-quality company information is unreliable or the companies’ sustainability indicators fail to satisfy our criteria.

The aim of these elimination principles is to reduce risk.

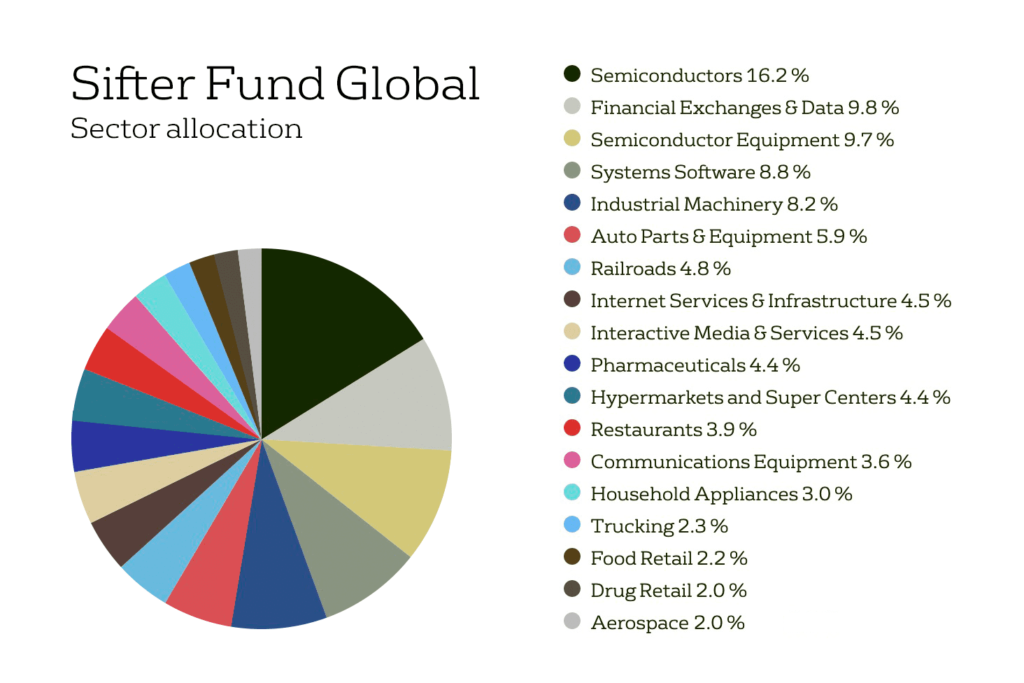

Industry diversification 2020

The Sifter Fund’s largest industry consists of semiconductor manufacturers, such as Taiwan Semiconductor, Lam Research and equipment manufacturers in this field.

Semiconductors, such as chips and integrated circuits, are the basic components used in all types of electronics. Growth in the number of smart devices and the decreasing size of electronics and chips lead to increased demand for these components.

The Sifter Fund’s second-largest industry is stock exchanges and financial data. Examples of the fund’s shareholdings in this category include Deutsche Boerse and S&P Global Inc. While these companies can be broadly included in the financial sector, the nature of their services differs from banks. Their balance sheets are not difficult to interpret, which sets them apart from banks, and their services are largely based on continuous subscriptions, which we believe makes them strong and less cyclical.

The Sifter Fund includes several smaller industries in its portfolio. Their weight in the portfolio is only 2–3% each. In many cases, they are individual companies that are the best and most successful in their respective industries. For example, the trucking industry (2.3%) is represented in Sifter’s portfolio by the US-based Old Dominion Freight Line.

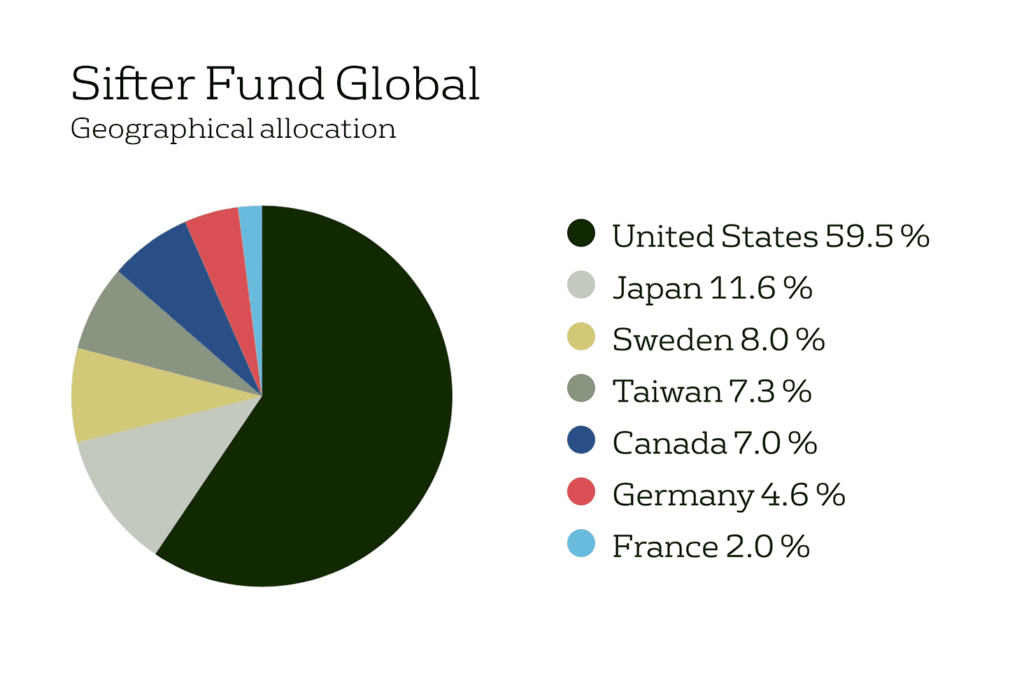

Geographical diversification 2020

We have not set targets for what proportion of the fund’s shareholdings should be in certain continents or countries.

How Sifter’s geographical diversification has changed

North America

- In 2020, North America (US and Canada) represents more than 65% of the Sifter Fund’s shareholdings.

- It is interesting to note that, in 2010, North America represented only about 10% of our portfolio.

- The growth of North America’s proportion of the portfolio’s assets is the result of Sifter’s elimination process rather than an active pre-defined diversification decision.

Asia

- In 2020, Asia (Japan and Taiwan) represented 19% of the Sifter Fund’s shareholdings.

- A decade earlier, in 2010, Asian stocks accounted for nearly 50% of the portfolio.

Europe

- In 2020, Europe represents about 15% of the Sifter Fund’s shareholdings.

- This figure has fluctuated between 13% and 44% during the past decade.

The portfolio’s low turnover means lower costs for investors

Sifter’s investment strategy is based on the key principle of buying high-quality companies for long-term ownership. This approach could be described as buy and watch. What does this mean for us?

We do not believe that we can create added value for our investors by buying and exchanging shares frequently.

Our investment decisions are based on lengthy and in-depth analyses of companies. It would be unfortunate to have to quickly sell the fund’s holdings in a company that we have carefully researched. That would suggest that our analysis of the company would probably have been inaccurate to begin with.

Each year, we study more than 100 new investment opportunities but end up investing in only about 3–5 new companies.

During the past five years, the average turnover of Sifter’s portfolio has been only about 10%. In other words, we have sold the Sifter Fund’s shareholdings in three companies per year on average. As a rule of thumb, a portfolio turnover under 30% is considered low.