Inflation is not a good phenomenon for corporations as the costs of doing business often rises faster than the ability to raise prices of one’s own products and services. Likewise, the increased uncertainty in the economy negatively affects companies’ willingness to invest and expand.

Given these uncertainties, how should an investor position their equity portfolio to reduce the potential negative impacts and ride out the storm?

In this article I argue that quality companies is one of many ways to go, as these are better positioned to protect their profit margins and have better access to capital if the liquidity dries up.

Why are quality companies less affected by inflationary pressure?

Quality companies have a strong fundamental support and solid numeric proof of their superiority. A quality company is in this context generally defined as:

- A strong business model with pricing power and competitive advantages

- A healthy balance sheet with low levels of fixed commitments (little debt and other “maintenance” debt)

- A good management team with a long-term investor friendly focus

- High return on invested capital (ROIC)

What does this mean in practice and how do these characteristics help quality investors during times of inflation?

Want to read more about the quantitative and qualitative factors behind the superiority of high-quality companies? Download our Long-term quality investing guide.

Quality companies have pricing power

The biggest impact of rising inflation are the increased costs of raw materials and wages which usually rises faster than the companies’ own ability to increase prices. Quality companies are less affected by this effect, as quality companies have significant pricing power.

In other words, the demand for the products and services are high and there are little or no alternative sources for these products and services due to competitive barrier of entry

Companies with pricing power can more easily raise the prices of their products and services and pass these on directly to the customers. Consequentially, the profit margins of these businesses remain mostly unaffected by rising costs.

For example, Canadian National Railway Company can easily raise the prices of their transportation services as there are no natural alternatives to long-distance cargo transportation over land.

Healthy balance sheet protects quality companies

A healthy balance sheet and a good credit rating makes it easier for companies to raise temporary capital even in a turbulent economic environment. Credit investors are less willing to invest in debt securities during inflationary periods as the real return on these investments trend downwards and the risk of credit losses increase.

Consequentially, credit capital dries up and gets concentrated towards only the safest companies with the most secure future cash flows.

On the other hand, it is very advantageous to have high levels of fixed interest rate debt at the start of inflationary periods as the interest burden of these melts away due to inflation, but this is unfortunately not a characteristic of quality companies.

Quality companies with high ROIC fare better

A high return on invested capital (ROIC) is another useful asset to have in this environment. ROIC is a measure of a companies’ earnings potential compared to the capital investments required to run the business and a high ROIC means that the reinvestment needs (for example business expansion, maintenance spending etc.) are low compared to the recurring earnings.

Consequentially, when the costs of capital investment rise (i.e., the cost of land, factories, machinery, and inventory) high ROIC companies fare better as there is a larger buffer between the earnings potential and the need for capital investment.

A low-quality business will see profit margins shrink at the same time as the cost of reinvestment rises and may be unable to execute their expansion plans. A quality company will have unaffected profit margins and sufficient capital to continue investing in their businesses. As a result, the latter will be able to take market share.

A relevant example is the world’s largest semiconductor foundry, Taiwan Semiconductor Manufacturing Company (TSMC), which invests close to $30 billion per year in manufacturing plants and technology.

TSMC has a ROIC of 25 % and is therefore able to recover this investment outlay in only four years and has ample cash flows to fund these growth investments even if these costs would increase.

Read more about Taiwan Semiconductor Manufacturing Company: These two Semiconductor Stocks are Sifter Fund’s largest investments

Has the long-lost inflation returned?

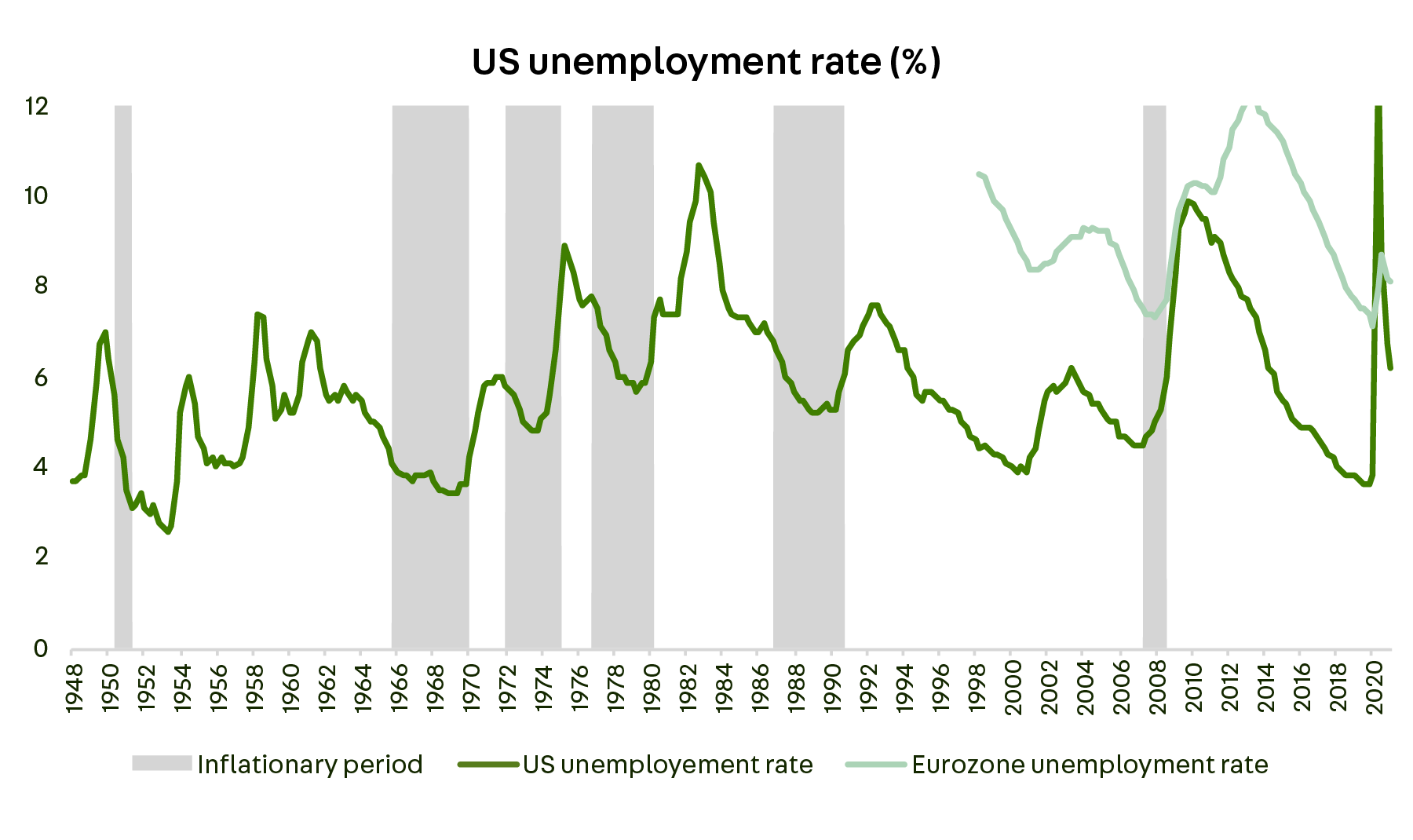

The 2010’s were characterized with low inflation in the Western economies, with the consumer price index averaging around 1.2 – 1.7 % per annum for the decade (For example: the U.S. consumers price index (CPI) for urban consumers: 1.7 %, and the European Union harmonized index of consumer prices: 1.2 %). Today there is speculation that this once lost inflation will return and there were already signs of this happening two years ago when the job markets in the United States and Eurozone were beginning to overheat – an early indication of inflation.

How COVID-19 effected to inflation?

Then the COVID-19 pandemic struck, and we faced the threat of deflation as consumers stopped consuming and businesses halted their expansion plans. In response to this threat, central banks around the world started their money printers on a scale not seen for a long while and this resulted in a massive increase to the money base (Figure 2).

This coincided with large fiscal stimulus directly aimed at the consumers and distressed companies which pushed the newly created money directly out into the economy. The increased amount of money in circulation combined with relatively low levels of industrial production have today caused a shortage of goods in several markets as the economies are reopening and consumers are once again spending money and businesses are investing. High demand combined with low supply will naturally lead to price increases, or in other words, inflation.

Investors with a high quality businesses will worry at lot less than those that do not

An unexpected and persistent rise in inflation is a negative phenomenon to corporations, as the profit margins tend to compress, and the business uncertainty rises. Some companies are more affected than others.

I argue that quality companies will fare better than their lower quality peers, due to their better ability to raise prices to counteract rising costs, easier access to capital, and low capital investment needs relative to profits.

We cannot know today whether the early signals of economic inflation will be a one-time jump in prices or a persistent phenomenon lasting numerous years, but an investor with a high exposure to these quality businesses will worry at lot less than those that do not.

Learn more about Sifter Fund’s qualitative criteria. Download our Long Term Quality Investing Guide.

Alexander Järf

Analyst, Sifter Capital Oy